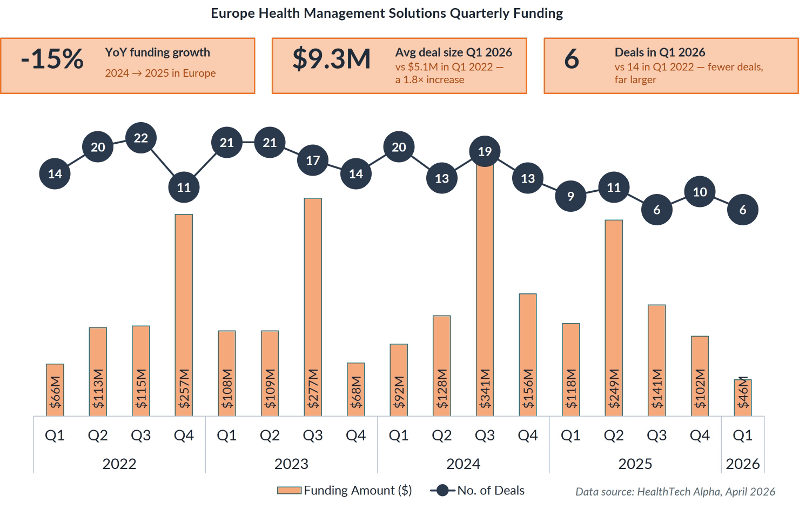

European Health Management Solutions funding fell to $610M in 2025, but the market is maturing fast: average deal size rose 1.8x, and 47% of capital flowed into Clinical Decision Intelligence.

KEY TAKEAWAYS

- Europe’s Health Management Solutions market is not shrinking; it is concentrating. European Health Management Solutions funding fell 15% year-on-year to $610M in 2025, but average deal size rose from $5.1M in Q1 2022 to $9.3M in Q1 2026, signalling a market that is backing fewer, more credible platforms.

- European capital is making a clear bet on clinical intelligence over administrative software. While Healthcare Operations & Workflow represents 38% of European Health Management Solutions ventures, Clinical Decision Intelligence captured 47% of 2025 funding, showing that investors are prioritising evidence-heavy AI over generic workflow digitisation.

- The UK and Germany are becoming Europe’s two practical scale corridors. The UK attracted $285M and Germany $173M in 2025 Health Management Solutions funding, making them the clearest entry points for ventures that can navigate NHS procurement, DiGA reimbursement, and enterprise health system deployment.

- Academic validation is not optional in Europe; it is the procurement gate. Healthcare providers account for 32% of European Health Management Solutions partnerships, while academia, research institutes, and CROs together account for 12%. European buyers want clinical evidence and real-world validation before enterprise adoption.

- Europe’s advantage is regulatory difficulty, not speed. EU MDR, GDPR, public procurement rules, and fragmented workflows slow market entry, but they also create defensible moats for ventures that can prove safety, integration, and outcomes at scale.

A forced revolution, not a slow digital transition

The idea that artificial intelligence is merely an emerging healthcare trend is now obsolete. European healthcare is being re-architected from a labour-driven care system into an intelligence-driven operating model, with Health Management Solutions forming the new operational backbone.

That shift is not optional because healthcare systems can no longer scale demand with labour alone. In Europe, however, change is especially difficult: it must move through public tendering rules, highly local workflows, strict privacy requirements, and one of the world’s most demanding regulatory environments. For investors, pharmaceutical companies, health systems, and ventures, the mandate is clear: win trust locally, prove outcomes rigorously, and scale only where the evidence supports enterprise deployment.

Why is administrative overload forcing health systems toward AI-enabled operations?

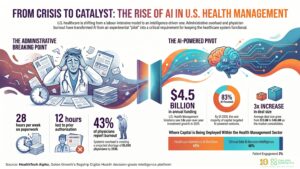

Healthcare capacity is now constrained as much by administration as by clinical demand. The World Health Organization projects a global health worker gap of 18 million by 2030, while clinicians and medical office teams are already losing substantial time to non-clinical work.

The average physician workweek in the U.S. spans 57.8 hours, but only 27.2 hours are spent on direct patient care. Another 30.6 hours – more than half the workweek – go to administrative burden (AMA Prior Authorization Survey 2024). This burden is not unique to the U.S.; European healthcare systems are equally loaded with administrative work.

This friction has clinical consequences. According to the same survey, nearly 9 in 10 physicians report that prior authorisation delays harm clinical outcomes, and nearly 1 in 3 say a patient has experienced a serious adverse event because of these delays. Administrative multitasking also contributes to decision fatigue and diagnostic risk. The result is a structural opening for software that can reduce bottlenecks, standardise workflows, and protect scarce clinical capacity.

The four-layer Health Management Solutions stack: from data infrastructure to patient engagement

Health Management Solutions are not one product category. They are a four-layer operating stack for modern care delivery.

| Layer | Role in the operating stack | Global venture share |

| Clinical Data Infrastructure | Captures, stores, and structures patient data across the care continuum, including EHR mining tools and AI clinical scribes. | 25% |

| Healthcare Operations & Workflow | Streamlines resource planning, patient intake, scheduling, and administrative processes with measurable ROI. | 49% |

| Clinical Decision Intelligence | Turns clinical data into treatment-relevant insight, including risk stratification, surgical planning, and clinical AI. | 18% |

| Patient Engagement | Connects patients and care teams outside the clinic, including remote patient monitoring and follow-up tools. | 9% |

The United States remains the largest global Health Management Solutions market, capturing 41% of Health Management Solutions ventures and $4.5B in 2025 funding. Europe, however, has a different strategic profile: it is less dominated by administrative ROI software and more focused on evidence-heavy clinical intelligence.

Where is European Health Management Solutions capital flowing in 2025?

Europe is the second-largest Health Management Solutions ecosystem globally, with 23% of all Health Management Solutions ventures. Funding fell to $610M in 2025, a 15% year-on-year decline, but the decline masks a maturing market. Fewer exploratory deals are being funded, while larger rounds are concentrating around growth-stage platforms.

Average European Health Management Solutions deal size rose from $5.1M in Q1 2022 to $9.3M in Q1 2026, a 1.8x increase. Capital is not disappearing; it is becoming more selective.

One example of this concentration is Tandem Health, a Swedish startup building a clinical copilot with ambient scribing and automatic medical note generation, which raised $50.0M in Series A funding in 2025, led by Kinnevik AB with participation from Northzone, Amino Collective, and Visionaries Club.

The funding mix matters as much as the headline total because it shows what kinds of problems European buyers and investors believe are worth solving. In 2025, the market did not reward administrative software evenly; it concentrated capital around categories that could demonstrate stronger clinical relevance, defensibility, and evidence.

| European Health Management Solutions category | Share of ventures | Share of 2025 funding |

| Healthcare Operations & Workflow | 38% | 22% |

| Clinical Decision Intelligence | 25% | 47% |

| Clinical Data Infrastructure | 24% | 29% |

| Patient Engagement | 13% | 2% |

This differs sharply from North America, where 49% of capital flowed into Operations & Workflow. In Europe, 47% of 2025 Health Management Solutions funding went to Clinical Decision Intelligence, followed by 29% into Clinical Data Infrastructure. The signal is clear: European investors and health systems are prioritising rigorous clinical AI over purely administrative software.

Which countries are Europe’s Health Management Solutions funding hubs?

European Health Management Solutions capital is heavily concentrated in the United Kingdom and Germany. The UK secured $285M in 2025, making it the primary European beachhead for ventures that can navigate NHS procurement. Germany followed with $173M, supported by the DiGA pathway and a structured route for clinically validated digital health applications.

| Rank | Country | 2025 funding | Strategic market position |

| 1 | United Kingdom | $285M | Dominant European beachhead; the NHS provides rigorous but visible commercial infrastructure for enterprise scaling. |

| 2 | Germany | $173M | Strong secondary entry point; DiGA offers structured access for clinically validated solutions. |

| 3 | Sweden | $51M | Highly digitised early-adopter market for real-world data and evidence generation. |

| 4 | Switzerland | $20M | Key hub for pharmaceutical partnerships and life sciences integration. |

| 5 | France | $18M | Expanding digital health market with strict national health technology assessment requirements. |

Why Europe requires two different Health Management Solutions scaling strategies

Hyper-local operations: workflow software must fit the system

Healthcare Operations & Workflow solutions need deep local integration. A scheduling algorithm, digital front door, or capacity-management tool built for an American fee-for-service environment will not map cleanly onto the NHS, Germany’s decentralised system, or Spain’s regional public systems.

Spain illustrates the local-first model. Spanish Health Management Solutions ventures steer heavily toward domestic healthcare efficiency, with 44% focused on Healthcare Operations & Workflow. These ventures build operating evidence at home before attempting to export proven models abroad.

Borderless intelligence: clinical AI can scale through evidence and regulation

Clinical Decision Intelligence is less dependent on local billing and workflow structures. Sepsis markers, oncology genomics, and surgical-planning algorithms do not change because reimbursement rules change. This gives evidence-backed clinical AI platforms a clearer path to cross-border scale. Europe’s regulatory complexity can become an advantage. Ventures that secure EU MDR clearance and generate robust clinical evidence can turn regulation into a competitive moat. In clinical AI, the burden of proof is high, but once met, it can protect scaled platforms against less validated competitors.

The United States has placed its most aggressive Health Management Solutions bets on Healthcare Operations & Workflow. This category accounts for 44% of U.S. private Health Management Solutions ventures and captured 49% of all U.S. Health Management Solutions venture funding in 2025.

That concentration is not accidental. U.S. health systems are prioritising AI tools that can show immediate board-level value: lower cost, higher throughput, reduced documentation burden, faster scheduling, improved capacity planning, and fewer administrative bottlenecks.

Healthcare Operations & Workflow solutions include supply chain management, hospital capacity planning, scheduling, digital front doors, prior authorisation automation, and ambient documentation. U.S. ventures such as Aledade, QGenda, Qventus, LeanTaaS, Iodine Software, and Clarify Health illustrate how workflow, capacity, scheduling, coding, and operational intelligence are becoming central to the Health Management Solutions stack. These tools address the highest-friction areas of U.S. care delivery before the system can reliably scale more disease-specific or diagnostic AI.

The funding distribution reinforces the operating-model thesis. In the 2025 U.S. Health Management Solutions funding breakdown, Healthcare Operations & Workflow captured 49% of funding, followed by Clinical Data Infrastructure at 24%, Clinical Decision Intelligence at 24%, and Patient Engagement at 3%.

This is a pragmatic sequencing decision. Before health systems can fully benefit from advanced clinical decision intelligence, they need the data infrastructure, workflow integration, governance, and workforce adoption required to make those tools operationally useful.

How do partnerships work as Europe’s due diligence proxy?

Enterprise deployment requires trust. In Europe, that trust is created through a specific partnership mix. Globally, Health Management Solutions partnership volumes declined by 25% from 2024 to 2025 as health systems moved away from broad experimentation and toward fewer, deeper enterprise deployments. In Europe, healthcare providers account for 32% of Health Management Solutions partnerships, confirming active clinical and operational deployment. The more distinctive feature is Europe’s reliance on academic and research validation: academia and research institutes represent 7% of partnerships, while Clinical Research Organisations represent another 5%.

| European Health Management Solutions partner type | Share of partnerships, 2021-2025 |

| Healthcare providers | 32% |

| Startup / venture-to-venture | 9% |

| Tech companies | 9% |

| Academia / institutes | 7% |

| Clinical Research Organisations (CRO) | 5% |

| Government | 4% |

| Other industry verticals | 34% |

Academic and CRO partnerships function as a due diligence proxy. Traditional randomised clinical trials are declining across Health Management Solutions categories – down 43% globally – because adaptive AI tools often require continuous real-world evidence rather than static trial snapshots. Ventures entering Europe need university hospital collaborations, peer-reviewed outcomes data, and deployment-based evidence before they can win public tenders at scale.

What this means

For investors: Concentrate capital on AI-native Health Management Solutions platforms with regulatory clearance, multi-site deployments, and evidence strong enough for enterprise procurement. Clinical Decision Intelligence should remain a high-conviction European category, while the UK and Germany are the priority scaling beachheads.

For pharma and corporate partners: Treat Health Management Solutions platforms as infrastructure for real-world data generation. Clinical Data Infrastructure partnerships can support longitudinal, GDPR-compliant datasets for drug discovery, post-market surveillance, and evidence generation.

For health systems and providers: Move from pilots to enterprise deployments where administrative burden is already constraining capacity. Prioritise proven workflow tools for immediate relief, and require evidence standards, demographic bias auditing, and internal AI governance for clinical decision tools.For digital health ventures: Build academic and CRO partnerships early. Solve local administrative problems with system-specific integrations, or use EU regulatory clearance and clinical evidence to scale Clinical Decision Intelligence across borders. Fragmented point solutions without evidence will struggle as the market consolidates.

FAQ

How much funding did European Health Management Solutions receive in 2025?

European Health Management Solutions venture funding totalled $610M in 2025, down 15% year on year, according to HealthTech Alpha by Galen Growth.

Which Health Management Solutions category attracted the most European funding?

Clinical Decision Intelligence attracted the largest share of European Health Management Solutions funding in 2025, capturing 47% of capital despite representing 25% of ventures.

Which countries led European Health Management Solutions funding in 2025?

The United Kingdom led with $285M in 2025 Health Management Solutions funding, followed by Germany with $173M, Sweden with $51M, Switzerland with $20M, and France with $18M.

Why are academic and CRO partnerships important in Europe?

Academic and CRO partnerships help generate the real-world evidence and clinical validation required for European procurement. Together, academia and CROs represented 12% of European Health Management Solutions partnerships from 2021 to 2025.

Why is Europe different from North America in Health Management Solutions funding?

North America directed 49% of Health Management Solutions capital into Operations & Workflow, while Europe directed 47% into Clinical Decision Intelligence. Europe is therefore more weighted toward evidence-heavy clinical AI than pure administrative ROI software.

Methodology

Data source: HealthTech Alpha by Galen Growth, Q2 2026, covering data up to 15 April 2026. Venture funding figures exclude M&A, IPO, and post-IPO transactions. Figures are in USD; some figures may be understated due to undisclosed deal terms. Partnership counts reflect publicly disclosed agreements. AI-powered ventures are defined as those tagged as Artificial Intelligence enabling technology in the HealthTech Alpha taxonomy. Investor and deal examples are sourced from HealthTech Alpha, April 2026.

Related Galen Growth analysis

- Re-Architecting Healthcare Delivery with AI: Digital Health — Galen Growth, March 2026

- Global Digital Health Ecosystem Q1 2026 Performance Review — Galen Growth

- HealthTech Alpha — global digital health intelligence platform — Galen Growth

How to cite this analysis

About Galen Growth

Galen Growth is the digital health intelligence firm behind HealthTech Alpha, the leading ontology-driven platform tracking the global digital health ecosystem. With operating entities in the US, Europe and Asia, we combine large-scale labelled data, auditable GenAI research and explainable analytics to advise pharma, medical device, insurance, health system, investor and startup clients.