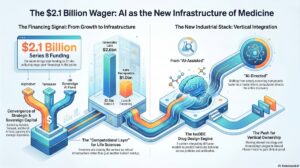

Capital didn’t just flow into Health Management Solutions in 2025 — 83% of it went to a single thesis: that AI must take administration off the clinician’s desk.

KEY TAKEAWAYS

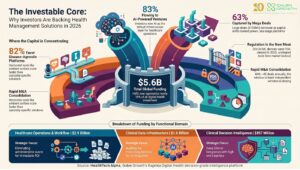

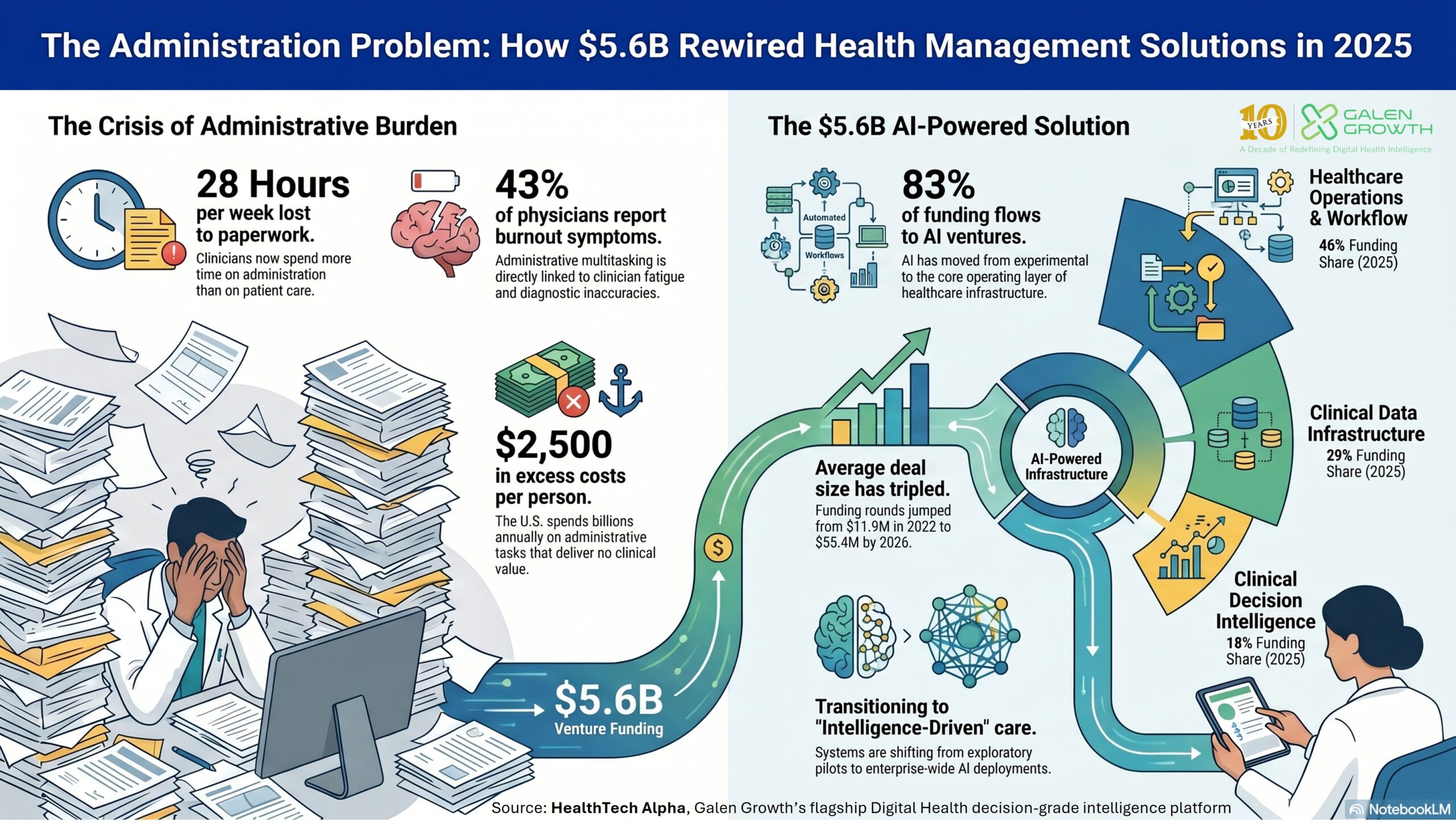

- Health Management Solutions captured $5.6 billion in 2025 venture funding, representing 18.8% of all global digital health funding.

- AI has become the indisputable core infrastructure: an unprecedented 83% of HMS capital flowed into AI-powered ventures by early 2026, up from 61% in 2021.

- The market is rapidly consolidating around late-stage platforms — average deal size tripled from $11.9 million in Q1 2022 to $35.4 million in Q1 2026.

- Healthcare Operations & Workflow captures 46% of health-system partnerships, proving systems are prioritising measurable ROI and capacity relief.

- Asia Pacific is the most asymmetric growth opportunity globally with +87% year-on-year funding growth in 2025; the Middle East +54%; North America plateaued at −5% and Europe contracted −15%.

- WHOOP closed a $575 million Series G and Harbinger Health a $100 million Series B1 — capital is concentrating in execution-focused, AI-native platforms.

Healthcare is structurally constrained by administrative inefficiency, not a lack of clinical demand. When clinicians lose up to 28 hours a week to administration (Google Cloud / Harris Poll, 2024), and the average doctor spends just 27.2 of a 57.8-hour workweek on direct patient care (AMA 2024 Physician Survey), the industry is operating on a fundamentally broken labour model. We are no longer waiting for a digital evolution; we require a structural redesign. It is time to let physicians practise medicine again and let AI do the administration.

The capital markets have already placed their bets on this intelligence-driven future. The next 24 months will ruthlessly separate the market leaders from the laggards, forcing health systems to choose between deploying enterprise-ready platforms and succumbing to operational obsolescence.

1. The administrative crisis: why healthcare is structurally constrained

The structural constraints on modern healthcare delivery have elevated administrative burden from a mere inefficiency to a severe clinical risk. Today, 43.2% of U.S. physicians report symptoms of burnout (AMA Org Biopsy 2024), driven by high-stakes clinical judgement colliding with administrative multitasking. To solve this, Health Management Solutions have rapidly emerged as the essential operating layer for care delivery. In 2025, these solutions captured a staggering $5.6 billion in venture capital, accounting for 18.8% of global digital health funding.

The market has definitively moved past exploratory pilots, bolstered by increasing regulatory clarity. The FDA’s issuance of the Total Product Life Cycle (TPLC) framework for AI-enabled device software has provided the clearest regulatory roadmap to date, driving approvals to a record 324 in 2025 alone. Consequently, capital is heavily consolidating around AI-native platforms capable of true enterprise scale. This consolidation is led by dominant tech infrastructure players like Microsoft and Google Cloud, alongside Electronic Health Record (EHR) giants such as Epic Systems and Oracle Cerner, who are aggressively acquiring leading independent tools. By early 2026, the average venture deal size had tripled to $35.4 million, confirming that the “winner-takes-most” dynamic is already in motion.

Implication: Health systems can no longer afford to run endless, isolated pilots; they must aggressively procure and integrate enterprise-ready AI platforms to survive.

Chart 1: AI’s rising dominance in Health Management Solutions (HMS) funding (2021–Q1 2026)

2. Let doctors be doctors: automating the operations layer

Health systems are overwhelmingly betting on operational efficiency over experimental clinical tools, seeking immediate relief from critical workforce shortages. When analysing the distribution of health system partnerships, Healthcare Operations & Workflow leads definitively, capturing 46% of total partnership activity within the cluster. Buyers are demanding immediate, measurable return on investment, focusing on solutions that alleviate capacity pressures, automate patient intake, and solve the administrative bottleneck that restricts care.

The United States health care system spends an estimated $2,500 per person per year on excess administrative costs that do not deliver clinical value, a staggering amount.

— Noah Benedict, President & CEO, Rhode Island Primary Care Physicians Corp.

Partnership strategies are reflecting this shift toward scale. Overall partnership volume actually declined by 25%, from 846 in 2024 to 636 in 2025 — a clear signal that health systems are abandoning exploratory pilots in favour of deep, enterprise-wide deployments with a select few proven vendors. While disease-agnostic platforms dominate the landscape — capturing 82% of total funding — investors are also placing highly strategic bets in specific therapeutic areas where AI can drive massive impact. Mental Health and Oncology represent the clearest near-term signals for disease-specific tools. Ventures such as WHOOP, which secured a massive $575 million Series G, and Harbinger Health with its $100 million Series B1, underscore the immense scale of capital available for execution-focused platforms.

Implication: Vendors must demonstrate real-world evidence and deep EHR workflow integration, as innovation without seamless execution will be excluded from health system procurement.

3. The global divide in AI adoption

While the shift toward AI-powered health systems is global, regional ecosystems reveal distinctly different priorities and routes to market.

Chart 2: Regional funding snapshot 2025 — growth vs. scale

| Region | 2025 funding | YoY growth | Where the money went |

| North America | $4.5B | −5% | 49% Operations & Workflow |

| Europe | Contracted | −15% | 47% Clinical Decision Intelligence |

| Asia Pacific | Surged | +87% | 34% Data Infra / 34% Operations |

| Middle East | Surged | +54% | Greenfield buildout |

North America (the scale leader). North America dominates the global market in pure scale, accounting for 41% of all ventures and bringing in $4.5 billion in 2025 funding. The U.S. ecosystem is heavily focused on solving administrative bottlenecks, with 49% of regional ventures concentrated in Healthcare Operations & Workflow.

Europe (the clinical intelligence hub). Europe differentiates itself through deep clinical intelligence. A massive 47% of its regional funding is captured by Clinical Decision Intelligence. Navigating the European market requires stringent validation, with ventures relying heavily on partnerships with academic institutions and clinical research organisations to meet strict regulatory and evidence requirements.

Asia Pacific (the fastest-growing greenfield). APAC represents the fastest-growing greenfield opportunity globally, with a 87% year-on-year surge in funding in 2025. Because many APAC health systems are digitising from the ground up, funding is evenly split: 34% directed to foundational Clinical Data Infrastructure, and another 34% to Operations to address severe regional workforce gaps.

Implication: Scaling globally requires bespoke market-entry strategies; a vendor built for U.S. enterprise sales must fundamentally redesign its approach to win in Europe or APAC.

What this means

| For investors Concentrate capital in late-stage, AI-native platforms with regulatory clearances and multi-site deployments. The market is consolidating into a winner-takes-most dynamic, with average deal size tripled to $35.4M. Look towards APAC for the most asymmetric, high-growth opportunities. | For pharma & corporate partners Pharmaceutical leaders must prioritise Clinical Data Infrastructure — which already captures 43% of pharma partnerships — and Clinical Decision Intelligence (28%). Leverage Health Management Solutions to build robust Real-World Data infrastructure and accelerate R&D and drug development pipelines. |

| For health systems & providers Stop running endless pilots. Shift to enterprise-wide deployments with selected vendors to secure measurable ROI and alleviate severe workforce shortages. Align CIOs and CMOs on a digital roadmap; prioritise tools that integrate seamlessly with existing EHR environments. | For digital health ventures Innovation alone is no longer enough; execution is the differentiator. Demonstrate real-world evidence, regulatory credibility, and deep workflow integration. Without measurable ROI and multi-site production deployment, you risk being permanently locked out of health-system procurement and future capital. |

FAQ

What are Health Management Solutions in digital health?

Health Management Solutions (HMS) represent the essential operating layer of modern healthcare systems, designed to transition healthcare from a labour-driven model to an intelligence-driven system. The category covers four functional layers: Clinical Data Infrastructure, Healthcare Operations & Workflow, Clinical Decision Intelligence, and Patient Engagement.

How much venture funding did Health Management Solutions raise in 2025?

Health Management Solutions raised $5.6 billion in venture funding in 2025, accounting for 18.8% of all global digital health funding. 83% of that capital flowed directly into AI-powered ventures.

Is AI being used in healthcare management systems?

Yes. AI has rapidly transitioned from an experimental concept to the core infrastructure of healthcare management. In 2025, 83% of HMS venture funding flowed directly into AI-powered ventures.

What kind of digital solutions are hospitals actually buying?

Hospitals and health systems are prioritising ROI-driven operational AI solutions, especially Healthcare Operations & Workflow tools such as ambient clinical scribing, supply-chain management, scheduling, and capacity planning.

How do trends differ between the US, Europe, and Asia Pacific?

The United States dominates in scale, Europe differentiates as a clinical intelligence hub, and Asia Pacific is seeing rapid growth driven by greenfield deployment and healthcare worker shortages.

What share of digital health funding is going to Health Management Solutions?

In 2025, Health Management Solutions captured 18.8% of all global digital health venture funding, equivalent to $5.6 billion in deployed capital.

Methodology

Data source: HealthTech Alpha by Galen Growth, Q2 2026 (covering data up to 30 March 2026). Venture funding figures exclude M&A, IPO, and post-IPO transactions. Figures are in USD; some figures may be understated due to undisclosed deal terms. Partnership counts reflect publicly disclosed agreements; AI-powered ventures are defined as those tagged as Artificial Intelligence enabling technology in the HealthTech Alpha taxonomy.

Related Galen Growth analysis

- Re-Architecting Healthcare Delivery with AI: Digital Health 2026 — galengrowth.com/product/health-management-solutions-digital-health-2026/

- Global Digital Health Ecosystem Q1 2026 Performance Review — galengrowth.com/digital-health-q1-2026-trends/

- Epic Joins the AI Scribe Race: Can Startups Still Win? — galengrowth.com/epic-joins-the-ai-scribe-race-can-startups-still-win/