IQVIA’s Global Trends in R&D 2026 confirms what the digital health data has been signalling for two years: pharma’s productivity problem lives in execution, not discovery — and the capital is already reallocating.

KEY TAKEAWAYS

- The United States accounts for 41% of global Health Management Solutions ventures, making it the largest market for Health Management Solutions innovation globally.

- U.S. venture funding for Health Management Solutions reached $4.5 billion in 2025, representing 1.8x year-over-year growth.

- By Q1 2026, 83% of all U.S. Health Management Solutions funding was deployed to AI-powered ventures, up from 61% in 2021.

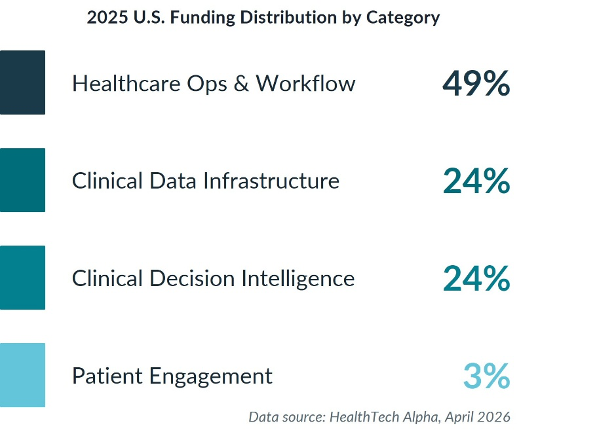

- Healthcare Operations & Workflow captured 44% of U.S. private Health Management Solutions ventures and 49% of U.S. Health Management Solutions venture funding in 2025, making it the dominant category in the market.

- U.S. physicians spend 28 hours per week on administrative work, while prior authorisation consumes roughly 12 hours of staff time per physician each week.

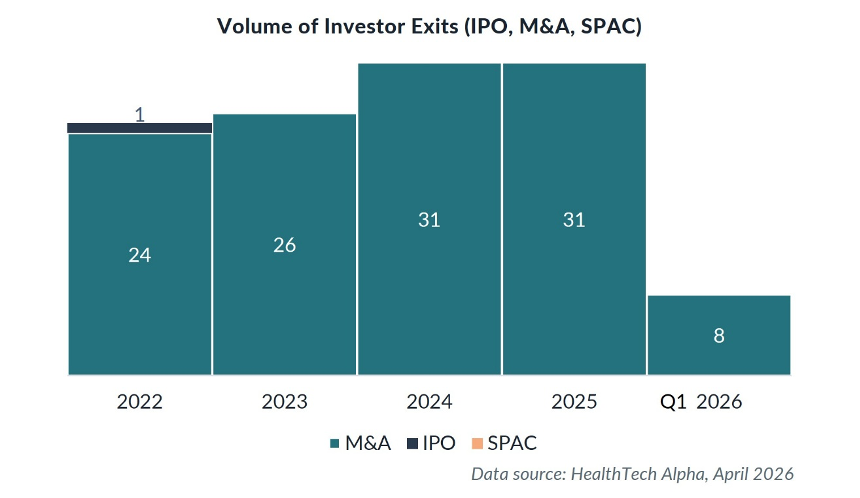

- The U.S. Health Management Solutions market recorded 31 exits in 2025, and the country accounted for 93% of global Health Management Solutions mega rounds that year.

U.S. healthcare did not become the global leader in AI-powered Health Management Solutions because it had excess capacity to experiment. It became the leader because the operating model was breaking.

Administrative burden, clinician burnout, workforce shortages, and rising costs have made AI-enabled Health Management Solutions a practical requirement rather than a speculative innovation theme. This article explains why the United States has become the global vanguard for Health Management Solutions, where capital is concentrating, and what the shift means for investors, pharma, health systems, and digital health ventures.

The U.S. healthcare system reached an administrative breaking point

The core constraint in U.S. healthcare is no longer only clinical demand; it is the administrative load required to deliver care. The average U.S. physician works 57.8 hours per week, but only 27.2 hours are spent on direct patient care (AMA 2024).

Prior authorisation has become one of the clearest examples of this structural burden. Physicians face roughly 43 prior authorisation requests per week, consuming approximately 12 hours of dedicated staff time (AMA Prior Authorization Survey, 2024). This is not just a workflow problem. According to the survey, 9 in 10 physicians report that prior authorisation negatively impacts patient outcomes, and nearly 1 in 3 report that a patient has experienced a serious adverse event due to these delays.

The workforce data makes the operating challenge more urgent. As of 2024, 43.2% of U.S. physicians reported symptoms of burnout (AMA Org Biopsy 2024). The system is also facing a projected shortage of more than 85,000 physicians by 2036 (AAMC) and an existing deficit of registered nurses.

Implication: U.S. health systems are not adopting AI-powered Health Management Solutions to modernise at the margins. They are using AI to shift from a labour-intensive operating model toward an intelligence-driven delivery model.

Why is U.S. Health Management Solutions investment concentrating around AI-powered platforms?

Capital is following the system’s most urgent operational pain points. In 2025, U.S. venture funding for Health Management Solutions reached $4.5 billion, representing 1.8x year-over-year growth. By Q1 2026, 83% of U.S. Health Management Solutions funding was directed to AI-powered ventures, up from 61% in 2021.

This shift indicates that investors no longer view operational AI as an experimental category. They are treating AI-enabled Health Management Solutions as enterprise infrastructure for healthcare delivery.

The venture landscape reflects this infrastructure shift. Companies such as Abridge, Ambience Healthcare, Innovaccer, and Saama are positioned around clinical data infrastructure, ambient documentation, analytics, and AI-enabled operational intelligence rather than narrow point-solution functionality. The funding pattern also shows a market moving away from early-stage experimentation and toward platform consolidation. Average U.S. Health Management Solutions deal size increased from $13.6 million in Q1 2022 to $46.6 million in Q1 2026, a more than threefold increase. Mega rounds of $100 million or more captured 63% of total capital, and the United States accounted for 93% of global Health Management Solutions mega rounds in 2025.

U.S. Health Management Solutions a winner-takes-all segment

The competitive landscape is also consolidating. The U.S. Health Management Solutions ecosystem now includes more than 19 unicorn-valuation companies, while M&A activity accelerated to 31 exits in 2025 – nearly one acquisition every 12 days. Much of this exit activity can be attributed to venture-to-venture acquisitions, as companies combine point solutions into broader platforms before approaching health systems for procurement. The exit data underscores this consolidation: acquisitions dominate U.S. Health Management Solutions exits, and activity accelerated sharply into 2024.

Operations & Workflow became the centre of the U.S. Health Management Solutions market

The United States has placed its most aggressive Health Management Solutions bets on Healthcare Operations & Workflow. This category accounts for 44% of U.S. private Health Management Solutions ventures and captured 49% of all U.S. Health Management Solutions venture funding in 2025.

That concentration is not accidental. U.S. health systems are prioritising AI tools that can show immediate board-level value: lower cost, higher throughput, reduced documentation burden, faster scheduling, improved capacity planning, and fewer administrative bottlenecks.

Healthcare Operations & Workflow solutions include supply chain management, hospital capacity planning, scheduling, digital front doors, prior authorisation automation, and ambient documentation. U.S. ventures such as Aledade, QGenda, Qventus, LeanTaaS, Iodine Software, and Clarify Health illustrate how workflow, capacity, scheduling, coding, and operational intelligence are becoming central to the Health Management Solutions stack. These tools address the highest-friction areas of U.S. care delivery before the system can reliably scale more disease-specific or diagnostic AI.

The funding distribution reinforces the operating-model thesis. In the 2025 U.S. Health Management Solutions funding breakdown, Healthcare Operations & Workflow captured 49% of funding, followed by Clinical Data Infrastructure at 24%, Clinical Decision Intelligence at 24%, and Patient Engagement at 3%.

This is a pragmatic sequencing decision. Before health systems can fully benefit from advanced clinical decision intelligence, they need the data infrastructure, workflow integration, governance, and workforce adoption required to make those tools operationally useful.

Health systems are moving from AI pilots to enterprise deployments

The U.S. health system adoption model has changed. Exploratory pilots are giving way to enterprise-scale deployments with vendors that can prove production readiness.

Healthcare providers are the primary drivers of collaboration in the U.S. Health Management Solutions market, accounting for 37% of all Health Management Solutions partnerships, the highest share of any global region. Adoption is also accelerating inside clinical environments. As of 2024, 71% of U.S. hospitals were running EHR-integrated predictive AI, up from 66% the prior year.

Procurement standards are becoming more demanding. Health systems now require evidence of multi-site deployment, tangible clinical outcomes, disaggregated demographic performance, and alignment with existing EHR roadmaps. Vendors are also being evaluated against the product trajectories of major EHR platforms such as Epic and Oracle, because many standalone workflow tools may eventually become native EHR features. This shift changes the vendor selection process. Health systems are no longer asking whether AI can work in principle. They are asking whether a solution can integrate into existing clinical and operational systems, perform consistently across patient populations, reduce administrative pressure, and survive the procurement scrutiny of enterprise deployment. Ventures such as Qventus, LeanTaaS, Abridge, Ambience Healthcare, and Arcadia demonstrate how enterprise-readiness is becoming a defining feature of the U.S. Health Management Solutions market.

8. What this means

| For investors: The U.S. Health Management Solutions investment window is narrowing around AI-native platforms with enterprise deployments, regulatory clarity, and defensible integration. Investors should be cautious about standalone workflow tools that may be absorbed into Epic, Oracle, or broader Health Management Solutions platforms. | For pharma sponsors and corporate partners: Pharma is using Health Management Solutions platforms less for administrative efficiency and more for data infrastructure. Clinical Data Infrastructure represents 43% of pharma’s Health Management Solutions partner mix and Clinical Decision Intelligence 28%, reflecting the strategic importance of real-world data, real-world evidence, and prospective registry models. |

| For health systems and providers: Health systems will differentiate through execution, not through the number of AI pilots they announce. The priority should be internal AI governance, clinical informatics leadership, workforce training, demographic performance monitoring, and procurement discipline. | For digital health ventures: Digital health companies need to prove enterprise readiness earlier. Multi-site deployment, EHR integration, outcome evidence, and clear buyer ROI will matter more than product novelty. |

FAQ

Why is the United States leading Health Management Solutions adoption?

The United States leads Health Management Solutions adoption because administrative overload, clinician burnout, workforce shortages, and rising costs have made AI-powered operating tools a practical necessity. The U.S. accounts for 41% of global Health Management Solutions ventures.

How much U.S. venture funding went into Health Management Solutions in 2025?

U.S. venture funding for Health Management Solutions reached $4.5 billion in 2025, representing 1.8x year-over-year growth.

What share of U.S. Health Management Solutions funding goes to AI-powered companies?

By Q1 2026, 83% of U.S. Health Management Solutions funding went to AI-powered ventures, up from 61% in 2021.

Which Health Management Solutions category is most important in the United States?

Healthcare Operations & Workflow is the leading U.S. Health Management Solutions category. It represents 44% of U.S. private Health Management Solutions ventures and captured 49% of U.S. Health Management Solutions venture funding in 2025.

What does U.S. Health Management Solutions growth mean for health systems?

Health systems should move beyond isolated pilots and prioritise enterprise-ready AI tools that reduce administrative workload, integrate with EHR systems, and show measurable clinical or operational outcomes.

Methodology

Data source: HealthTech Alpha by Galen Growth, Q2 2026, covering data up to 15 April 2026. Venture funding figures exclude M&A, IPO, and post-IPO transactions. Figures are in USD; some figures may be understated due to undisclosed deal terms. Partnership counts reflect publicly disclosed agreements. AI-powered ventures are defined as those tagged as Artificial Intelligence enabling technology in the HealthTech Alpha taxonomy. Investor and deal examples are sourced from HealthTech Alpha, April 2026.

Related Galen Growth analysis

- Digital health funding in Clinical Trials: Why Execution, Not Discovery, is Pharma’s Next Existential Bottleneck — Galen Growth, March 2026

- HealthTech Alpha — global digital health intelligence platform — Galen Growth

- Galen Growth Insights — full archive of digital health analyses — Galen Growth

How to cite this analysis

About Galen Growth

Galen Growth is the digital health intelligence firm behind HealthTech Alpha, the leading ontology-driven platform tracking the global digital health ecosystem. With operating entities in the US, Europe and Asia, we combine large-scale labelled data, auditable GenAI research and explainable analytics to advise pharma, medical device, insurance, health system, investor and startup clients.