TL;DR

Emphasis on Clinical Strength: The digital health industry is increasingly prioritizing clinical evidence as a critical factor for investment and growth. Partnerships drive clinical proof, with 24% of all private digital health ventures globally having demonstrated clinical strength through clinical trials, regulatory filings, or peer-reviewed publications.

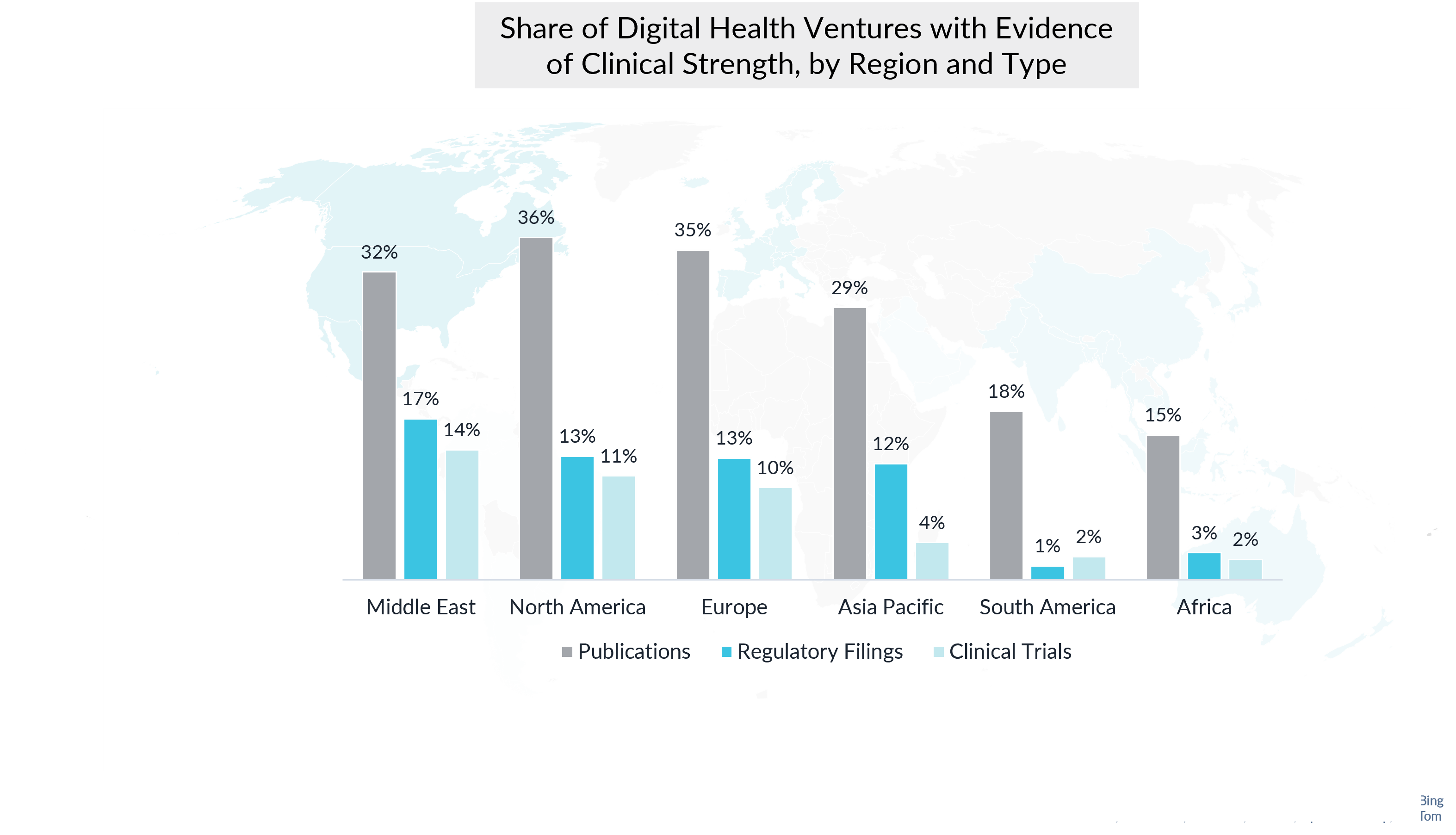

Regulatory Support and Regional Leaders: The regulatory landscape for digital health is becoming more supportive worldwide. Europe leads with 29% of its ventures showcasing clinical strength, while the Middle East and North America each account for 24%.

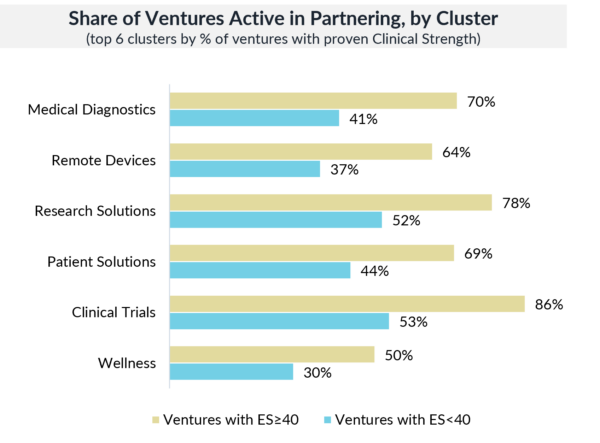

Partnerships Drive Success: Ventures with proven clinical strength are more likely to secure partnerships, which are crucial for accessing patients, funding, and clinical expertise. In the top five digital health clusters, ventures with clinical strength have 1.5 times more partnerships than those without.

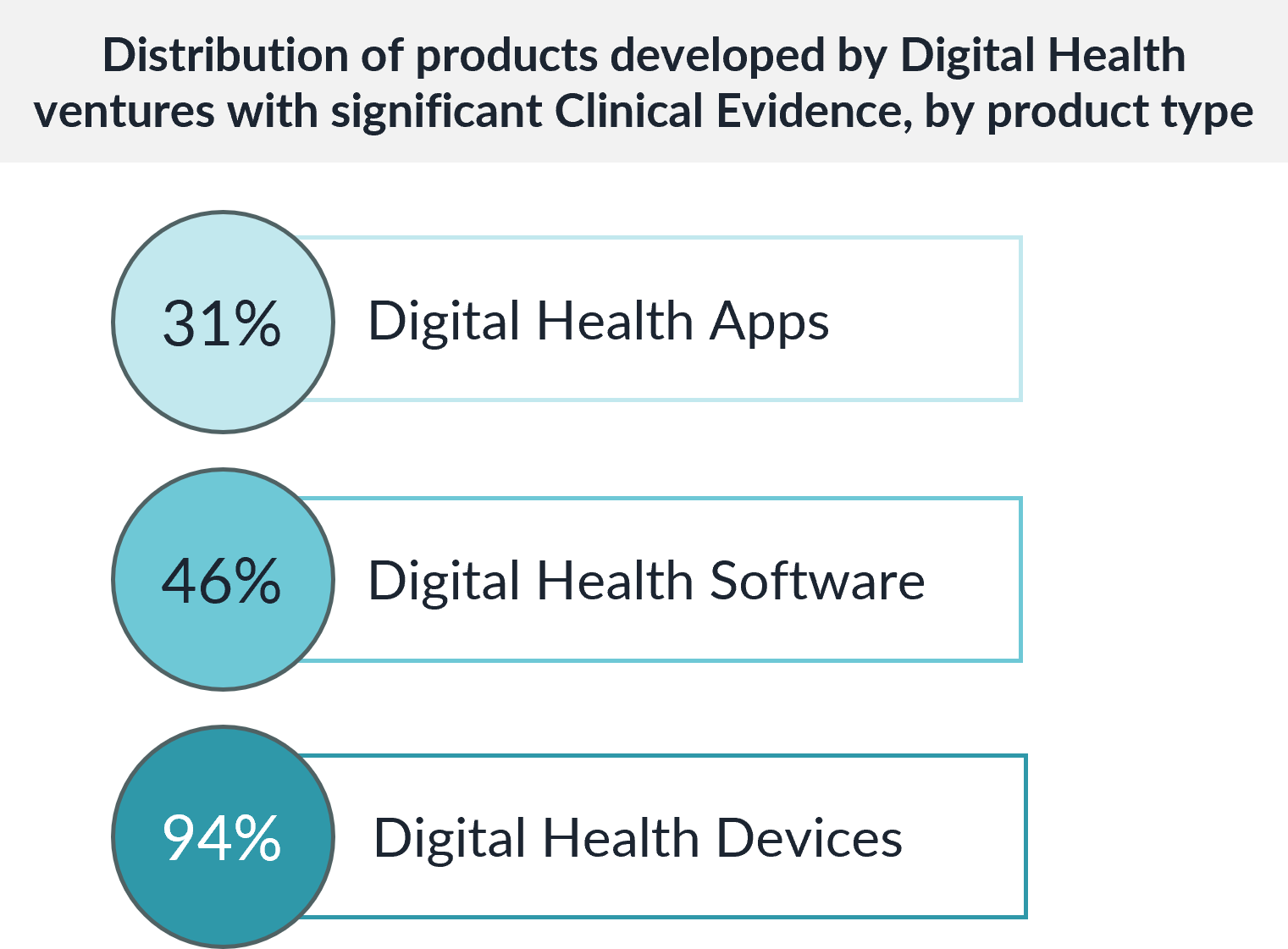

Product Category Disparities: Navigating health-related apps, software, and devices can be challenging. Only 31% of digital health apps have proven clinical strength, compared to 46% of software products and 94% of digital health devices.

As the digital health industry matures, clinical evidence has become paramount. Partnerships drive clinical proof in this space where technology meets patient care. Demonstrating clinical strength through validated proof points is increasingly seen as a critical factor for scaling and investment. The “Clinical Strength in Digital Health Innovation 2024” report by Galen Growth offers a comprehensive look at how ventures across the globe are approaching this challenge and what it means for the future of digital health.

The report draws from HealthTech Alpha’s extensive dataset, analysing the clinical strength of digital health ventures and products across various regions and categories. This blog delves into the key findings, including the shift towards clinical evidence, the role of partnerships, differences between digital health clusters, and the disparities between product categories.

The Shift Toward Clinical Proof Points in Digital Health

Over the past decade, robust Digital Health companies have thrived due to innovative ideas and sound business strategies. However, there is a noticeable shift towards emphasising proof points, with Clinical Strength emerging as a crucial data point. According to the report, 24% of private digital health ventures globally have demonstrated clinical strength through clinical trials, regulatory filings, or peer-reviewed publications. This focus on clinical proof points responds to growing demands from healthcare providers, payers, and investors who require evidence of a product’s safety and efficacy before committing to its adoption or funding.

Clinical strength has become a priority data point, particularly in an industry that operates at the intersection of technology and patient care. Ventures that can provide robust clinical evidence are more likely to gain traction in the market, attract investment, and form partnerships with established healthcare providers and payers. This trend is expected to continue as the industry evolves, with proof-points becoming a standard expectation for digital health products.

Galen Growth’s Evidence Signal in HealthTech Alpha enables the evaluation of a venture’s clinical strength or its ability to prove that its products are safe and effective. In particular, the Evidence Signal (ES) considers the number of clinical trials, regulatory filings and peer-reviewed publications that a venture has for its Digital Health products. A venture with at least one clinical trial, one regulatory filing or four peer-reviewed publications can be considered to have proven clinical strength.

A Favourable Regulatory Landscape for Digital Health

The regulatory environment for digital health is becoming increasingly supportive worldwide. The U.S. FDA’s release of the Digital Health Policy Navigator in January 2022 marked a significant step towards streamlining the regulatory process for digital health products. This initiative provides a clear framework for navigating the complex regulatory landscape, making it easier for innovators to bring clinically validated products to market.

Similarly, the Digital Health Applications (DiGA) program has grown significantly in Germany, with over 50 successful applications as of 2024. The DiGA program allows digital health applications with proven clinical benefits to be prescribed by healthcare providers and reimbursed by the healthcare system. This has created a favourable environment for digital health ventures to thrive, particularly those that can demonstrate clinical strength.

Regionally, Europe leads the way, with 29% of its digital health ventures boasting proven clinical strength. The continent’s supportive regulatory framework and robust funding and research infrastructure have positioned it as a leader in digital health innovation. The Middle East and North America follow, with 24% of ventures demonstrating proven clinical strength. These regions are also seeing positive regulatory developments, which are expected further to support the growth of clinically validated digital health solutions—21% of ventures in Asia Pacific.

The Role of Partnerships in Driving Clinical Evidence

Partnerships play a crucial role in the development and success of digital health ventures, particularly those with proven clinical strength. The report highlights that ventures with clinical evidence are significantly more likely to form partnerships essential for accessing patients, funding, and clinical expertise.

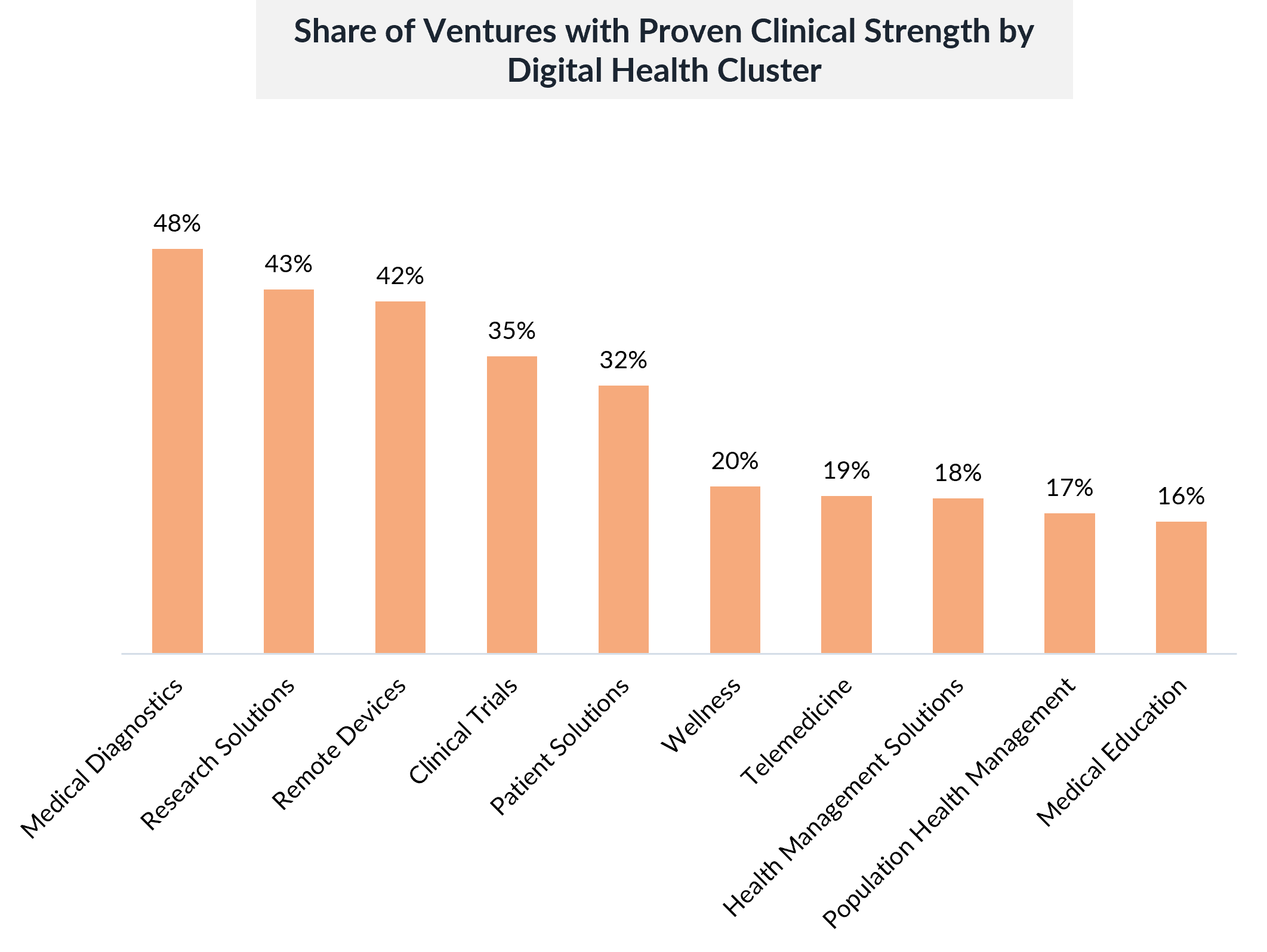

In the top five digital health clusters—Medical Diagnostics, Patient Solutions, Wellness, Remote Devices, and Research Solutions—ventures with proven clinical strength have at least 1.5 times more partnerships than those without. Clinical trials are particularly important, with 85% of ventures with clinical evidence actively engaging in partnerships. Partnerships drive clinical proof through these collaborations, which are crucial for conducting rigorous clinical trials, gaining regulatory approvals, and ultimately proving the efficacy and safety of digital health products.

Partnerships drive clinical proof by providing access to valuable resources and enhancing a venture’s credibility in the eyes of investors and regulators. For example, collaborations with hospitals and research institutions can facilitate access to clinical data and patient populations. At the same time, partnerships with established healthcare companies can provide the financial support needed to conduct large-scale clinical trials. This collaborative approach is a crucial strategy for digital health ventures looking to develop and demonstrate clinical strength.

Navigating the Digital Health Product Landscape: Apps, Software, and Devices

The digital health product landscape encompasses everything from mobile apps and software to sophisticated medical devices. However, the level of clinical evidence required varies significantly across these categories, reflecting the different regulatory and safety standards applicable to each.

- Digital Health Apps: Despite their popularity, only 31% of digital health apps have demonstrated clinical strength. Many health apps focus on wellness and lifestyle, often not requiring the same level of clinical evidence as more complex medical products. However, as the market matures and more apps claim to offer medical benefits, there will be increased scrutiny and demand for clinical evidence.

- Software Products: Software products, which include clinical decision support systems, electronic health records, and telemedicine platforms, have a higher rate of proof-points, with 46% demonstrating clinical strength. These products often operate in more regulated environments and are integral to patient care, making clinical evidence necessary for market entry and adoption.

- Digital Health Devices: Digital health devices, such as remote monitoring tools and diagnostic equipment, have the highest rate of clinical evidence, with 94% showing proven clinical strength. Devices are subject to stringent regulatory scrutiny, requiring rigorous clinical testing to meet safety and efficacy standards. This high level of validation is crucial for devices used directly in patient care, as they must prove their reliability and safety to gain regulatory approval and market acceptance.

Navigating this complex landscape requires a nuanced understanding of the regulatory requirements and clinical evidence standards applicable to each product category. For healthcare providers and payers, the challenge lies in identifying which products offer genuine clinical benefits, while for digital health ventures, the challenge is to provide the necessary proof points to support their claims.

Medical Diagnostics: A Model of Clinical Strength

Medical diagnostics ventures are often at the forefront of digital health innovation, utilising advanced technologies such as AI and machine learning to enhance diagnostic accuracy and efficiency. However, the high stakes involved in medical diagnostics necessitate rigorous proof-points to ensure these tools are reliable and effective. This is particularly important given these tools’ direct impact on patient care and outcomes.

The emphasis on clinical evidence within the Medical Diagnostics cluster is particularly pronounced. According to the report, 48% of all ventures and 78% of growth- and late-stage ventures in this cluster have proven clinical strength. This focus is reflected in the funding landscape, with 95% of the cumulative funding value in the first half of 2024 directed towards ventures with proven clinical strength.

Interestingly, the growing interest in generative AI within healthcare has led some investors to shift their focus to AI-driven ventures, sometimes at the expense of ventures with proven clinical robustness. For more information, download Galen Growth’s full report on AI in Digital Health. While AI has the potential to revolutionise healthcare, it is crucial that these solutions are developed and validated with the same rigour as other digital health products. Without proper proof-points, the adoption of AI in healthcare could avoid significant hurdles, particularly in gaining the trust of healthcare providers and regulators.

Conclusion

The “Clinical Strength in Digital Health Innovation 2024” report highlights the growing importance of clinical evidence in the digital health sector. As the industry continues to evolve, the demand for clinically validated solutions is expected to increase, driven by regulatory developments, investor expectations, and the need for products that can demonstrably improve patient outcomes.

Partnerships drive clinical proof and are a crucial factor for success in the digital health industry. Ventures prioritizing clinical evidence will be better positioned to secure partnerships, funding, and market adoption, ultimately setting themselves apart in an increasingly competitive landscape.

Download the full report from Galen Growth’s website to explore these insights in more detail and gain a deeper understanding of the digital health ecosystem. Stay informed and stay ahead in the rapidly changing world of digital health!