TL;DR

Venture Funding: In Europe, Q1 saw a funding increase of 48% over Q4, but the enthusiasm was quelled with a lacklustre Q2, leaving an overall first-half performance of $1.5B, 7% lower than H1 2023. The share of digital health funding in Europe accounted for only 12% of global funding, marking a two-percentage-point YoY decline.

Funding Strength: As global venture capital inflows regain momentum in H1 2024, funding stress is gradually easing. Ventures in Europe have maintained a steady level of funding strength, with 42% of growth-stage ventures having raised funding in the past 18 months. Galen Growth’s Alpha Forecaster indicates that ventures with above-average venture signals are poised to attract strong investor interest during the next half of 2024.

Biopharma: As biopharma seeks to supplement drug discovery and development processes with technological innovation, such as AI and large datasets, biopharma emerged as the primary driver of partnerships in the first half of the year, forging 21% of all collaborations. This underscores the transformative potential of technology in advancing biopharma capabilities.

Patient Solutions: Digital Therapeutics remains a focus for European ventures. The Patient Solutions cluster (including Digital Therapeutics) moved to the top funded spot in H1 2024, with $396M of venture capital deployed over 27 deals. Research Solutions followed with $1.76B. The substantial investment in patient and research solutions emphasises the surge in AI-driven research and healthcare tools in 2024.

AI in Digital Health: In 2024, investments in AI-driven ventures surged, making up 65% of the total funding for European-founded ventures in the year’s first half. This is a significant share, especially given that only 43% of these ventures utilise AI technology. However, only 2% of European private digital health ventures leverage generative AI technology.

In the first half of 2024, Europe’s digital health landscape exhibited resilience and challenges amidst a fluctuating funding environment. While global digital health investments surged, Europe experienced a modest decline in funding compared to the previous year. However, the sector witnessed significant advancements in biopharma collaborations, patient solutions, and the adoption of AI-driven technologies. This blog delves into the key trends, investment dynamics, and notable developments within the European digital health ecosystem, leveraging data from Galen Growth’s comprehensive “Europe Digital Health Innovation H1 2024” report.

A Mixed Funding Landscape: Triumphs and Troubles

Contrary to the North America trend where digital health funding reached $9.6 billion across 414 deals, marking a notable 13% YoY increase from H1 2023, Europe saw a contrasting scenario. European digital health ventures attracted $1.5 billion in H1 2024, representing a 7% year-over-year decrease from H1 2023. This decline was particularly evident in Q2, which saw a 23% drop from Q1, despite the initial 48% quarter-over-quarter increase from Q4 2023. The share of digital health funding in Europe accounted for only 12% of the global total, a decrease from 14% in 2023. The funding winter that plagued Europe in 2022 and 2023 continued to cast a shadow, with cautious investor sentiment prevailing.

Key Investment Trends and Insights: Booming Innovations vs. Stark Realities

Despite the decline, certain European digital health ecosystem areas showed promising growth. Investments in TechBio—digital health solutions for biopharma—remained robust, driven by advancements in foundational models and AI. Ventures in this category (Research Solutions) attracted $1.76 billion in funding, emphasising their potential to revolutionise drug discovery and development processes. Biopharma emerged as the most frequent partner for digital health ventures, accounting for 21% of partnerships in H1 2024. This strong focus on biopharma highlights the sector’s reliance on technological innovations to supplement traditional methodologies. Read Galen Growth’s full report on Digital Health in Biopharma Research for a deep-dive into this Cluster.

Patient Solutions, encompassing digital therapeutics and other patient-centred healthcare innovations, emerged as a top funding recipient. In the first half of 2024, this category saw $396 million deployed across 27 deals. A notable highlight in this sector was Sword Health, a Portuguese-founded digital therapeutics venture, which raised $130 million. This significant investment underscores the growing focus on AI-driven patient care solutions.

Alpha Forecaster: The Investor’s Crystal Ball

Galen Growth’s Alpha Forecaster is an integral tool that leverages proprietary algorithms and a vast database of over 680 million data points to predict venture success and investment attractiveness. This tool provides investors with data-driven insights to identify ventures with strong potential, mitigating risks associated with funding uncertainties. For example, Sword Health, with an Alpha Score of 81.7, demonstrates high innovation and partnership signals, making it an attractive proposition for investors. The platform’s ability to integrate AI in therapeutic interventions has positioned it ahead of its peers, as evidenced by its substantial Series D funding round. Learn more about Sword Health on HealthTech Alpha.

Geographic Distribution and Venture Dynamics: Hotspots and Cold Fronts

The digital health ecosystem in Europe comprises more than 2,800 active ventures, growing at a five-year compound annual growth rate (CAGR) of 8%. The United Kingdom and Germany lead in venture volume, collectively attracting 38% of the funding deployed across Europe during the first half of 2024. This concentration of ventures in key markets underscores the regional hubs of innovation and the strategic importance of these countries in driving digital health advancements.

In terms of funding stages, growth-stage ventures maintained steady funding strength, with 42% raising capital in the past 18 months. This steady funding inflow indicates investor confidence in the scalability and potential market impact of these ventures. However, early-stage and Series A ventures faced the highest funding pressures, with only 27% securing funding within the same period. This disparity highlights early-stage European companies’ challenges in securing initial funding and the critical need for robust business models and clear value propositions to attract investors.

Notable Deals and Partnerships: Power Plays and Strategic Alliances

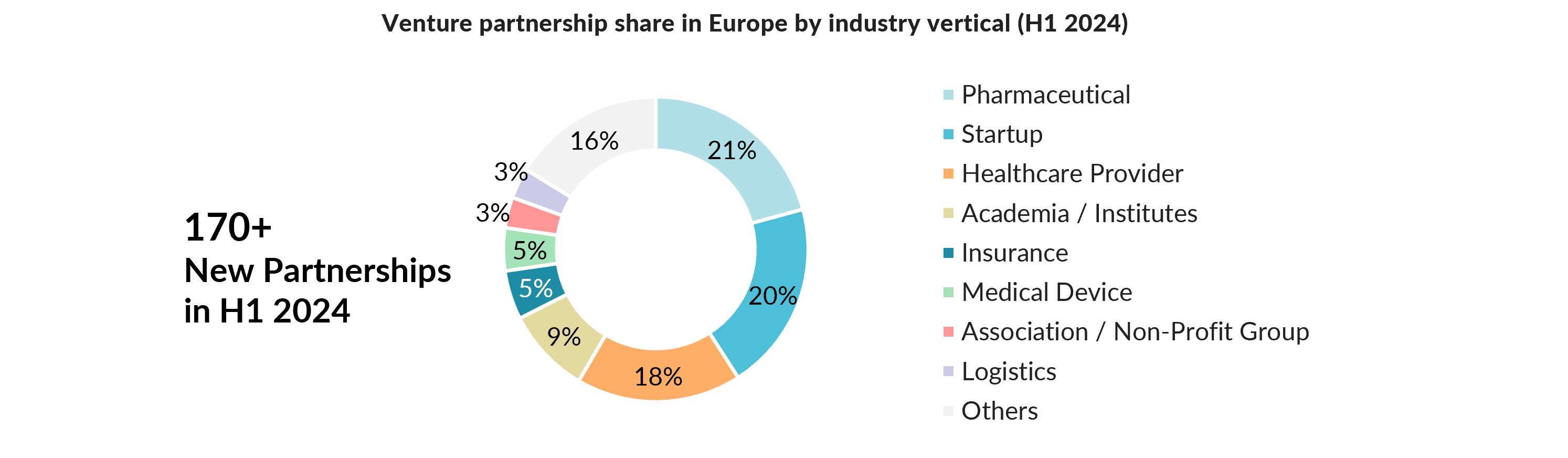

In the first half of 2024, 170 digital health venture partnerships were announced in Europe, a 10% year-over-year increase. Pharmaceutical companies were the most active partners, driven by the need to integrate AI and large datasets into drug discovery and development processes. This strategic focus on leveraging AI to enhance biopharma capabilities underscores the transformative potential of these technologies in accelerating drug development and improving patient outcomes.

Key pharma partners included AstraZeneca and Boehringer Ingelheim, each establishing multiple collaborations with digital health ventures. AstraZeneca, in particular, has been a prolific partner, forming 55 partnerships since 2012. These collaborations highlight the ongoing efforts of pharmaceutical giants to diversify their digital health portfolios and enhance their innovation capabilities through strategic partnerships. Learn more about the digital health portfolios for AstraZeneca and Boehringer Ingelheim in HealthTech Alpha.

Therapeutic Focus and Clinical Evidence: Breakthroughs and Benchmarks

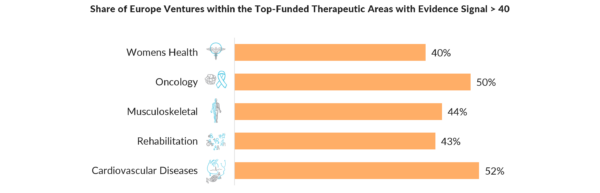

Women’s Health and Oncology were the top-funded therapeutic areas in H1 2024. Women’s Health secured $318 million across 19 deals, primarily driven by Sword Health’s Series D funding round. The significant investment in Women’s Health solutions reflects the growing recognition of the unique healthcare needs of women and the importance of developing targeted solutions to address these needs. Explore Women’s Health ventures in HealthTech Alpha.

Oncology, despite a 7% year-over-year decline, continued to attract significant investment, reflecting the ongoing demand for innovative cancer treatment solutions. Clinical evidence remains a critical factor in venture success, with 29% of European digital health ventures having an Evidence Signal greater than 40, indicating robust clinical validation. Ventures in cardiovascular diseases, oncology, and musculoskeletal conditions exhibited strong clinical evidence, enhancing their attractiveness to investors and demonstrating their potential impact on patient outcomes. Read Galen Growth’s full report on the Evidence Signal and Clinical Strength in Digital Health.

Conclusion: Navigating the Tightrope of Innovation and Survival

The European digital health ecosystem in H1 2024 demonstrated resilience, driven by strategic investments in AI-driven patient and research solutions. More startups are pushing the limits of how long they can go before replenishing their cash reserves, likely resulting in more shutdowns. This underscores the critical importance of sustainable business models and efficient capital management.

Despite the overall decline in funding, specific clusters and therapeutic areas showed robust growth, underscoring the sector’s dynamic nature. Tools like Galen Growth’s Alpha Forecaster are crucial in navigating this complex landscape, providing investors with actionable insights to identify high-potential ventures.

As we move into the second half of 2024, the focus will likely remain on AI integration, biopharma partnerships, and clinical validation, setting the stage for sustained innovation and growth in the European digital health sector. With strategic investments and collaborations, the ecosystem is poised to overcome current challenges and continue its trajectory toward transformative healthcare solutions.

About Galen Growth

Galen Growth is a preeminent global digital health intelligence, analytics, and advisory firm. With a mission to unlock the full potential of the digital health ecosystem, Galen Growth provides unparalleled insights and data-driven strategies to stakeholders worldwide. Their extensive services include market analysis, venture capital trends, and strategic advisory, making them an invaluable partner for investors, startups, and corporates aiming to navigate and excel in the digital health landscape. By leveraging its comprehensive network and proprietary tools, Galen Growth bridges the gap between innovation and industry, fostering growth and facilitating impactful partnerships. For more information, visit https://www.galengrowth.com/ and https://www.galengrowth.com/about/

Source

This blog is based on the “Galen Growth Mid-Year 2024 Europe Digital Health Ecosystem Key Trends Report,” which features over 80 pages of data, charts, and insights. The report provides data-driven, non-biased, and non-hype analysis, unrivalled in its ability to go beyond just funding data. This comprehensive report is available to all our Premium customers.