Global Health Management Solutions funding reached $5.6 billion in 2025, with 83% flowing to AI-powered ventures — marking the permanent shift from experimental point solutions to an intelligence-driven healthcare operating layer.

KEY TAKEAWAYS

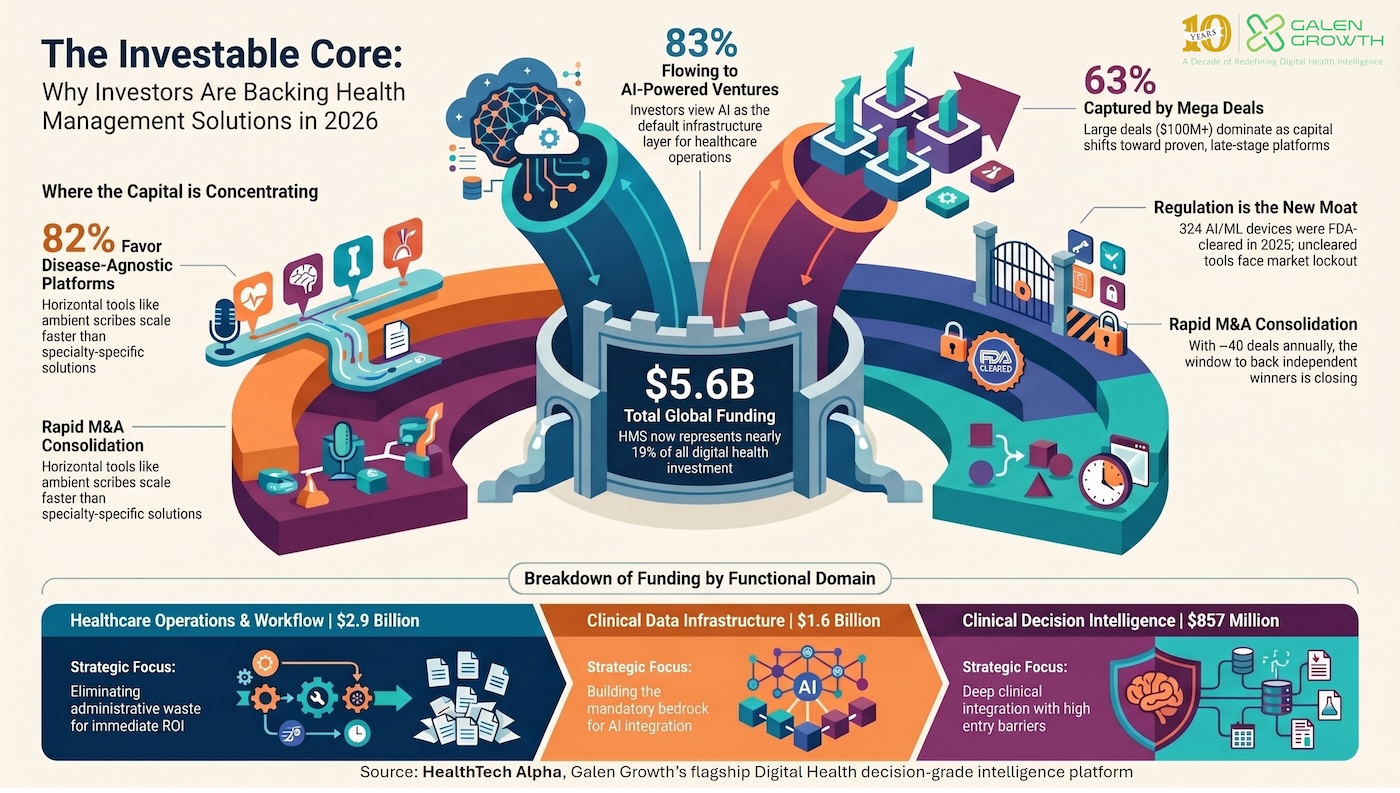

- The AI infrastructure play: Global Health Management Solutions funding reached $5.6B in 2025 — 18.8% of all digital health investment — with 83% ($4.4B) directed to AI-powered ventures.

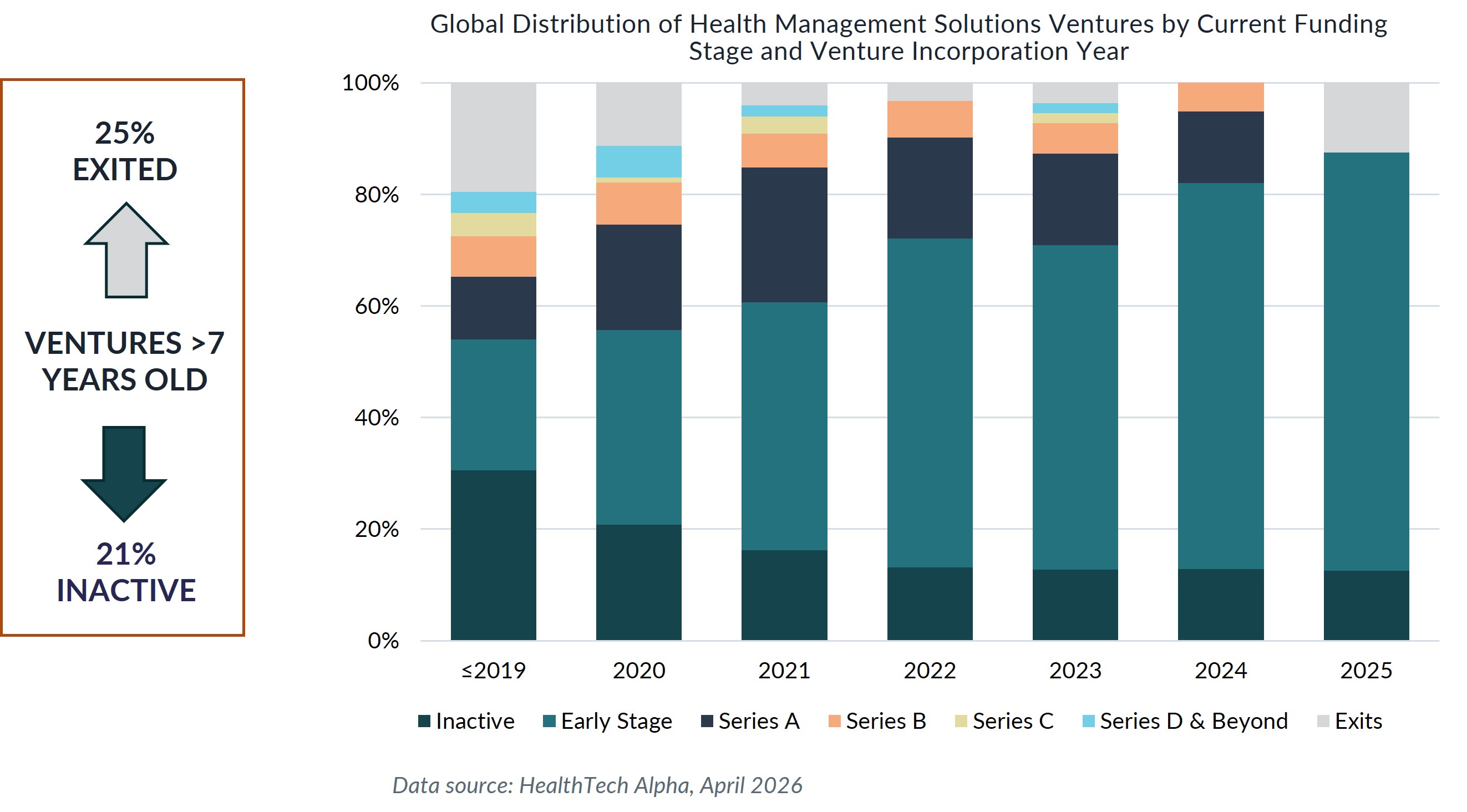

- A consolidated market: Among ventures older than 7 years, 25% have exited and 21% are inactive. M&A runs at 37–41 deals per year; 31 U.S. acquisitions in 2025 alone.

- Late-stage flight to quality: Mega deals ($100M+) captured 63% of Health Management Solutions funding in 2025. Average deal size tripled from $11.9M (Q1 2022) to $35.4M (Q1 2026).

- U.S. dominates; APAC offers asymmetric upside: The U.S. took $4.5B; APAC surged 87% year-on-year to $439M — the highest-growth greenfield opportunity globally.

- Regulation is the new moat: The FDA cleared 324 AI/ML devices in the Health Management Solutions cluster in 2025. Uncleared tools are being locked out of enterprise contracts.

The investment thesis: funding the AI life raft

Healthcare has been suffocating under a structural, labour-driven crisis for a decade. The average physician works 57.8 hours a week but spends only 27.2 hours on direct patient care — the remainder consumed by administrative overhead that is not merely an operational inefficiency, but a clinical risk that directly causes burnout and harms patient outcomes.

Capital has recognised this emergency. By deploying $5.6 billion into Health Management Solutions in 2025, the investment community is actively re-architecting healthcare from a strained, labour-driven model into an intelligence-driven system. This is not a speculative hype cycle. Health Management Solutions are the foundational, investable core of a new healthcare operating model — evidenced by the $4.4 billion (83% of total funding) that flowed directly to AI-powered ventures.

A maturing market: the winner-takes-most era

For venture and corporate investors, the Health Management Solutions space is defined by rapid maturation and rigorous consolidation. Investors are no longer building diverse portfolios of exploratory point solutions; they are backing a select few late-stage, proven platforms.

The data reveals a stark bifurcation between late-stage dominance and early-stage scarcity. Among ventures incorporated more than seven years ago, 25% have achieved successful exits while another 21% have gone inactive — a combined attrition rate approaching 50%. Acquirers — primarily large tech firms, EHR vendors, and health systems — are actively sweeping the board.

M&A volume has remained consistent at 37–41 deals per year. In the U.S. alone, there were 31 M&A exits in 2025: one successful acquisition nearly every 12 days. The mega deal ($100M+) has returned in force: 14 such deals in 2025 captured 63% of total Health Management Solutions funding. Average deal sizes tripled from $11.9M in Q1 2022 to $35.4M in Q1 2026.

Investment heavyweights: the top investors shaping the market

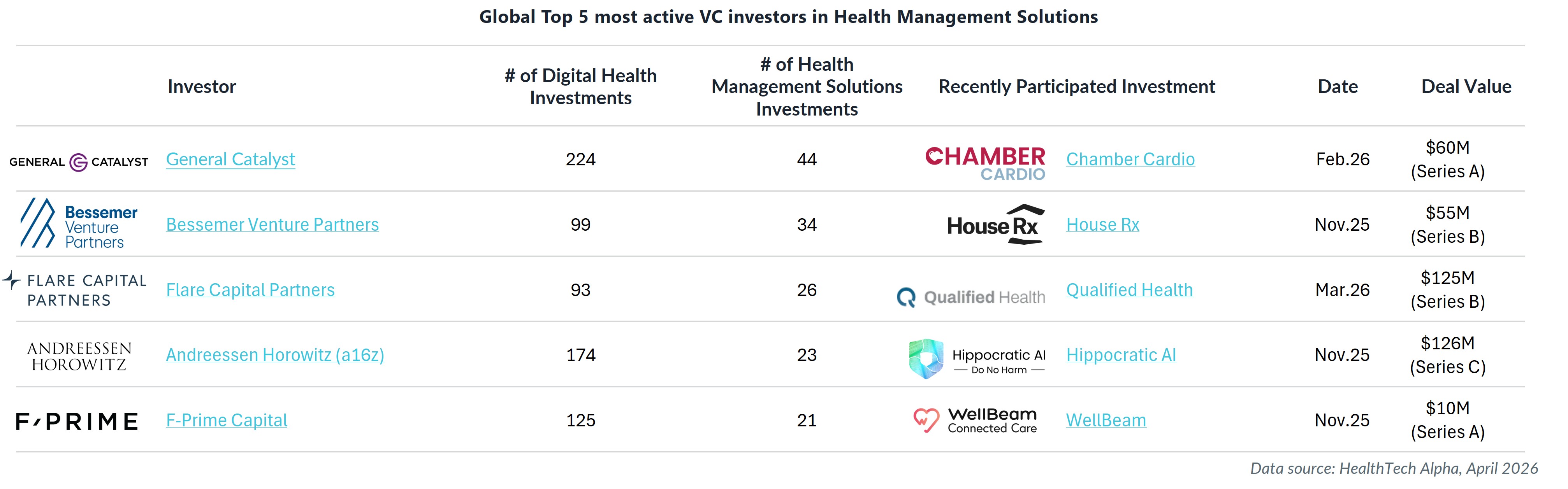

Health Management Solutions has graduated from niche curiosity to the mainstream core of top venture portfolios. General Catalyst leads globally: 44 of its 224 total digital health investments — a 20% concentration — are dedicated to this cluster. Other top investors actively consolidating the space include Bessemer Venture Partners (34 investments), Flare Capital Partners (26 investments), Andreessen Horowitz / a16z (23 investments), and F-Prime Capital (21 investments).

Recent high-profile activity illustrates the conviction: Flare Capital backed Qualified Health‘s $125M Series B in March 2026; a16z participated in Hippocratic AI‘s $126M Series C; Bessemer invested in House Rx‘s $55M Series B. The investment heavyweights are overwhelmingly backing platforms that solve administrative and operational bottlenecks at enterprise scale.

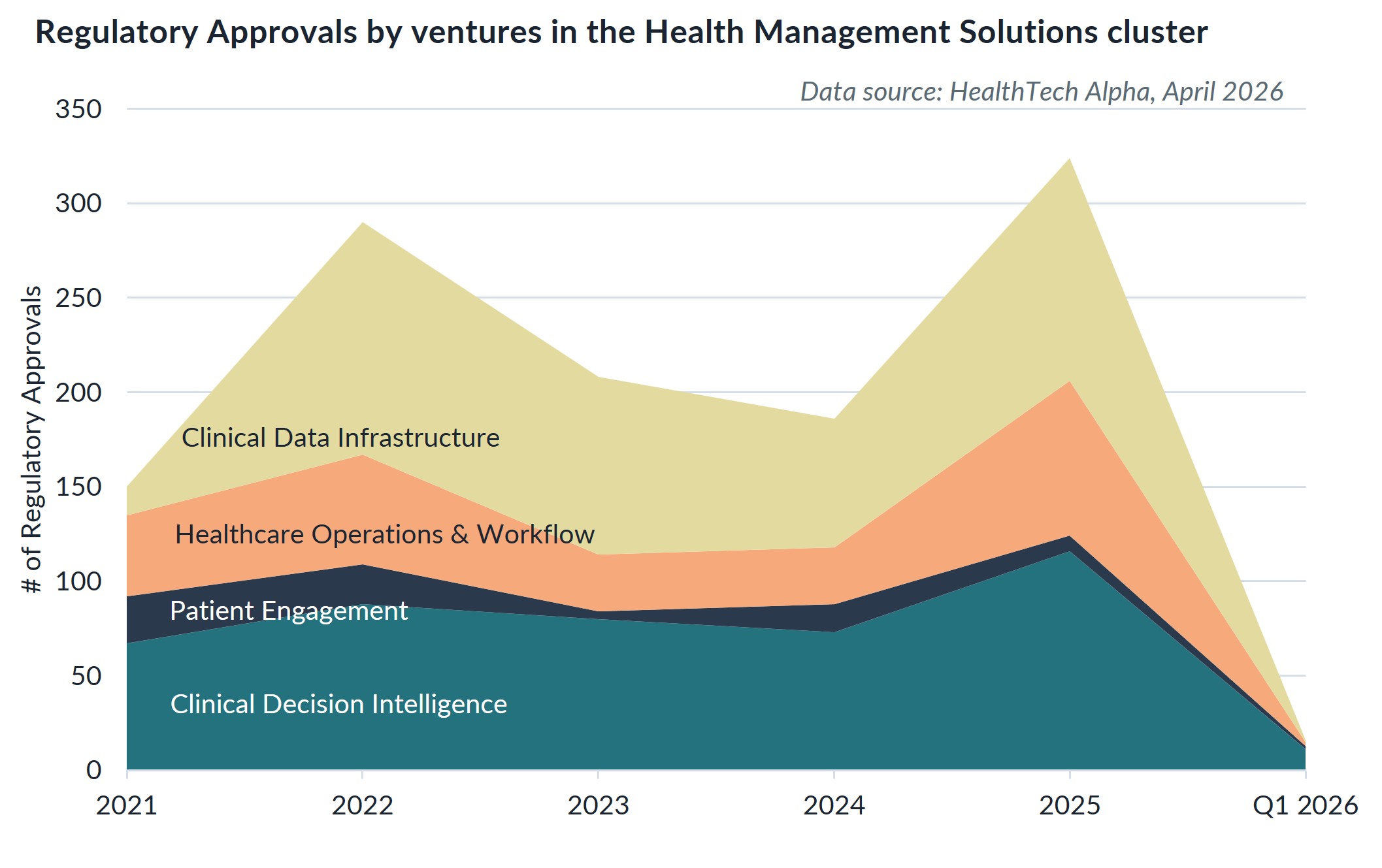

Where smart money is flowing: category focus

The four functional domains within Health Management Solutions attracted 2025 capital unevenly. Investors are prioritising categories that deliver immediate, board-level ROI.

- Healthcare Operations & Workflow — $2.9B (46%): The undisputed entry point for health systems globally. Eliminates administrative waste, provides instant capacity relief, and aligns with CFO procurement mandates.

- Clinical Data Infrastructure — $1.6B (29%): The mandatory bedrock for future AI integration. Investors recognise that clinical AI cannot be built on unstructured data.

- Clinical Decision Intelligence — $857M (18%): Requires a higher evidence bar but offers deep clinical integration and substantial barriers to entry.

- Patient Engagement — $144M (7%): The smallest slice today; value-based care expansion will likely drive future scale.

Horizontal scale over point solutions

For investors seeking massive scale, the data is unequivocal: disease-agnostic ventures captured 82% ($4.6B) of all Health Management Solutions funding in 2025. Horizontal platforms — ambient scribes, scheduling tools, workflow orchestration — offer faster time-to-market and a much easier path to enterprise-wide integration.

Among disease-specific plays, two stand out. Mental health tools received the highest specialty-area funding at $223M — serving a dual purpose of alleviating provider burnout while scaling patient access to behavioural care. Oncology received $150M, where multi-modal AI platforms (combining imaging, pathology, and genomics) are successfully transitioning from academic proofs-of-concept into enterprise deployments.

Global investment distribution: diverging strategies

United States ($4.5B; 1.8× YoY growth): With 41% of global Health Management Solutions ventures and over 19 unicorn-valuation companies in this cluster, the U.S. is the market. CFO-driven procurement prioritises 12-month ROI on efficiency, which is why Operations & Workflow captured 49% of all U.S. venture funding. The U.S. is the epicentre of aggressive M&A and late-stage scaling.

Europe ($610M; −15% YoY): The second-largest ecosystem (23% of global ventures) but a declining funding share. Europe’s publicly funded systems prioritise clinical integration, directing 47% of funding into Clinical Decision Intelligence — the highest proportion globally. Academic partnerships are the prerequisite for commercial scale. The UK ($285M) and Germany ($173M) remain the premier hubs.

Asia Pacific ($439M; +87% YoY): The most asymmetric, high-growth opportunity globally. Structural health worker shortages (India has fewer than 1 doctor per 1,000 rural residents) are forcing APAC systems to build their digital foundations from the ground up. Operations & Workflow and Clinical Data Infrastructure each received 34% of funding. Government and academic partnerships are the primary access mechanism for national tenders.

The new moats: regulation and real-world evidence

Barriers to entry have radically shifted over the past 24 months. First, FDA clearance is now table stakes. By end of 2025, the FDA had cleared approximately 1,430 AI/ML-enabled medical devices, with 324 approvals in the Health Management Solutions cluster in 2025 alone. Uncleared AI tools are being locked out of enterprise health system contracts. Regulatory complexity is a protective moat — not a deterrent — for the companies that achieve it.

Second, formal clinical trial volumes for Health Management Solutions tools are actively declining across all categories. This is not a quality issue: traditional randomized clinical trials (RCTs) are ill-suited for adaptive AI tools. The FDA’s Total Product Life Cycle (TPLC) framework embraces continuous Real-World Evidence (RWE) and EHR-based validation instead. This structural pivot disproportionately benefits mature incumbents who possess the large, diverse patient datasets required to generate RWE rapidly — further raising the entry bar for early-stage startups.

What this means

For investors: The window to back independent Health Management Solutions leaders is closing. With 37–41 acquisitions per year and EHR vendors expected to acquire 2–3 leading standalone AI tools by 2027, acquisition premiums available today will not exist in 24 months. Concentrate capital on late-stage, AI-native platforms with FDA clearance, multi-site enterprise deployments, and demonstrable CFO-level ROI.

For pharma and corporate partners: RWE generation is now the primary validation pathway, and the ventures accumulating large, diverse patient datasets are accumulating a structural advantage. Partnerships with horizontal AI platforms — particularly in Clinical Data Infrastructure — are the fastest route to RWE at scale.

For health systems and providers: Procurement teams are the new product gatekeepers. Uncleared AI tools and solutions that cannot map directly to EHR workflows are being excluded from enterprise contracts. Vendor selection criteria must now lead with FDA clearance status and EHR integration depth.

For digital health ventures: Disease-agnostic platforms are winning on funding and time-to-market. For those building specialty tools, mental health and oncology are the two sub-segments with demonstrated investor conviction and clear enterprise demand. Agentic AI orchestration — entering its first production-scale deployments in 2026 — represents the pre-consolidation layer with the most remaining upside.

Frequently asked questions

How much did Health Management Solutions receive in venture funding in 2025?

Health Management Solutions received $5.6 billion in global venture funding in 2025, representing 18.8% of all digital health investment. Of that total, $4.4 billion (83%) went to AI-powered ventures.

Which investors are most active in Health Management Solutions?

General Catalyst leads globally with 44 Health Management Solutions investments (20% of its total digital health portfolio), followed by Bessemer Venture Partners (34), Flare Capital Partners (26), Andreessen Horowitz / a16z (23), and F-Prime Capital (21). Recent rounds include Hippocratic AI’s $126M Series C (a16z) and Qualified Health’s $125M Series B (Flare Capital) in 2026.

What is driving the APAC funding surge in digital health?

APAC Health Management Solutions funding grew 87% year-on-year to $439M in 2025, driven by severe structural health worker shortages — India, for example, has fewer than 1 doctor per 1,000 rural residents. Governments are building digital health infrastructure from the ground up, with Operations & Workflow and Clinical Data Infrastructure each capturing 34% of regional investment.

Why are clinical trial volumes declining for Health Management Solutions tools?

Traditional Randomised Clinical Trials are ill-suited for adaptive AI tools that continuously improve with new data. The FDA’s Total Product Life Cycle (TPLC) framework actively embraces Real-World Evidence (RWE) and EHR-based validation as primary pathways, shifting the advantage to incumbents with large patient datasets.

What does the FDA clearance landscape look like for AI/ML medical devices?

By end of 2025, the FDA had cleared approximately 1,430 AI/ML-enabled medical devices in total, with a record 324 approvals occurring within the Health Management Solutions cluster in 2025 alone. FDA clearance is no longer a competitive differentiator — uncleared tools are being systematically excluded from enterprise health system procurement.

Data source and methodology

Data source: HealthTech Alpha by Galen Growth, 2025 full year and Q1 2026 (covering 1 January 2025 – 31 March 2026). Figures in USD. Excludes M&A, IPO, and post-IPO transactions unless stated. Partnership counts reflect headquartered-venture attribution. Some figures may be understated due to undisclosed deal terms.

RELATED GALEN GROWTH ANALYSIS

- Re-Architecting Healthcare Delivery with AI: Digital Health 2026 – Full Report

- The Administration Problem: How $5.6B Rewired Health Management Solutions in 2025

- AI in U.S. Healthcare Operations: Why Health Management Solutions Attracted $4.5B in 2025

How to cite this analysis

About Galen Growth

Galen Growth is the digital health intelligence firm behind HealthTech Alpha, the leading ontology-driven platform tracking the global digital health ecosystem. With operating entities in the US, Europe and Asia, we combine large-scale labelled data, auditable GenAI research and explainable analytics to advise pharma, medical device, insurance, health system, investor and startup clients.