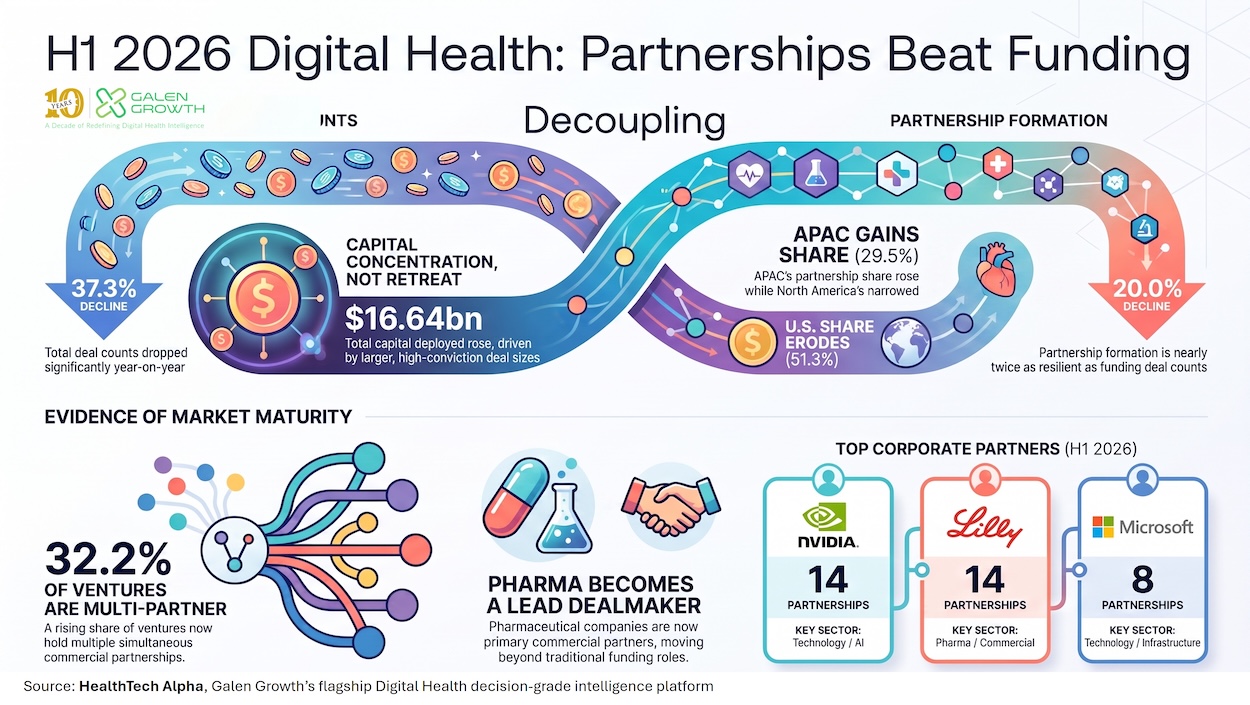

Partnership formation has decoupled from funding as digital health’s leading indicator. The pilot economy is ending — the market’s most reliable signal is now who ventures deploy with, not who funds them.

KEY TAKEAWAYS

- Partnerships have replaced funding as digital health’s leading indicator. Partnership formation has held far steadier than funding deal count through the current tightening cycle — a sign that enterprise demand is intact even as capital discipline increases.

- Capital is not leaving the market, it is concentrating. Fewer, larger funding rounds reflect investor selectivity, not investor retreat, and should be read that way in fundraising and diligence conversations alike.

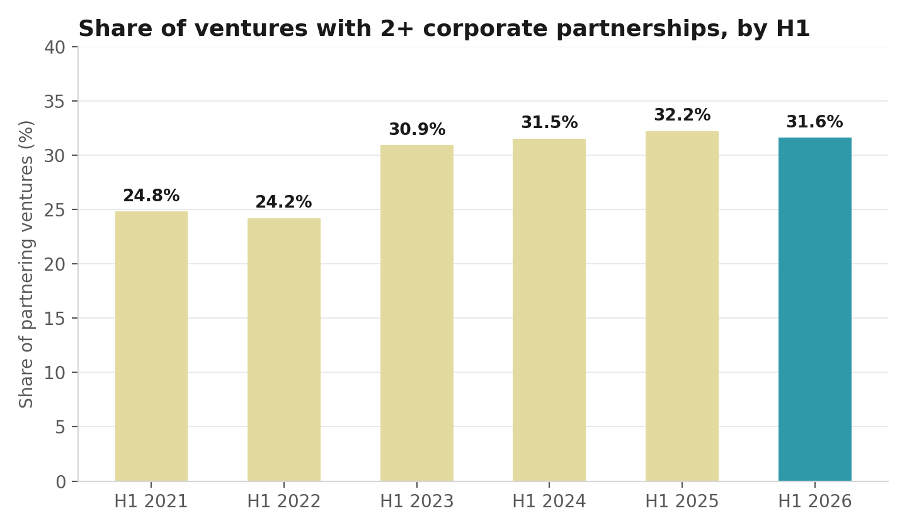

- The commercial centre of gravity has moved from pilots to scaled deployment. A rising share of ventures now hold multiple simultaneous corporate partnerships — evidence of repeat enterprise commitment rather than one-off experimentation.

- Enterprise demand is globalising beyond the U.S. APAC has captured a growing share of global partnership activity at the U.S.’s expense, with direct implications for how market-entry and expansion sequencing should be prioritised.

- Pharma is now a lead dealmaker in its own right, not just a funder. Several of the most active corporate partners in H1 2026 are pharmaceutical companies, confirming that partnerships have become pharma’s preferred mechanism for commercial-stage engagement with digital health.

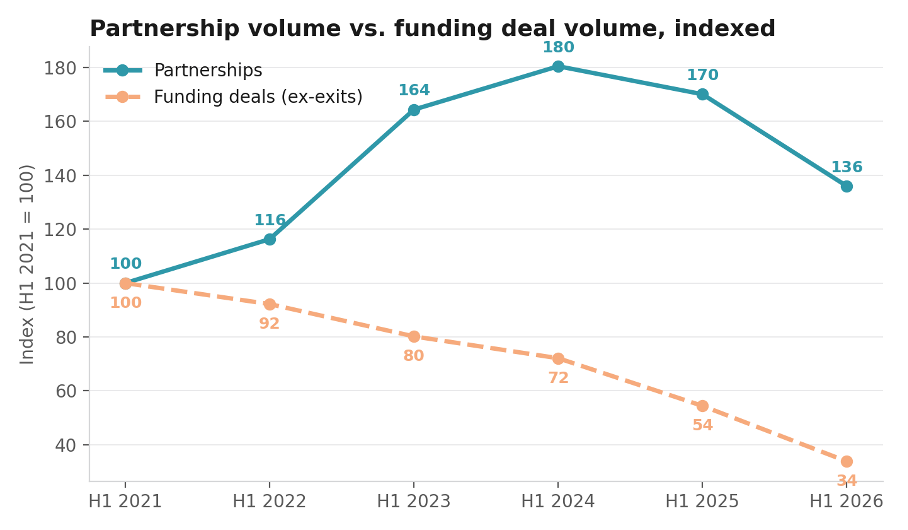

Every funding round invites the same diligence question: does this reflect genuine commercial pull, or a well-capitalised search for product-market fit? Answering that question by round size alone is now the weaker method available. HealthTech Alpha data through H1 2026 shows funding deal count contracting for a fifth consecutive half-year period even as partnership formation holds its ground — and a rising share of ventures are converting a single pilot into a portfolio of live commercial relationships.

Our analysis sets out why partnership data has become the sharper instrument for investors, corporates and ventures alike: the decoupling from funding, the geographic reallocation of enterprise demand, where partnerships concentrate by category, and the evidence that pilots are scaling rather than merely multiplying.

Partnerships have decoupled from funding as the market’s signal

The strategic implication precedes the data: when two indicators that used to move together diverge this sharply, the one that holds steadier is the one worth trusting. Funding deal count and partnership volume grew in step through 2021–2024 as digital health scaled. Since then, they have decoupled — and the direction of that decoupling favours partnerships as the more credible read on enterprise demand.

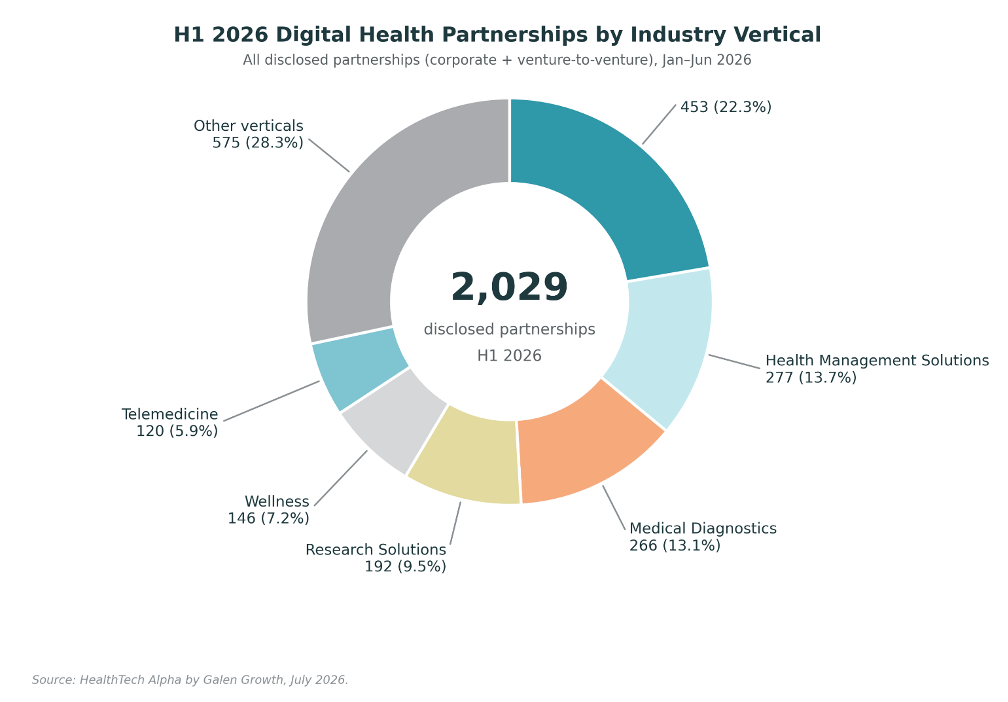

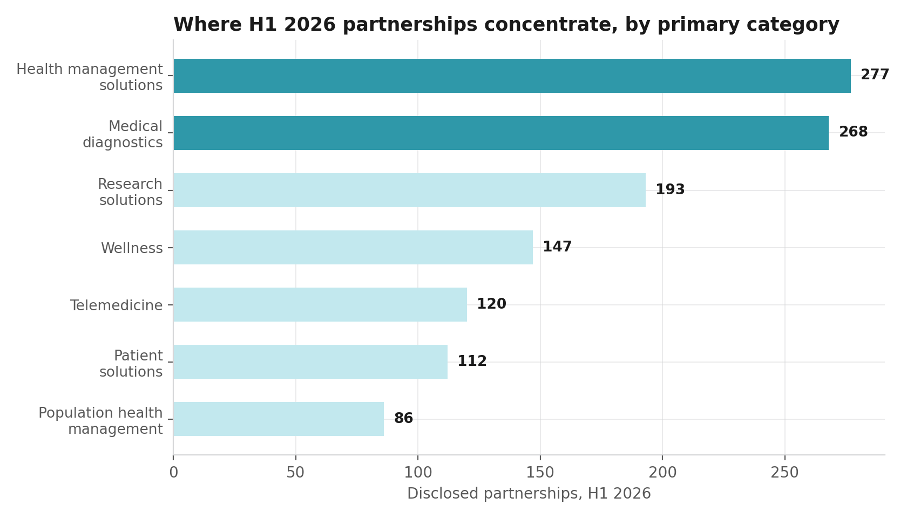

The 2,029 disclosed H1 2026 partnerships shown here include venture-to-venture deals (22.3% of the total) alongside the corporate partnerships this analysis focuses on throughout; corporate partnerships alone account for 1,582 of that total. Health management solutions and medical diagnostics remain the largest single verticals, consistent with the cluster concentration examined later in this piece.

In H1 2026, disclosed funding deal count fell to 525, down from 837 in H1 2025 — a 37.3% contraction. Yet capital deployed across those fewer deals rose, from $15.55bn to $16.64bn, pushing the average disclosed deal size up from roughly $18.6m to $31.7m. That is a late-cycle signature of conviction concentrating into fewer, larger, more scrutinised bets — not capital leaving the asset class.

Partnership formation fell 20.0% over the same window (1,582 vs 1,978) — roughly half the rate of decline in funding deal count. A partnership, by definition, requires a paying or piloting enterprise counterparty; its comparative resilience through a capital-markets tightening cycle is meaningful evidence that enterprise buyers, as distinct from investors, have not pulled back to the same degree.

The vertical mix behind H1 2026’s 2,029 disclosed partnerships adds a layer to the decoupling thesis: this resilience is not confined to a single niche. Venture-to-venture activity is the single largest bucket at 22.3% (453 deals), confirming that ventures are increasingly building commercial ecosystems with one another, not just with corporate buyers — a build-out that funding data, which only ever captures the investor side, cannot see. Read alongside the funding contraction, the breadth of this distribution — rather than concentration in one or two hot categories — is itself evidence that enterprise demand for digital health is broad-based, not a narrow bet by a handful of buyers.

Enterprise demand is broadening beyond the U.S.

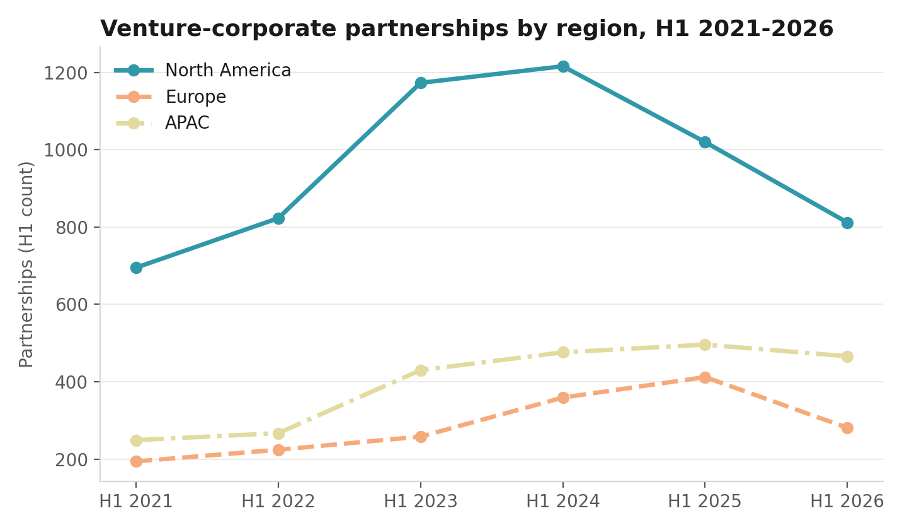

Where partnerships form matters as much as how many form. The U.S. remains the largest single market for venture-corporate partnerships, but its erosion is structural rather than cyclical — a genuine reallocation of enterprise demand that funding geography, still U.S.-weighted, does not yet reflect.

North America (primarily represented by the U.S.) accounted for 59.8% of global H1 partnership activity in 2021; by H1 2026 that share had narrowed to 51.3%, notwithstanding its absolute count remaining the largest of any region. APAC’s share expanded from 21.4% to 29.5% over the same period — a gain compounded across five consecutive H1 periods without a single contraction, a resilience the funding data does not show in any region over the same window. Europe’s share has held broadly flat, edging up from 16.7% to 17.8%.

Where is deployment actually concentrating — and who is leading it?

Partnership activity in H1 2026 is not evenly spread across the digital health landscape. It concentrates where the buyer is an operational function with a budget line — a health system, payer or pharma commercial team evaluating a tool for live use — rather than an innovation team running discovery projects.

Health Management Solutions and Medical Diagnostics together account for over a third of all disclosed H1 2026 partnerships — both categories where the natural buyer sits in operations, not R&D. Research Solutions ranks third, reflecting continued pharma appetite for AI-enabled discovery and clinical-development tooling, but the concentration in the top two operational categories supports the broader thesis: the centre of gravity has moved from R&D-adjacent experimentation towards workflow-embedded deployment.

The named-entity data reinforces the point. Nvidia and Eli Lilly and Company were the most active corporate partners across all clusters in H1 2026, each closing 14 disclosed venture partnerships, narrowly ahead of Microsoft and Daiichi Sankyo.

| Corporate partner | Disclosed H1 2026 partnerships | Most recent H1 2026 partner venture |

| Nvidia | 14 | Proxima |

| Eli Lilly and Company | 14 | Abridge |

| Microsoft | 8 | Caregility |

| Daiichi Sankyo | 7 | Waiv |

| OpenAI | 7 | Massive Bio |

| Novo Nordisk | 6 | Novi Health |

| Walmart | 6 | Teladoc |

| Athenahealth | 6 | Smart Meter |

The presence of Eli Lilly and Company, Daiichi Sankyo, and Novo Nordisk inside the top eight confirms this is not solely a technology-vendor phenomenon: large pharma is itself among the most active corporate dealmakers in the partnership market, treating partnerships as a commercial-deployment mechanism rather than an R&D side project.

Ventures are scaling partnerships, not just signing one

The final piece of evidence concerns depth, not breadth. If the pilot economy were genuinely ending, ventures should be graduating from a single corporate relationship to a multi-partner commercial footprint at a rising rate over time — and that is precisely what the data shows.

The share of ventures securing multiple corporate partnerships within a single H1 window rose from 24.8% in H1 2021 to 32.2% in H1 2025 — a structural climb sustained across five consecutive periods, not noise. That is the clearest available proxy for the shift from “a venture ran one pilot” to “a venture is being deployed across a portfolio of enterprise relationships.”

Notably, this scaling signal shows up more clearly in partnership repetition than in the funding-stage profile of partnering ventures: the average funding stage of ventures announcing partnerships has stayed broadly flat, and the share of later-stage ventures among partnering companies has if anything declined slightly as more early-stage ventures enter the partnership market. The “pilot economy ending” signal is therefore about deployment intensity per venture, not about later-stage ventures monopolising partnership activity — an important distinction for anyone using funding stage alone as a proxy for commercial readiness.

What this means

For investors: Partnership depth is a more discriminating diligence signal than round size in the current environment. The share of ventures securing two or more corporate partnerships within a single H1 window has expanded from 24.8% to 32.2% since 2021 — treat this cohort as a distinct, higher-conviction category, and weight it explicitly in sourcing and follow-on decisions rather than defaulting to valuation or round size as the primary filter.

For corporates: The concentration of H1 2026 partnership activity in health management solutions and medical diagnostics indicates where peer institutions are already committing budget to live deployment, not exploratory pilots. Corporates entering later than Nvidia, Eli Lilly and Company, Microsoft and the other most active dealmakers in this dataset are competing for scarcer, more mature counterparties — the window for favourable first-mover partnership terms in these categories is narrowing, not widening.

For digital health ventures: Capital is harder to raise and is concentrating into fewer, larger rounds — H1 2026 deal count fell 37.3% year-on-year even as average disclosed round size rose 70.6%. In that environment, a second or third corporate partnership now functions as a more persuasive proof point to prospective investors and enterprise buyers than a funding announcement alone, and should be positioned as such in fundraising narratives.

FAQ

Is digital health funding actually declining in 2026?

Deal count is declining sharply — down 37.3% year-on-year in H1 2026 — but total capital deployed is up 7.0% over the same period, because average disclosed round size has grown from roughly $18.6m to $31.7m. Fewer, larger rounds is the more accurate description than an overall funding decline.

Why treat partnerships as a leading indicator instead of funding?

Partnership volume has declined at roughly half the rate of funding deal count through the current tightening cycle (a 20.0% decline in H1 2026 versus a 37.3% funding deal decline). A partnership requires a paying or piloting enterprise counterparty, making it a closer proxy for demonstrated commercial demand than a financing event.

Which regions are gaining share of partnership activity?

APAC’s share of global H1 partnership volume rose from 21.4% in 2021 to 29.5% in 2026, the largest gain of any region, while North America’s share (primarily focused on the U.S.) fell from 59.8% to 51.3% over the same period.

Which corporates are most active in digital health partnerships right now?

Nvidia and Eli Lilly and Company were the most active named corporate partners in H1 2026, each with 14 disclosed partnerships, ahead of Microsoft, OpenAI, Daiichi Sankyo, Novo Nordisk, Walmart, and Athenahealth.

Does a rising multi-partner share prove pilots are converting to scale?

Not definitively. HealthTech Alpha tracks disclosed partnership announcements, not deployment scope or contract value, so a second partnership could reflect either expansion of an existing relationship or the start of a new pilot. The consistent multi-year rise in the multi-partner share is nonetheless the closest available proxy for the pilot-to-scale transition, and should be read as directional evidence rather than proof of contract-level scale.

Data source and methodology

Data source: HealthTech Alpha by Galen Growth, July 2026, covering venture-corporate partnership records and venture financing records globally. Funding analysis excludes M&A, IPO, Post-IPO Equity, SPAC, Pre-IPO, Secondaries and Delisted stages throughout, consistent with a focus on primary venture financing rather than exit activity.

Disclaimer: This analysis is provided solely for informational purposes and was prepared in good faith on the basis of public information available at the time of publication without independent verification. Numbers will be updated from time to time to reflect information identified after the event. Galen Growth does not guarantee or warrant the reliability or completeness of the data nor its usefulness in achieving any particular purposes. Galen Growth shall not be liable for any loss, damage, cost or expense incurred by any reason because of any person’s use or reliance on this report.

Related Galen Growth analysis

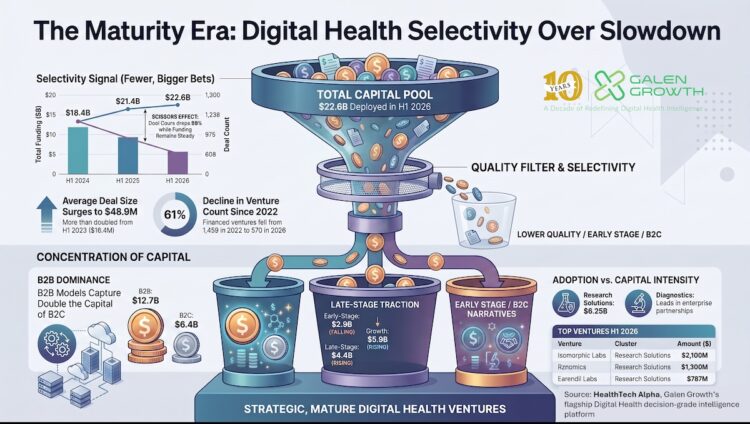

- Digital Health H1 2026: The Maturity Era

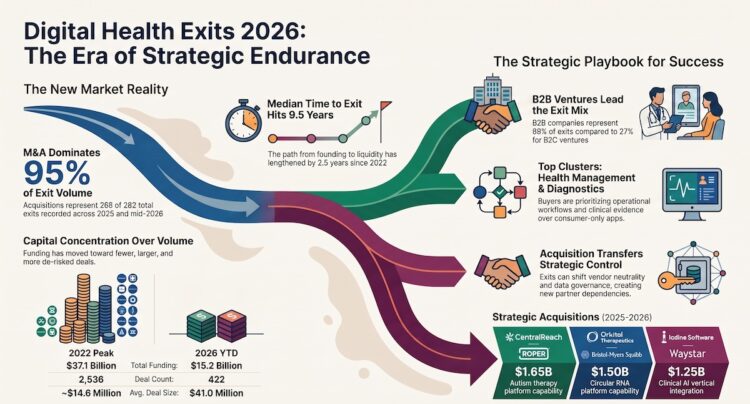

- 95% of Digital Health Exits Are Now M&A: 2026 Liquidity Shift

How to cite this analysis

About Galen Growth

Galen Growth is the Healthcare Innovation Intelligence company behind HealthTech Alpha. Built on proprietary data, AI-enabled workflows and expert insights, HealthTech Alpha delivers decision-grade intelligence that helps healthcare leaders identify opportunities, evaluate companies and make better strategic decisions.