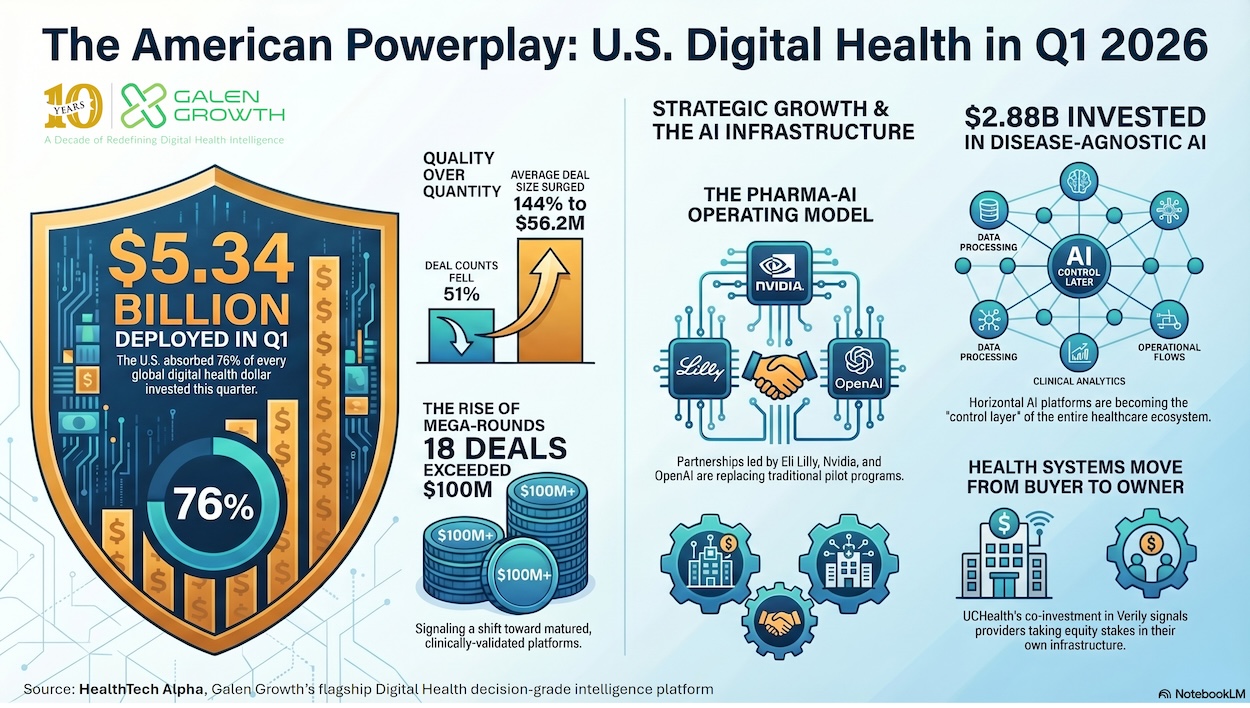

The United States absorbed 76% of global digital health funding in Q1 2026. Here’s what the data actually says.

TL;DR — U.S. DIGITAL HEALTH, Q1 2026 (FIVE THINGS TO KNOW)

- U.S. digital health VC totalled $5.34 billion across 105 deals in Q1 2026 — capturing 76% of global capital — with average deal size reaching $56.2M and 18 mega-rounds (≥$100M) driving concentration.

- Mental Health ($1.27B, 14 deals) and Neurology ($718M, 10 deals) lead the therapeutic charge; Obesity and Diabetes remain magnets for GLP-1-adjacent plays, while the Disease Agnostic AI layer absorbed $2.88B alone.

- Health Management Solutions dominates both venture capital ($892M, 19 deals) and corporate partnerships (80 of 362 US deals) — the convergence of capital and collaboration in a single cluster is the defining structural signal of Q1 2026.

- 362 U.S. corporate partnerships recorded in Q1 2026, led by Eli Lilly, OpenAI, Anthropic, and Nvidia — pharma-AI co-investment is no longer a trend; it is the operating model of the sector’s most ambitious players.

- U.S. exits were headlined by Talkspace ($865M M&A) and the Generate Biomedicines $400M IPO — the only digital health IPO globally — confirming M&A as the dominant exit route while the IPO window edges fractionally open.

The United States did not simply participate in the global digital health funding market in Q1 2026 — it absorbed it. While global capital contracted modestly in deal count, American ventures captured three-quarters of every dollar deployed worldwide. This is not a coincidence of geography; it is the compound result of a decade of ecosystem-building, deepening institutional knowledge among specialist healthcare investors, and the gravitational pull of an AI infrastructure boom that is restructuring how healthcare is delivered, paid for, and discovered.

What follows is a granular reading of the U.S. digital health ecosystem in Q1 2026 — covering venture capital flows, cluster and category dynamics, therapeutic area trends, corporate partnership patterns, and exit activity — drawn exclusively from HealthTech Alpha Premium.

Global Context

Global digital health venture funding reached $7.1 billion across 216 deals in Q1 2026 — a modest 6.6% year-on-year decline in deal value, but a sharp 83% surge in average deal size to $38.4 million, confirming accelerating capital concentration. Exit and post-exit activity added a further $5.1 billion, bringing total disclosed activity to $12.2 billion. Corporate partnerships contracted 21% year-on-year to 676 transactions globally, reflecting a deliberate industry-wide shift from broad pilot portfolios to fewer, deeper, commercially committed relationships. In a quarter defined by geopolitical turbulence, the United States acted as the ecosystem’s safe harbour — absorbing 76% of global VC capital — while Europe held steady and Asia-Pacific cooled significantly.

VC Funding: Concentration, Scale, Conviction

Key Q1 Stats for Digital Health Funding in the U.S.:

- Q1 2026 VC Funding (excl. exits): $5.34 billion ↑20% vs Q1 2025

- VC Deal Count (excl. exits): 105 deals ↓51% vs Q1 2025

- Average VC Deal Size: $56.2 million ↑144% vs Q1 2025 ($22.8M)

- VC Mega-Deals (≥$100M): 18 transactions vs 10 in Q1 2025

- Corporate Partnerships: 362 partnerships announced in Q1 2026

The headline figures tell a consistent story with global trends, but at American scale. Deal count is down; deal size is dramatically up. The 18 mega-rounds (≥$100M) of Q1 2026 account for a disproportionate share of the $5.34 billion deployed — a pattern that reflects both the maturation of the sector and the increasing dominance of specialist healthcare investors who are concentrating firepower rather than diversifying it.

“The U.S. digital health market in Q1 2026 is not writing more cheques — it is writing better ones. The bar for institutional capital has risen, and the companies clearing it are doing so on the strength of contracted revenue, clinical evidence, and workflow integration.”

Cluster & Category Trends

Health Management Solutions — Capital & Consolidation in One Cluster

Health Management Solutions leads U.S. VC with $892 million across 19 deals — and simultaneously records the greatest corporate partnership activity (80 of 362 U.S. partnerships). Verily ($300M Series E, led by Series X Capital), Qualified Health ($125M Series B), and Zarminali Health ($110M Series A) exemplify the cluster’s breadth — from AI-powered analytics platforms to hospital workflow optimisation tools.

Patient Solutions & Telemedicine — The Clinical Delivery Duopoly

Patient Solutions ($673M, 12 deals) and Telemedicine ($655M, 11 deals) together represent $1.33 billion. Within Patient Solutions, Digital Therapeutics leads with $455M across 8 deals, anchored by Science Corporation ($230M Series C). In Telemedicine, Talkiatry ($210M Series D, a16z-led) and Grow Therapy ($150M Series D, Goldman Sachs/Sequoia) together raised $360M — confirming the sustained institutionalisation of mental health telehealth.

Health InsurTech — Large Rounds, Thin Deal Count

Health InsurTech secured $561M across just 5 deals — the highest average deal size of any cluster at $112M. Devoted Health‘s $366M Series F (Google Ventures, Morgan Health) and Collective Health‘s $110M Series F (Mubadala, Founders Fund, NEA) anchor concentrated bets on value-based insurance infrastructure.

Top 15 U.S. VC Deals — Q1 2026

| # | Venture | Category | Stage | Amount | Lead Investors |

|---|---|---|---|---|---|

| 1 | WHOOP | Wearables | Series G | $575M | Mubadala, QIA, IVP, Mayo Clinic Ventures |

| 2 | Devoted Health | Health Insurance | Series F | $366M | Google Ventures, Morgan Health, VanEck |

| 3 | Verily | Prescriptive Analytics | Series E | $300M | Alphabet, UCHealth, Series X Capital |

| 4 | OpenEvidence | Health Info Platform | Series D | $250M | DST Global, Thrive Capital, Nvidia, Sequoia |

| 5 | Science Corporation | Digital Therapeutics | Series C | $230M | Khosla Ventures, Lightspeed |

| 6 | Talkiatry | Teleconsultation | Series D | $210M | a16z, Left Lane Capital, Perceptive Advisors |

| 7 | eMed | Disease Management | Series A | $200M | Aon, Joe Lonsdale, Antonio Gracias |

| 8 | Zipline | On-demand Delivery | Series H | $200M | Fidelity, Tiger Global, Valor Equity |

| 9 | Claroty | Cybersecurity | Series F | $150M | Golub Growth |

| 10 | Grow Therapy | Teleconsultation | Series D | $150M | Goldman Sachs Alternatives, Sequoia, TCV |

| 11 | Solace | Healthcare Navigation | Series C | $130M | IVP, Menlo Ventures, SignalFire |

| 12 | Qualified Health | Hospital | Series B | $125M | NEA, Flare Capital, Transformation Capital |

| 13 | Garner Health | Medical Concierge | Series D | $118M | Kleiner Perkins, Kaiser Permanente Ventures |

| 14 | Zarminali Health | Hospital | Series A | $110M | General Catalyst, Healthier Capital |

| 15 | Collective Health | Healthcare Navigation | Series F | $110M | Mubadala, Founders Fund, NEA |

Therapeutic Area Trends

The Disease Agnostic solutions absorbed $2.88 billion across 47 deals, underscoring how much of Q1 2026’s capital is flowing into horizontal platforms rather than condition-specific solutions.

Mental Health — The Sector’s Most Consistent Conviction Theme

Mental Health attracted $1.27 billion across 14 deals — the most therapeutically concentrated funding pool of Q1 2026. Talkiatry ($210M) and Grow Therapy ($150M) represent the telehealth delivery layer. The 14-deal spread indicates broad-based conviction, not megadeal distortion.

Sleep & Neurology — The Brain-Body Axis Investment Thesis

Sleep attracted $1.14B (7 deals) and Neurology $718M (10 deals) — together $1.86B reflecting the convergence of wearables, neural interfaces, and digital therapeutics. Science Corporation‘s $230M brain-computer interface platform anchors the Neurology cluster.

Obesity & Diabetes — GLP-1 Infrastructure Lives On

Obesity-focused ventures attracted $300M and Diabetes $313M in Q1 2026. The companies building GLP-1 monitoring, adherence, and outcome platforms are increasingly valuable to both pharmaceutical manufacturers and payers, as the post-prescription management gap widens.

Partnerships & Key Trends

362 corporate partnerships were recorded for U.S. digital health ventures in Q1 2026. Health Management Solutions leads with 80 transactions — 1.6x more than the second-placed Medical Diagnostics (51). Research Solutions (42) and Patient Solutions (30) round out the top four, demonstrating that the partnership engine fires hardest where enterprise buyers see the most immediate operational relevance.

The Pharma-AI Alliance: The Defining Partnership Trend of Q1 2026

Eli Lilly is the most active pharma partner in the first quarter of 2026 across multiple clusters. Novo Nordisk has concentrated partnership activity in Telemedicine — a direct adjacency to its GLP-1 commercial infrastructure. On the technology side, OpenAI and Anthropic each recorded three U.S. digital health partnerships, while Nvidia spans both Health Management Solutions and Medical Diagnostics. Pharma-AI co-investment is no longer an emerging trend: it is the operating model of the sector’s most strategically sophisticated players.

Health Systems as Integrators, Not Just Buyers

UCHealth’s co-investment in Verily‘s $300M Series E — alongside Alphabet — signals a new category of health system behaviour: not merely procuring digital health solutions, but taking equity stakes in the platforms they intend to run on. This buyer-as-investor model is the rational response to partnership fatigue and the clearest leading indicator of where health system procurement is heading.

Exit Activity: U.S. Q1 2026

| Venture | Category | Exit Type | Value | Notes |

|---|---|---|---|---|

| Talkspace | Teleconsultation | M&A | $865M | Largest US exit Q1; mental health telehealth platform |

| Generate Biomedicines | Drug Discovery | IPO | $400M | Only digital health IPO globally in Q1 2026; generative AI + drug discovery |

| Care.com | Home Healthcare | M&A | $320M | PE change of ownership; home care platform consolidation |

| Torch | EHR / PHR | M&A | $60M | AI health data company; strategic acquisition |

Talkspace’s $865M acquisition confirms that mental health telehealth platforms command substantial strategic premiums. Care.com’s $320M PE change of ownership reflects ongoing rationalisation of home care infrastructure. Generate Biomedicines’ $400M IPO — the only digital health public listing globally in Q1 2026 — is a bellwether for AI-native biotech: the public markets will price platforms that have moved from computational promise to credible clinical pipelines, but the gate is narrow. In December 2025, Freenome announced a planned SPAC transaction, but it has not yet started trading on the NASDAQ under the ticker symbol FRNM.

What It Means: Investors, Ventures & Corporates

📈 For Investors

Q1 2026 confirms that diversification is no longer a winning strategy. With $5.34B across 105 deals and 18 mega-rounds dominating capital, returns are driven by conviction in a few clusters—especially Health Management Solutions, Telemedicine, and Health InsurTech. The pattern is clear: capital flows to companies with contracted revenue, clinical validation, and real workflow integration—not future potential. Meanwhile, $2.88B into disease-agnostic AI signals that horizontal platforms are becoming the control layer of healthcare.

Alpha now requires deep domain expertise in reimbursement, clinical pathways, and enterprise sales. Generalist approaches will increasingly underperform – the HealthTech Alpha taxonomy (69 categories, 18 clusters, 19 technology types) is the analytical infrastructure that makes this level of conviction investable.

🏥 For Digital Health Ventures

The bar has fundamentally shifted from promise to proof. The companies raising the largest rounds are not earlier—they are more commercial, with enterprise contracts and recurring revenue already in place. Partnerships alone are no longer enough. With corporate activity down 21% globally, buyers are prioritising fewer, deeper relationships. Ventures must convert traction into contracted ARR and measurable outcomes to stay in the core portfolio.

In this market, success depends on being embedded in workflows, not adjacent to them. Those that fail to integrate risk being deprioritised—regardless of technology quality.

🤝 For Corporates (Pharma, Device, Health Systems)

The shift from pilots to commitment is underway. With fewer but more strategic partnerships, corporates are concentrating resources on platforms that deliver operational and financial impact. For pharma, AI partnerships are now the operating model, and early movers are securing positions that will be difficult to replicate. For health systems, co-investment models like UCHealth–Verily signal a move from procurement to ownership.

The implication is simple: integration defines relevance. Partners that are not embedded in workflows—and tied to outcomes—will be left behind.

| About the Data: HealthTech Alpha Premium Every data point in this analysis is drawn exclusively from HealthTech Alpha Premium, Galen Growth’s proprietary intelligence platform for the global digital health ecosystem. In a world flooded with AI-generated market commentary and synthetic data, HealthTech Alpha is built differently: human expert curation combined with AI-assisted enrichment, applied to a purpose-built taxonomy of 69 categories, 18 clusters, and 19 technology types.In the GenAI era, this distinction is not cosmetic — it is the difference between analysis you can publish and analysis you should not. General-purpose AI tools hallucinate deal data, misattribute funding rounds, and confuse funding stages. HealthTech Alpha Premium is verified, structured, updated in near-real time, and designed for machine-readable analysis and human-guided strategy. It is the only dataset we trust, the only one we publish from, and the one that every serious investor, venture, and corporate in digital health should be using as their primary intelligence layer. |

| Read the Full Galen Growth Q1 2026 Analysis This op-ed surfaces the headline trends. The full Galen Growth Q1 2026 report goes deeper — global breakdowns, venture-by-venture profiles, investor network mapping, therapeutic deep-dives, and curated strategic watchlists. >> Access the Full Report at galengrowth.com << |

Methodology & Data Note

All data sourced exclusively from HealthTech Alpha Premium by Galen Growth. Q1 2026 covers 1 January – 31 March 2026. VC figures exclude M&A, IPO, SPAC, and Post-IPO transactions. Partnership counts reflect U.S.-headquartered ventures only. Funding amounts in USD. Some figures may be understated due to undisclosed deal terms. © 2026 Galen Growth. All rights reserved.