The European Commission’s new Scaleup Europe Fund is being dismissed as too small. The criticism is understandable. But HealthTech Alpha data suggests the real issue is not whether €5 billion is enough. It is whether Europe can finally build the late-stage capital infrastructure required to keep its winners European.

KEY TAKEAWAYS

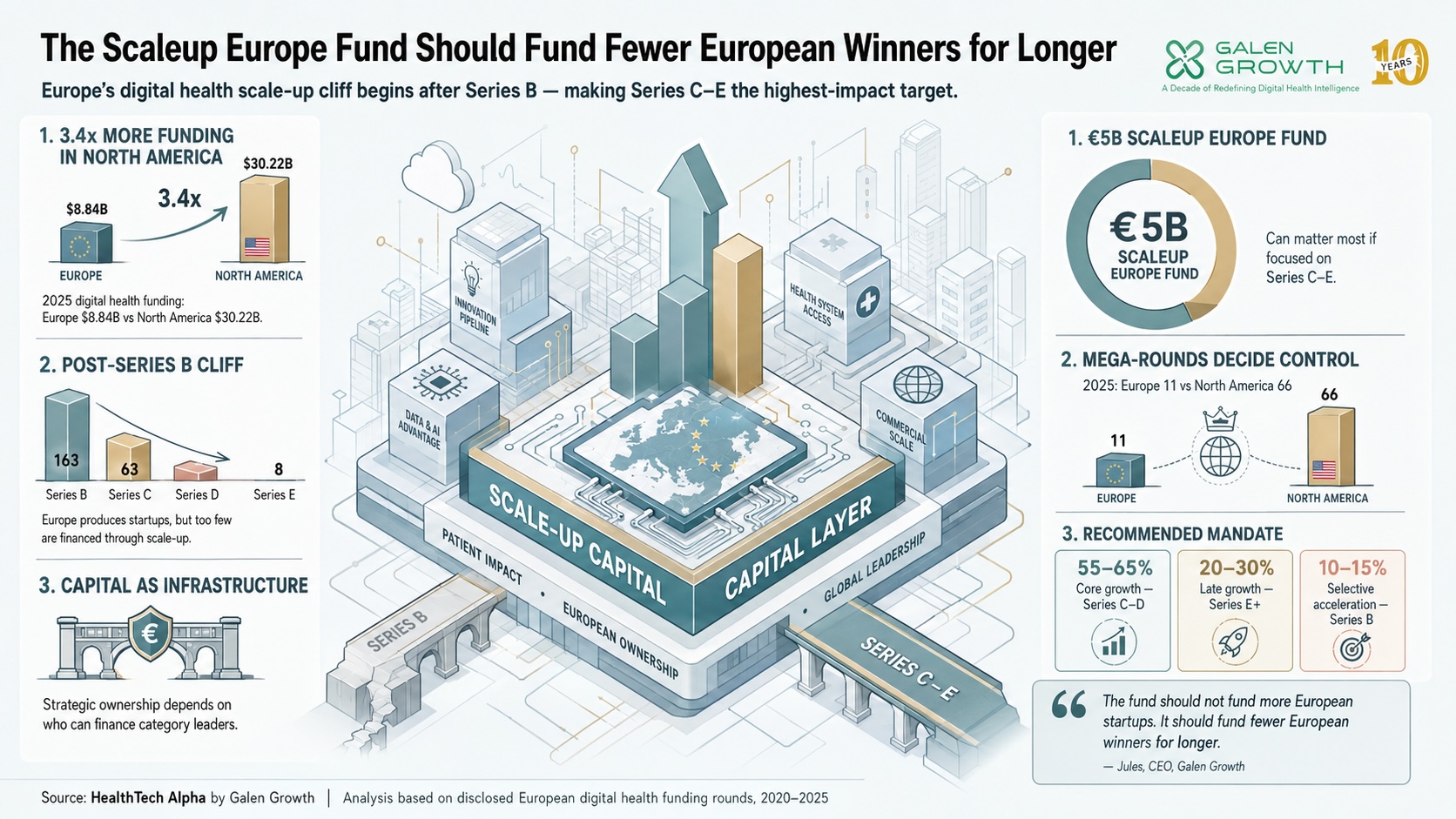

- The European Commission has announced support for the new Scaleup Europe Fund, anchored by EQT, with a target size of €5 billion.

- HealthTech Alpha data shows that, in 2025, the United States attracted 3.5x more disclosed digital health VC funding than Europe.

- In 2025, the United States attracted 3.5x more disclosed digital health VC funding than Europe; across 2020-2025, the cumulative gap was approximately 5x.

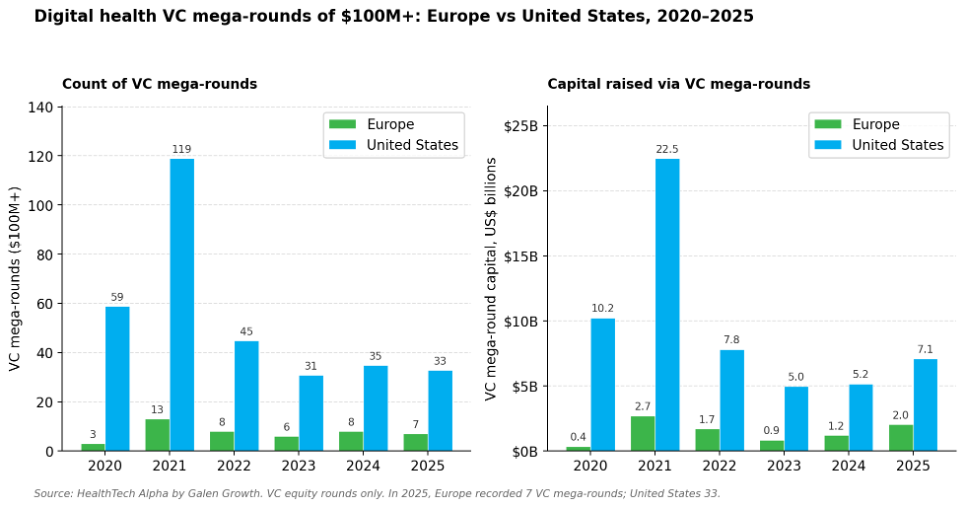

- Europe recorded 7 disclosed digital health VC mega-rounds of $100 million or more in 2025, compared with 33 in the United States.

- HealthTech Alpha data from 2020–2025 shows Europe’s scale-up cliff begins after Series B: Europe recorded 163 Series B rounds, but only 63 Series C rounds, 18 Series D rounds, and 8 Series E rounds.

- Galen Growth recommends that the Scaleup Europe Fund focus primarily on Series C to Series E European scale-ups, with selective Series B exposure, rather than dispersing capital across Seed and Series A.

Europe’s critics are right — and still missing the point

The immediate reaction to the European Commission’s announcement was predictable.

€5 billion? That’s it?

Compared with the scale of American private equity, sovereign AI infrastructure spending, or the balance sheets of hyperscalers, the number appears modest. A single late-stage AI company in the United States can command valuations many times larger than the Scaleup Europe Fund’s target size. A single major platform company can add or lose more than €5 billion in market value in a single trading session.

On the surface, the criticism lands.

Europe’s scale-up financing gap is real. The continent repeatedly succeeds at producing scientific talent, technical founders, and early-stage innovation, only to watch many of its most strategically important companies turn to U.S. capital markets, U.S. acquirers, or U.S.-led investor syndicates when serious scale financing becomes necessary.

But the obsession with whether €5 billion is “enough” risks misunderstanding what was actually announced.

The significance of the fund is not only numerical. It is institutional.

For nearly two decades, Europe treated industrial policy and venture capital as separate conversations. Brussels regulated markets. Private capital funded innovation. Sovereignty was discussed primarily in the context of competition law, privacy frameworks, procurement rules, or trade policy.

That model no longer works in an era where capital itself determines geopolitical power.

Source: HealthTech Alpha by Galen Growth, VC equity rounds announced from 1 January 2020 to 31 December 2025. Excludes IPO, SPAC, M&A, post-IPO, debt, grant, and other non-VC transactions.

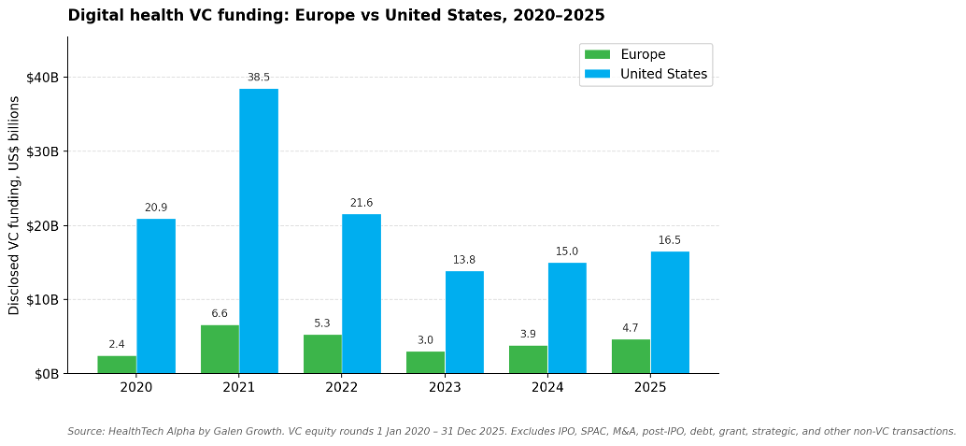

Europe is not short of digital health ventures. It is short of capital density. In 2025, the United States attracted 3.5x more disclosed digital health VC funding than Europe. Across 2020-2025, the cumulative gap is approximately 5x.

Europe’s real problem was never startup creation

Europe does not suffer from a startup creation problem.

The continent produces world-class technical founders at remarkable efficiency. It has deep university systems, strong public research infrastructure, and increasingly sophisticated venture ecosystems across Paris, Stockholm, Berlin, Amsterdam, London, Munich, Copenhagen, Barcelona, and Helsinki.

The problem emerges later.

HealthTech Alpha’s digital health funding data makes the pattern visible. In 2020, Europe recorded 632 disclosed digital health VC funding rounds, while United States recorded 1,175. In 2021, Europe again recorded 632 rounds, while United States recorded 1,507. Even during the post-2021 venture correction, Europe remained active, with 659 rounds in 2022, 622 in 2023, and 594 in 2024.

That is not ecosystem absence.

It is financing asymmetry.

The capital gap becomes especially visible when comparing total dollars. United States attracted $89.29 billion in digital health VC funding in 2021, compared with $13.18 billion in Europe. In 2025, the gap narrowed in absolute terms but remained substantial: $30.22 billion in United States versus $8.84 billion in Europe.

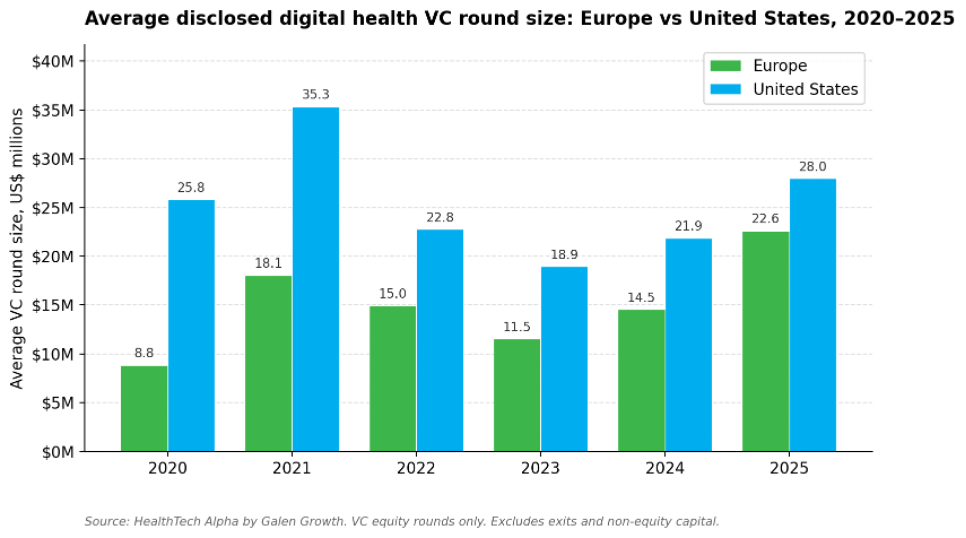

Europe has historically struggled to finance the transition from promising company to globally dominant platform business. Not because capital does not exist in aggregate, but because it is fragmented, conservative, and structurally less willing to concentrate risk around potential category leaders.

American capital markets tolerate concentration. Europe prefers diversification.

American pension funds and endowments have historically allocated more aggressively to venture and growth equity. European institutional allocators remain more cautious.

American industrial policy increasingly deploys direct financial power. Europe traditionally preferred regulatory architecture.

The result is visible across sectors from AI to semiconductor infrastructure to digital health to climate technologies: Europe incubates innovation, but too often exports the economic upside.

That is the context in which the Scaleup Europe Fund matters.

The European Commission is implicitly acknowledging that strategic autonomy cannot exist without strategic ownership.

Source: HealthTech Alpha

Europe can generate venture activity. The harder question is whether it can finance escape velocity.

The Scaleup Europe Fund should not fund more startups. It should fund fewer winners for longer.

The most important strategic decision facing the Scaleup Europe Fund is not only its size. It is its stage focus.

A €5 billion fund can be meaningful if it is concentrated at the point of maximum market failure. It can be diluted quickly if it is spread too broadly across the venture lifecycle.

For European digital health, HealthTech Alpha data points to a clear recommendation:

Galen Growth recommends that the Scaleup Europe Fund focus primarily on Series C to Series E European scale-ups, with selective Series B exposure for companies already demonstrating exceptional maturity, evidence, commercial traction, and strategic relevance.

The fund should not become a Seed or Series A vehicle.

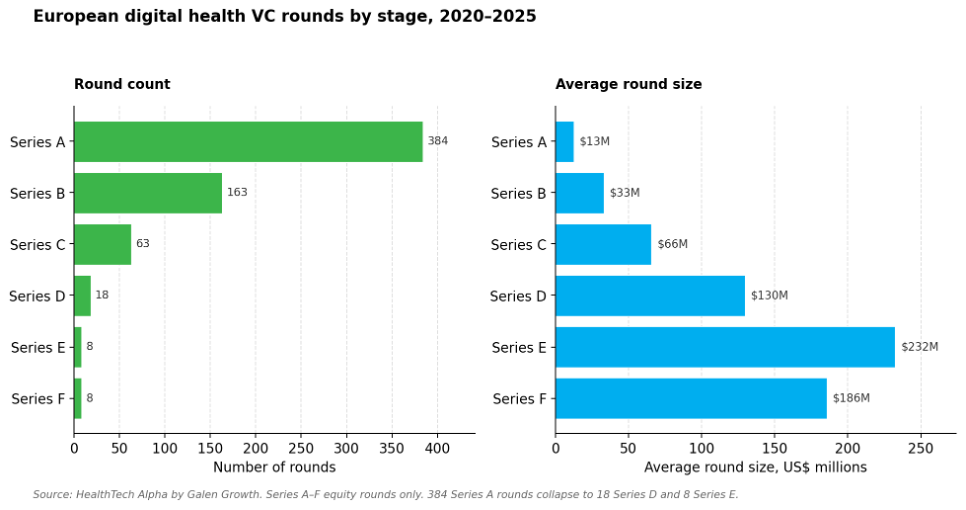

Europe already has meaningful activity at those stages. From 2020 to 2025, HealthTech Alpha recorded 384 European Series A digital health VC rounds, attracting $4.82 billion in disclosed funding. Series A matters, but it is not where Europe’s sovereignty problem is most acute.

The cliff appears later.

Europe recorded 163 Series B rounds over the same period, attracting $5.40 billion. But by Series C, the count falls to 63 rounds. By Series D, it falls to 18. By Series E, only 8.

That is where promising companies either obtain escape velocity or become dependent on external capital structures.

A strategic European scale-up fund should therefore be designed around concentration rather than coverage. The goal should not be to touch as many companies as possible. It should be to ensure that Europe’s highest-potential companies can raise sufficiently large rounds without being forced prematurely into U.S.-led financing, distressed M&A, or relocation pressure.

The right model is fewer companies, deeper capital, and longer support.

Source: HealthTech Alpha by Galen Growth.

Europe’s scale-up cliff begins after Series B. The strategic financing gap is not company creation; it is sustaining winners through Series C, Series D, and Series E.

A practical mandate for EQT: concentrate capital where Europe loses ownership

The Scaleup Europe Fund should be judged by whether it changes outcomes for companies that already have proof points, not whether it maximises the number of logos in its portfolio.

For digital health, that means prioritising companies that have:

- validated commercial demand,

- credible clinical or real-world evidence,

- regulatory or reimbursement progress,

- cross-border expansion potential,

- strategic relevance to European health systems,

- and the ability to become category leaders, not only attractive acquisition targets.

The mandate should therefore be staged around three capital buckets.

| Mandate bucket | Indicative share of fund | Stage focus | Strategic purpose |

| Core growth | 55–65% | Series C–D | Finance European category leaders through commercial scale-up |

| Late growth / pre-IPO | 20–30% | Series E+ | Prevent forced migration to U.S. capital markets or premature exits |

| Selective acceleration | 10–15% | Series B | Back exceptional ventures before the growth-stage funding gap appears |

This structure would enable the fund to lead or co-lead large rounds, rather than merely participate as a symbolic investor.

That distinction is crucial.

A passive minority cheque does not solve Europe’s strategic capital problem. Lead investors shape round pricing, syndicate composition, board dynamics, hiring ambition, commercial expansion, exit timing, and eventually listing geography.

If Europe wants ownership retention, it needs European capital capable of leading.

For digital health, that likely means the Scaleup Europe Fund should be prepared to write $50 million to $100 million initial cheques at Series C, and $100 million to $200 million cheques at Series D and Series E, with meaningful reserves for follow-on rounds.

The fund’s purpose should not be to fill every gap.

It should be to prevent Europe’s most strategically important companies from hitting a capital ceiling just as they begin to matter globally.

Sovereignty is decided at the growth stage, not the seed stage. In 2025, Europe recorded 7 disclosed digital health mega-rounds of $100 million or more; United States recorded 33.

Why €5 billion may be intentionally small

There is another possibility critics are overlooking: perhaps the fund is small because Europe is testing political viability before testing financial scale.

A €50 billion announcement would have generated headlines. It may also have generated immediate resistance from member states already divided on industrial spending priorities, fiscal integration, defence spending, energy transition, and strategic sovereignty.

Europe rarely moves through revolutionary leaps. It moves through institutional precedent.

The European Central Bank evolved this way. Pandemic recovery financing evolved this way. Joint energy coordination evolved this way. Defence procurement may evolve this way.

The Scaleup Europe Fund may follow the same pattern: establish the legitimacy of pan-European strategic capital first, then expand it once political resistance softens and operational credibility is established.

That would make this less a final-state solution and more a proof of concept for a new European financing doctrine.

And if that is the objective, €5 billion may be sufficient.

Not sufficient to close the gap.

Sufficient to establish the mechanism.

HealthTech Alpha data shows that, in 2025, the United States attracted 3.5x more disclosed digital health VC funding than Europe. One €5 billion pan-European scale-up fund will not transform the entire technology financing landscape. But a €5 billion vehicle focused on Series C to Series E could materially change the financing environment for the subset of companies that matter most for strategic ownership.

That is the distinction.

If spread thinly across the whole startup funnel, €5 billion is too small.

If concentrated behind Europe’s most credible scale-ups, it becomes a serious instrument.

The first serious pan-European growth capital vehicle need not be the last. It needs to prove that Europe can coordinate strategic ownership at scale.

The deeper question: what kind of Europe is being built?

The real divide exposed by the Commission’s announcement is philosophical.

One side argues Europe cannot compete unless it immediately matches American and Chinese capital firepower at massive scale.

The other argues Europe’s first challenge is institutional alignment: building mechanisms capable of deploying strategic capital coherently before dramatically increasing the amounts involved.

Both arguments contain truth.

But there is also a more uncomfortable reality beneath them: Europe’s challenge has never been purely financial. It has been cultural.

Europe has historically been more comfortable constraining market power than creating it. More comfortable regulating global platforms than producing them. More comfortable discussing innovation than concentrating ownership around it.

Yet the global economy increasingly rewards scale concentration.

Artificial intelligence infrastructure, semiconductor supply chains, quantum computing, defence technologies, and next-generation healthcare platforms all exhibit winner-take-most or scale-intensive economics. Regions unwilling to finance scale become dependent on those that do.

That is why today’s announcement matters even if the number disappoints.

Because once governments begin thinking in terms of strategic equity ownership rather than subsidy frameworks alone, the policy trajectory changes.

Europe has often funded research. It has often subsidised adoption. It has often regulated market behaviour.

What it has done less well is finance category dominance.

| Venture | Country | Funding date | Stage | Round size | Lead investor(s) | Primary category | Current stage |

| Oura | Finland | 14 Oct 2025 | Series E | $900M | Fidelity Management & Research | Wearables | Series E |

| CMR Surgical | United Kingdom | 28 Jun 2021 | Series D | $600M | Ally Bridge Group, SoftBank | Clinical Decision Intelligence | Series F |

| Doctolib | France | 1 Mar 2022 | Series F | $550M | Eurazeo | Medical Concierge | Series F1 |

| Dataiku | France | 1 Aug 2021 | Series E | $400M | Tiger Global Management | Healthcare Operations & Workflow | Series F |

| Kry | Sweden / France | 1 Apr 2021 | Series D | $316M | CPP Investments, Fidelity Investments | Teleconsultation | Debt Financing |

| Cera | United Kingdom | 1 Aug 2022 | Series C | $316M | Kairos HQ | Home Healthcare | Series D |

| Alan | France | 1 Apr 2021 | Series D | $262M | Coatue Management, Exor | Health Insurance | Series G |

| Neko Health | Sweden | 23 Jan 2025 | Series B | $260M | Lightspeed Venture Partners | Diagnosis Tools | Series B |

| AMBOSS | Germany | 25 Mar 2025 | Series C | $259M | Kirkbi, Lightrock, M&G Investments | Health Information Platform | Series C |

| eGym | Germany | 6 Jul 2023 | Series G | $225M | Affinity Partners | Smart Equipment | Series H |

| eGym | Germany | 25 Sep 2024 | Series H | $201M | L Catterton, Meritech Capital | Smart Equipment | Series H |

| Dataiku | France | 13 Dec 2022 | Series F | $200M | Wellington Management | Healthcare Operations & Workflow | Series F |

| CMR Surgical | United Kingdom | 2 Apr 2025 | Series F | $200M | Lightrock, SoftBank, Trinity Capital | Clinical Decision Intelligence | Series F |

| Alan | France | 1 Apr 2022 | Series E | $194M | Teachers’ Venture Growth | Health Insurance | Series G |

| Alan | France | 20 Sep 2024 | Series F | $193M | Belfius | Health Insurance | Series G |

What does this mean for investors, founders, and Europe itself?

For EQT and the Scaleup Europe Fund

The fund’s impact will depend less on the headline €5 billion figure than on deployment discipline.

For European digital health, Galen Growth’s recommendation is clear: focus on Series C to Series E, with selective Series B exposure. Do not dilute the mandate by trying to support the entire venture funnel.

The fund should be measured by whether it helps European companies avoid the scale-up cliff, not by the total number of companies financed.

For institutional investors

The Commission’s backing of the Scaleup Europe Fund signals that late-stage European technology financing is becoming politically strategic rather than purely commercial.

That changes the long-term risk calculus for pension funds, sovereign allocators, insurers, and family offices evaluating exposure to European growth equity. It also creates a benchmark question: if Europe can mobilise policy support behind strategic scale-up capital, why are many of Europe’s largest pools of private capital still underexposed to its own innovation economy?

The answer is no longer simply “risk appetite.” It is mandate design.

For founders

The announcement does not eliminate Europe’s scale financing gap.

But it does suggest that remaining headquartered in Europe may become incrementally more viable for later-stage companies that previously assumed serious growth capital would need to come from U.S.-dominated syndicates.

That matters because capital structure shapes strategic trajectory. The lead investor in a large round often influences hiring, commercial focus, acquisition options, listing pathway, and eventually domicile gravity.

For founders, Europe becoming a more serious growth capital market would not remove the need for global ambition. It would create more optionality over where that ambition is financed.

For policymakers

The success or failure of this initiative will shape future European industrial policy far beyond venture capital.

If the model works, expect larger strategic capital vehicles in AI, defence, energy transition, health infrastructure, compute, and advanced manufacturing. If it fails, critics will use it as evidence that Europe cannot coordinate financial sovereignty at scale.

This makes execution unusually important. The fund cannot become symbolic capital. It must prove it can select, finance, and support companies with genuine global scale potential.

For Europe itself

The central issue is no longer startup formation. It is ownership retention.

Europe is beginning to recognise that economic sovereignty depends not only on inventing technologies, but on continuing to own them once they matter globally.

The Scaleup Europe Fund is therefore not just a venture capital story. It is a test of whether Europe can adapt its economic model to an era in which capital allocation is geopolitical infrastructure.

Source: HealthTech Alpha by Galen Growth.

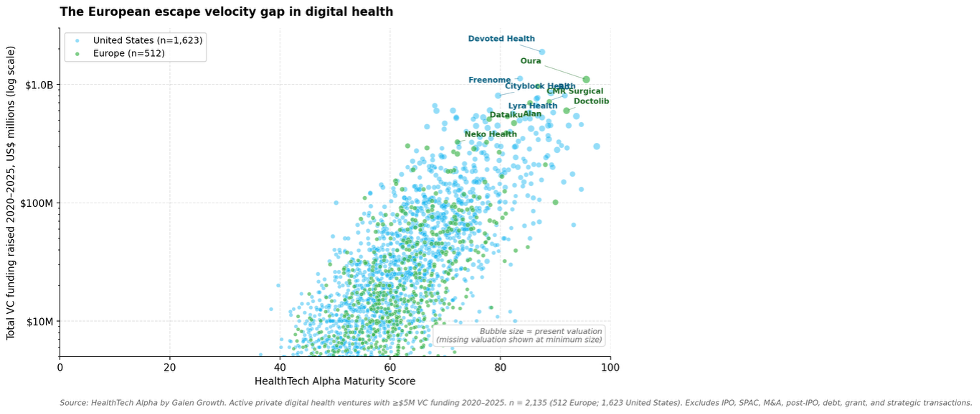

Europe produces mature digital health ventures. The escape velocity gap arises when maturity must be converted into large-scale capital formation.

The wrong debate

The easiest critique of the Commission’s announcement is numerical.

€5 billion is too small.

Perhaps it is.

But the more consequential question is whether Europe has finally accepted that capital is now infrastructure.

Not metaphorically. Literally.

In the twenty-first century, sovereign capability is increasingly determined by who finances compute, who owns platforms, who retains intellectual property, and who controls the balance sheets capable of sustaining technological dominance over decades.

HealthTech Alpha’s digital health data illustrates the broader point. Europe recorded hundreds of digital health funding rounds each year between 2020 and 2024. It is not absent from innovation. It is not absent from entrepreneurship. It is not absent from company formation.

But when the analysis shifts to capital density, average round size, mega-rounds, and the post-Series B cliff, the gap becomes unmistakable.

That is the distinction policymakers must internalise.

Startup policy is not scale-up policy.

Grant funding is not growth equity.

Regulatory leadership is not ownership.

And a scale-up fund should not behave like an early-stage venture programme.

Europe has spent years discussing strategic autonomy while outsourcing much of the underlying capital architecture required to achieve it.

The Scaleup Europe Fund does not solve that contradiction.

It does, however, suggest that Brussels has finally stopped pretending the contradiction does not exist.

FAQ

What funding stage should the Scaleup Europe Fund focus on for maximum impact in European digital health?

Galen Growth recommends that the Scaleup Europe Fund focus primarily on Series C to Series E, with selective Series B exposure. HealthTech Alpha data shows Europe’s digital health scale-up cliff begins after Series B, where round counts fall from 163 Series B rounds to 63 Series C, 18 Series D, and 8 Series E rounds between 2020 and 2025.

Why should the fund avoid Seed and Series A?

Europe already has meaningful Seed and Series A activity. HealthTech Alpha recorded 384 European Series A digital health VC rounds from 2020 to 2025. The more acute strategic gap is later, when companies need larger cheques to scale commercially and avoid dependence on non-European lead investors.

Why are critics saying the Scaleup Europe Fund is too small?

Critics argue that €5 billion is modest relative to the scale of U.S. and Chinese technology financing. HealthTech Alpha data shows United States attracted $30.22 billion in digital health funding in 2025 alone, compared with $8.84 billion in Europe.

Does Europe have a startup creation problem?

No. HealthTech Alpha data shows Europe consistently recorded hundreds of disclosed digital health funding rounds annually between 2020 and 2024. The more serious issue is the transition from venture formation to large-scale growth financing.

What is the best evidence of Europe’s scale-up gap?

Mega-round activity is one of the clearest indicators. In 2025, Europe recorded 7 disclosed digital health VC mega-rounds of $100 million or more, while the United States recorded 33.

What cheque sizes would matter?

For European digital health, the fund should be capable of writing $50 million to $100 million initial cheques at Series C and $100 million to $200 million cheques at Series D and Series E, with meaningful reserves for follow-on rounds.

What is the main problem the fund is trying to solve?

The fund is designed to address Europe’s late-stage financing gap. The deeper strategic problem is ownership retention: Europe often creates promising companies but struggles to retain economic control once those companies require large amounts of growth capital.

Methodology and data-source footer

Data source: HealthTech Alpha by Galen Growth. Analysis covers disclosed digital health venture capital equity rounds announced between 1 January 2020 and 31 December 2025 in Europe and the United States. The dataset excludes IPO, SPAC, M&A, post-IPO equity, debt, pure debt financing, grants, crowdfunding, secondaries, private equity buyouts, and strategic transactions. This filter ensures the analysis reflects venture capital activity rather than total capital flow including exits and non-VC funding sources. Mega-rounds are defined as disclosed VC equity rounds of $100 million or more. Funding figures are shown in U.S. dollars and rounded.