Isomorphic Labs’ $2.1bn Series B is not simply another oversized AI funding round. It is a signal that investors now believe artificial intelligence can move from assisting drug discovery to industrialising it.

KEY TAKEAWAYS

- London-based Isomorphic Labs has raised $2.1bn in a Series B round led by Thrive Capital, with participation from Alphabet, GV, MGX, Temasek, CapitalG and the UK Sovereign AI Fund, bringing total funding to approximately $2.6bn.

- The financing places Isomorphic Labs among the best-capitalised ventures in AI-driven drug discovery, eclipsing many recent peer financings, including Xaira Therapeutics’ $1bn launch financing and several late-stage rounds across the computational biology sector.

- Investors are increasingly backing vertically integrated AI biology companies rather than pure software platforms, betting that proprietary data, wet-lab infrastructure and therapeutic pipelines will create defensible economics.

- The centre of gravity in AI drug discovery is shifting from “AI-assisted chemistry” towards full-stack biological modelling systems capable of predicting protein structure, binding affinity and molecular behaviour across multiple therapeutic modalities.

- Europe has spent years asking whether it can produce globally significant AI champions. Isomorphic Labs suggests the more important question may be whether Europe can retain them once they become strategically indispensable.

A financing round that looks more like infrastructure than venture capital

The most revealing detail in Isomorphic Labs’ $2.1bn Series B financing is not the size of the cheque. Silicon Valley, and increasingly the Gulf, have already conditioned markets to treat ten-figure AI rounds as acts of competitive necessity rather than exuberance. The more telling feature is the syndicate’s composition. When sovereign capital, Alphabet, specialist venture investors and strategic technology funds all converge around a single company, the market is usually signalling something larger than growth. It is signalling infrastructure.

That is what Isomorphic Labs is starting to resemble. Not just another biotechnology company applying machine learning to drug discovery, nor a DeepMind spin-out wrapped in pharmaceutical ambition, but an attempt to build a computational layer for the life sciences. The company’s financing, led by Thrive Capital and backed by Alphabet, GV, MGX, Temasek, CapitalG and the UK Sovereign AI Fund, lands at an awkward moment for both biotech and venture capital. Late-stage investors remain selective, public biotech markets are hardly euphoric, and many AI companies are still searching for business models robust enough to justify their valuations.

Yet investors have committed more than $2bn to a company whose core thesis, while technically impressive, still awaits the ultimate proof that matters in medicine: clinical outcomes. That tension makes the transaction important. It is not merely a validation of Isomorphic Labs; it is a referendum on whether artificial intelligence can change the industrial economics of drug discovery itself.

For most of the past decade, AI in drug development was sold as a productivity tool. Algorithms would screen faster. Models would prioritise better targets. Pharma companies would shorten early discovery timelines and waste less money pursuing dead ends. The promise was attractive, but incremental. What Isomorphic Labs and a handful of its closest peers are now proposing is more radical. They want to redesign biological research as an engineering discipline, where computation does not simply support discovery but increasingly directs it.

That is a much larger claim. It also explains why the money has arrived in such volume.

From better tools to a different industrial model

The economic case for AI drug discovery begins with a familiar indictment of the pharmaceutical industry. Developing a new medicine remains slow, expensive and failure-prone. Large pharmaceutical companies continue to spend heavily on R&D, but productivity has not improved in proportion to the capital deployed. Patent cliffs are looming across several therapeutic categories. Regulators demand rigorous evidence. Health systems push back against pricing. Investors increasingly want proof that scientific ambition can translate into durable returns.

In that context, an AI platform capable of compressing timelines, improving candidate quality or reducing late-stage attrition would be valuable. A platform capable of doing all three would be strategically significant. Isomorphic Labs is making the latter argument.

Its core asset is the Isomorphic Labs Drug Design Engine, or IsoDDE, a system described in the company’s briefing materials as integrating diffusion models, structural biology and deep-learning techniques to predict molecular interactions across proteins, small molecules, biologics and antibodies. The company is not merely claiming to accelerate a narrow part of the discovery workflow. It is positioning itself as an end-to-end design engine for therapeutic development, with ambitions to model biomolecular behaviour in ways that traditional physics-based simulations and earlier AI systems cannot.

The distinction matters because it changes where value may accrue. In the old model, the central scarce asset was a promising compound, protected by patents and advanced through clinical development by teams with regulatory, scientific and commercial expertise. In the emerging model, the scarce asset may be the system that generates and optimises those compounds repeatedly. If that system becomes predictive enough, the company that owns it is not just a biotech venture. It becomes an upstream infrastructure provider to the pharmaceutical industry.

This is why Isomorphic’s Series B should not be read as a simple funding event. It is capital formation for a new industrial stack. The company will use the proceeds to advance internal oncology and immunology programmes towards Phase I trials, expand its operations across London, Cambridge, San Francisco and Lausanne, and deepen pharmaceutical partnerships with groups including Eli Lilly, Johnson & Johnson and Novartis. That is a capital-intensive strategy, but it is also a coherent one. The model only works if Isomorphic can combine computational superiority, proprietary biological feedback loops, therapeutic ownership and commercial partnerships at scale.

The company’s investors are underwriting precisely that combination.

The peer group is becoming clearer — and more unforgiving

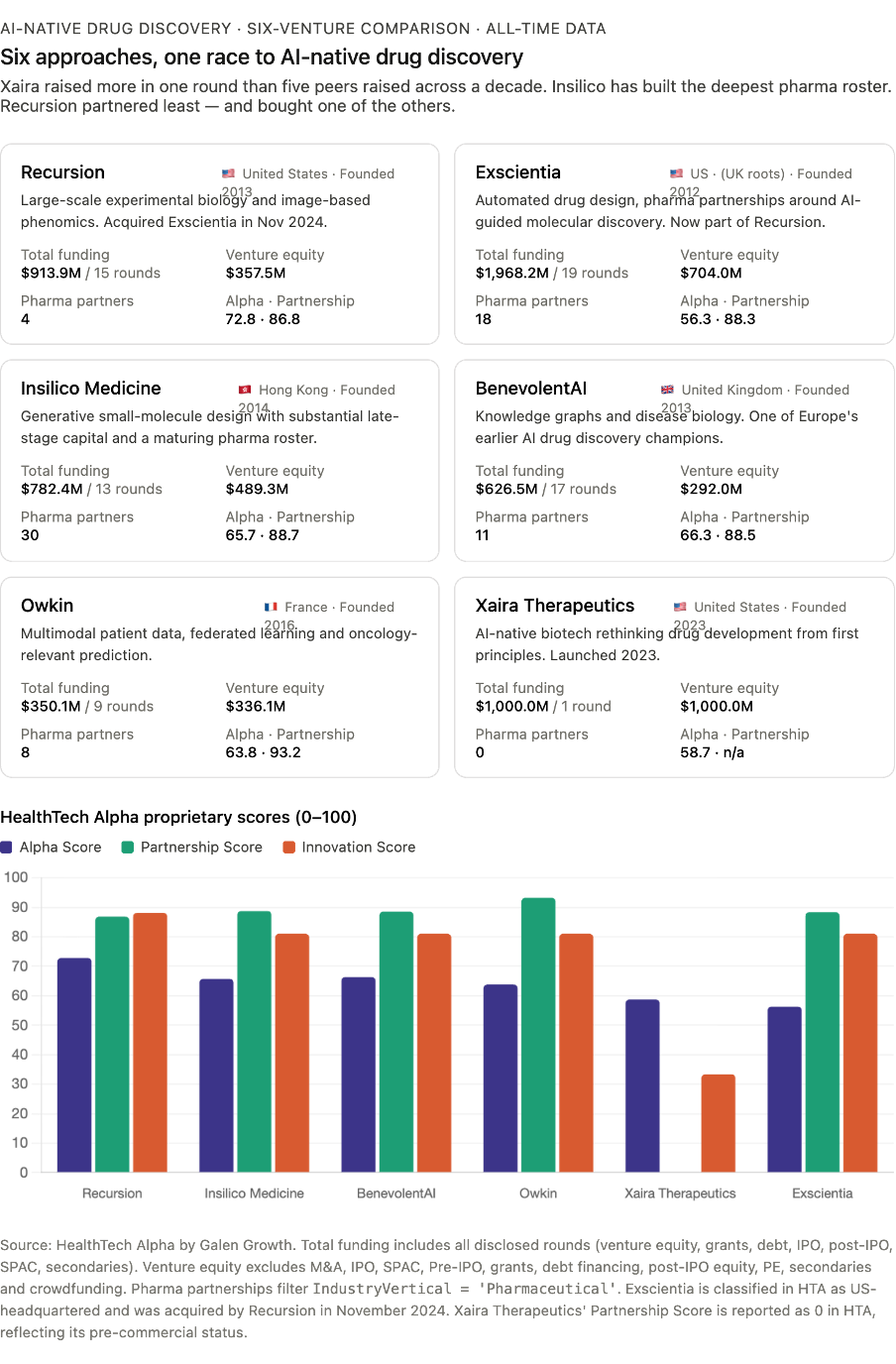

HealthTech Alpha data shows that Isomorphic Labs sits within an increasingly defined cohort of AI-enabled drug discovery and computational biology companies, but the peer group is not uniform. Its competitors differ not only by geography and financing stage, but also by the theory of biology.

Recursion, based in the United States, has built its strategy around large-scale experimental biology and image-based phenomics. Exscientia, with roots in the UK and now classified in HealthTech Alpha as US-based, became known for automating drug design and building pharma partnerships around AI-guided molecular discovery. Insilico Medicine, headquartered in Hong Kong, has focused heavily on generative small-molecule design and has continued to attract substantial late-stage capital. BenevolentAI, one of Europe’s earlier AI drug discovery champions, built its reputation on knowledge graphs and disease biology. Owkin, from France, has concentrated on multimodal patient data, federated learning and oncology-relevant prediction. Xaira Therapeutics, launched in the US with a reported $1bn financing, is perhaps the closest in ambition: an integrated AI-native biotechnology company attempting to rethink drug development from first principles.

This cohort demonstrates that AI drug discovery is no longer a slogan. It is a competitive market with strategic subcategories. Some companies are strongest in chemistry. Others in imaging, patient data, target biology or simulation. Some remain platform partners. Others are becoming therapeutic developers in their own right.

The direction of travel is clear. The largest financings are increasingly flowing to companies that can plausibly claim vertical integration. Pure software vendors face a harder path because pharmaceutical companies are reluctant to pay enduringly high rents for tools that may become commoditised. Asset-heavy biotechs without differentiated AI, meanwhile, struggle to stand out in crowded therapeutic categories. The companies attracting strategic capital are those that can argue they possess both: a proprietary computational platform and a route to therapeutic ownership.

Isomorphic Labs is unusually well placed in that contest because it benefits from three forms of credibility at once. It has the scientific halo of DeepMind and AlphaFold. It has continuing association with Alphabet, which gives it access to technical and strategic resources few biotech companies can match. And it has assembled high-profile pharmaceutical partnerships while preparing to move its own programmes towards the clinic.

None of this guarantees success. Indeed, the history of drug discovery is full of elegant platforms that failed when biology became inconvenient. But it does mean Isomorphic is being judged by investors less as an experimental start-up and more as a potential category-defining company.

The promise — and the burden — of DeepMind-grade biology

The danger for Isomorphic Labs is that its greatest reputational advantage may also become its heaviest burden. The company is inevitably viewed through the lens of AlphaFold, DeepMind’s celebrated breakthrough in protein-structure prediction. That association gives Isomorphic scientific authority, but it also risks flattening the story. Predicting protein structures and designing clinically successful medicines are not the same problem.

Isomorphic’s challenge is therefore to prove that the leap from biological prediction to therapeutic design can be made repeatedly and commercially. Its briefing materials suggest that IsoDDE is intended to address some of the limitations of earlier computational approaches, including multi-body molecular dynamics, binding affinity prediction, cryptic pockets, and difficult protein targets often described as “undruggable”. These are not minor technical refinements. They go to the heart of why so many drug discovery projects fail.

If a model can better predict how molecules behave in realistic biological contexts, it could improve the quality of candidates entering preclinical development. Better candidates, in theory, should reduce wasted laboratory work and increase the likelihood that a programme progresses to clinical testing. That is the economic prize. But medicine does not reward elegant theory alone. The market will ultimately care about whether Isomorphic-designed candidates produce safety, efficacy and differentiation in humans.

This is where the next eighteen to twenty-four months become decisive. The company is expected to push internal oncology and immunology assets towards Phase I trials. That shift will change how it is evaluated. Until now, Isomorphic has benefited from the language of platform potential. Once assets enter the clinic, the company enters the harsher world of therapeutic evidence.

There is no way around this. AI drug discovery companies can publish benchmarks, announce partnerships and build extraordinary computational systems, but they cannot escape clinical biology. The first credible human data from this generation of AI-native therapeutics will do more to shape market sentiment than any financing round.

For Isomorphic, the Series B buys time, talent and infrastructure. It does not buy proof.

Why sovereign capital is entering the laboratory

The presence of sovereign and state-adjacent capital in Isomorphic’s round is not incidental. It reflects a broader shift in how governments and strategic investors think about artificial intelligence, healthcare and industrial resilience.

For years, Europe’s anxiety about technology leadership focused on consumer platforms, cloud infrastructure and semiconductors. The concern was that European research excellence too often became American corporate power. DeepMind itself was the canonical example: a British AI laboratory acquired by Google in 2014 that went on to become one of the world’s most consequential research organisations inside a US technology group.

Healthcare changes the stakes. Biological data, drug development, national health systems and AI infrastructure are not merely commercial assets. They sit close to questions of sovereignty, security and long-term industrial competitiveness. A country that lacks capability in AI biology may find itself dependent not only on foreign cloud providers or foreign chips, but on foreign systems that help determine which medicines are discovered, which diseases are prioritised and where pharmaceutical value is captured.

That is why the UK Sovereign AI Fund’s involvement is politically interesting. Britain has spent years trying to turn scientific excellence into globally scaled companies. In life sciences and AI, it has genuine strengths: elite universities, the NHS as a potential data asset, deep biomedical research clusters and a respected regulatory ecosystem. What it has often lacked is growth capital on the scale required to keep category-leading companies anchored domestically.

Isomorphic Labs complicates the national story because it is both British and not entirely British. It is headquartered in London but sits within Alphabet’s orbit. It is a UK success story, but also a reminder that the commanding heights of AI remain concentrated around American technology groups. Its financing demonstrates that the United Kingdom can host a globally significant AI-biology company. Whether Britain can retain meaningful strategic influence over such companies is a different question.

This question will become sharper as AI biology matures. If computational systems become central to pharmaceutical discovery, governments will not treat them as ordinary venture-backed software assets. They will increasingly view them as part of the state’s health, science, and security infrastructure.

The pharmaceutical industry should be both excited and uneasy

For large pharmaceutical companies, Isomorphic’s rise is attractive for obvious reasons. Any technology that can improve target selection, candidate design or early-stage development efficiency deserves attention in an industry where failure is routine and expensive. Partnerships with companies such as Isomorphic provide access to capabilities that would be difficult, slow and costly to reproduce internally.

But the strategic implications are less comfortable. If AI-native companies become the owners of the most advanced discovery engines, pharma risks ceding a portion of its upstream intelligence layer. Historically, large pharmaceutical companies controlled much of the scientific, clinical and commercial machinery required to bring drugs to market. They outsourced selectively, partnered opportunistically and acquired assets when needed. In an AI biology world, that balance may shift.

The analogy is imperfect, but cloud computing offers a useful warning. Many enterprises initially treated the cloud as a cheaper infrastructure. Over time, the hyperscalers became strategic dependencies, shaping architecture, economics and competitive behaviour across entire industries. A similar dynamic could emerge in drug discovery if a small number of AI biology platforms become indispensable to early-stage therapeutic design.

Pharma companies will therefore need to be careful about how they structure partnerships. Access to AI capability is valuable, but so are data rights, intellectual property ownership, exclusivity terms and the ability to learn from joint programmes. The most sophisticated pharmaceutical groups will not merely ask whether Isomorphic can help discover better drugs. They will ask which organisational capabilities they must retain to avoid becoming permanently dependent on external engines.

That is the paradox of AI drug discovery. The better the platforms become, the more strategically sensitive they are.

The market’s unresolved question

The central question remains brutally simple: will AI-designed or AI-optimised drugs succeed in the clinic at materially better rates than conventional programmes?

Until that answer is clear, the sector will exist in a state of productive ambiguity. The technical progress is real. The investor appetite is real. The pharmaceutical partnerships are real. But the clinical proof remains incomplete.

That does not mean the financing is irrational. Venture capital, at its best, funds the period between plausibility and proof. What makes Isomorphic unusual is the size of that bridge. A $2.1bn Series B gives the company the resources to recruit aggressively, run parallel programmes, build infrastructure and absorb the long timelines inherent in drug development. It also raises expectations dramatically.

The next phase of AI drug discovery will not be judged by conference presentations or model benchmarks alone. It will be judged by investigational new drug applications, Phase I readouts, tolerability profiles, biomarker signals, efficacy data, regulatory engagement and, eventually, approvals. That is the hard terrain on which Isomorphic must now compete.

Still, the direction of travel is difficult to ignore. Capital is concentrating. The peer group is maturing. Pharmaceutical companies are engaging more seriously. Governments are beginning to recognise the strategic importance of AI biology. The market is moving from curiosity to infrastructure.

Isomorphic Labs may or may not become the company that proves machine-designed medicine at scale. But its Series B financing marks a turning point. The question is no longer whether AI belongs in drug discovery. It is whether the companies building the most powerful AI systems will become the new gatekeepers of pharmaceutical innovation.

What this means

For investors: Isomorphic’s financing confirms that capital is concentrating around a small number of AI biology platforms that combine proprietary models, therapeutic pipelines and pharmaceutical partnerships. Investors should carefully distinguish between application-layer AI tools and companies that attempt to own the infrastructure of discovery itself. The former may be useful. The latter may become strategically scarce.

For pharma and corporate partners: AI partnerships can no longer be treated as peripheral innovation projects. If computational biology platforms begin to influence which targets are pursued and which candidates advance, partnership terms will have long-term strategic consequences. Data rights, programme ownership, and internal capability-building should matter as much as the headline value of collaboration.

For health systems and policymakers: Faster discovery could eventually improve therapeutic availability, particularly in oncology, immunology and rare disease. But AI biology also raises questions about sovereignty, data governance and the ownership of biological intelligence. Governments that already worry about dependence on foreign AI infrastructure will soon need to apply the same lens to medicine.

For digital health and healthtech ventures: The market is becoming less forgiving of shallow AI narratives. The financings attracting serious capital are those backed by proprietary data, scientific depth, defensible infrastructure, and clear commercial pathways. “AI-enabled” is no longer enough; investors want to know what is genuinely scarce.

Frequently asked questions

Why is Isomorphic Labs’ Series B financing important?

Isomorphic Labs’ $2.1bn Series B is important because it signals that investors believe AI can reshape the economics of drug discovery, not merely improve productivity at the margins. The investor group also indicates that AI biology is increasingly being treated as strategic infrastructure.

How does Isomorphic Labs differ from other AI drug discovery companies?

Isomorphic Labs combines DeepMind-derived expertise in structural biology with a vertically integrated drug development strategy. It is not only building discovery tools for pharmaceutical partners; it is also advancing its own oncology and immunology pipeline.

Which companies compete most directly with Isomorphic Labs?

The closest peer group includes Recursion, Exscientia, Insilico Medicine, Xaira Therapeutics, BenevolentAI, Owkin and Schrödinger. These companies differ in their technical approaches, with strategies spanning phenomics, generative chemistry, patient-data modelling, molecular simulation, and AI-guided drug design.

What is the biggest commercial risk facing AI drug discovery companies?

The biggest risk is clinical validation. Strong computational performance, prestigious partnerships and large financing rounds do not guarantee that AI-designed drugs will be safe, effective or commercially differentiated in humans.

Why are sovereign investors interested in AI biology?

Sovereign investors are interested because AI biology increasingly overlaps with industrial policy, healthcare resilience and strategic technology infrastructure. The ability to discover and design medicines may become a national capability, not just a private-sector opportunity.

Data source and methodology

Data source: HealthTech Alpha by Galen Growth, accessed May 2026, covering venture financing, company profiles, partnership activity and market positioning across the AI drug discovery and computational biology ecosystem. Figures are reported in USD unless otherwise stated. Some funding totals may be understated where transaction terms remain undisclosed.

Additional company background and transaction details were sourced from the uploaded Isomorphic Labs Series B briefing sheet, which stated that the round was led by Thrive Capital and included Alphabet, GV, MGX, Temasek, CapitalG and the UK Sovereign AI Fund, bringing total funding to approximately $2.6bn.