TL;DR

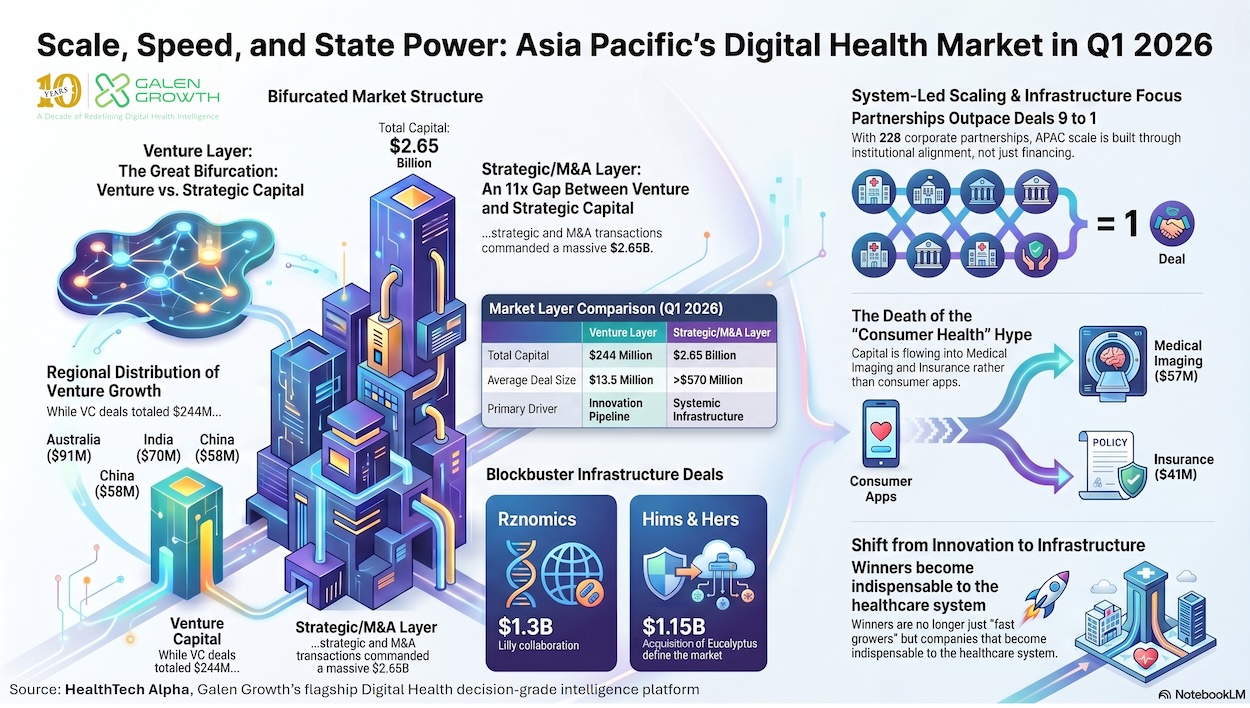

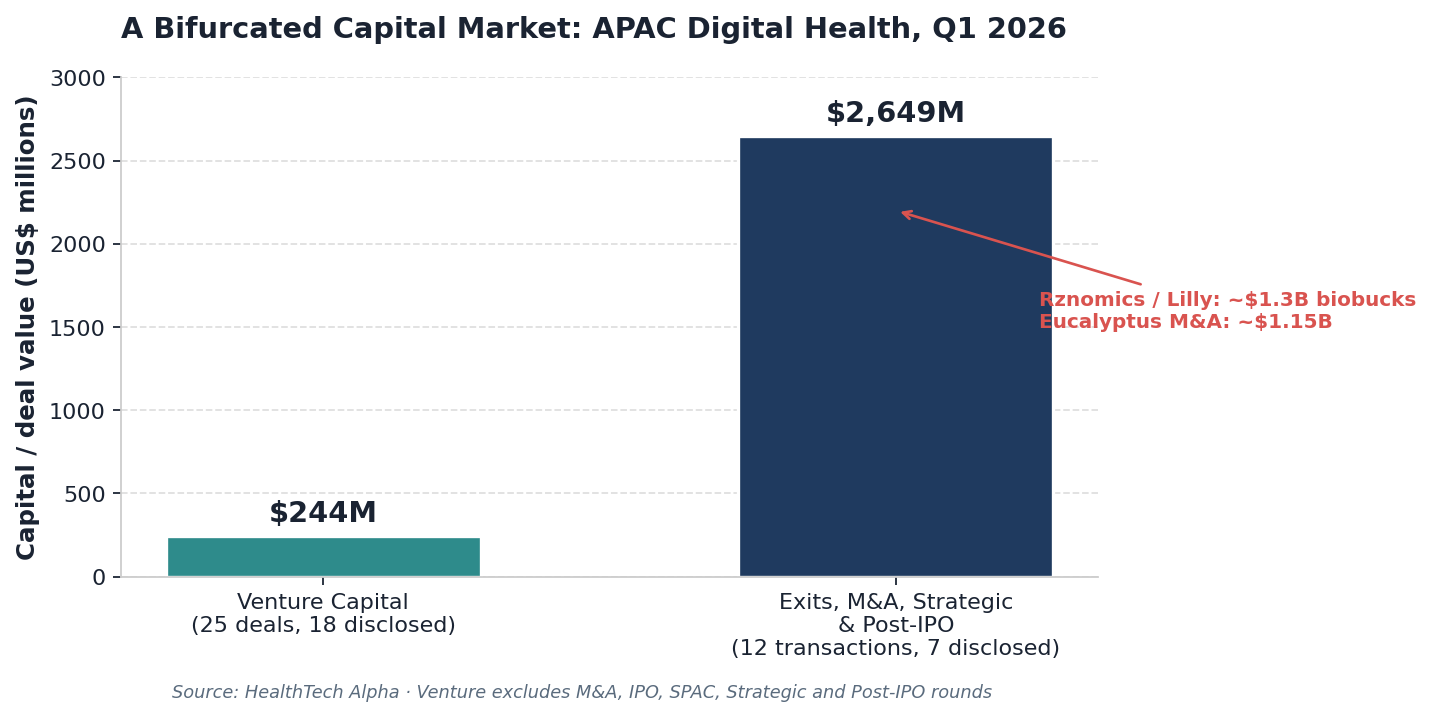

- Asia Pacific digital health funding raised roughly $244 million across 25 true VC deals in Q1 2026 (18 with disclosed amounts), excluding M&A, IPO, SPAC, Strategic, and Post-IPO rounds.

- A separate $2.65 billion flowed through 12 strategic, M&A and post-IPO transactions, anchored by Rznomics’ $1.3 billion licensing collaboration with Eli Lilly and Hims & Hers’ $1.15 billion acquisition of Australia’s Eucalyptus.

- The quarter revealed a sharply bifurcated capital market: a selective but credible VC layer beneath a much more concentrated layer of strategic, M&A, and post-IPO capital, roughly 11× larger.

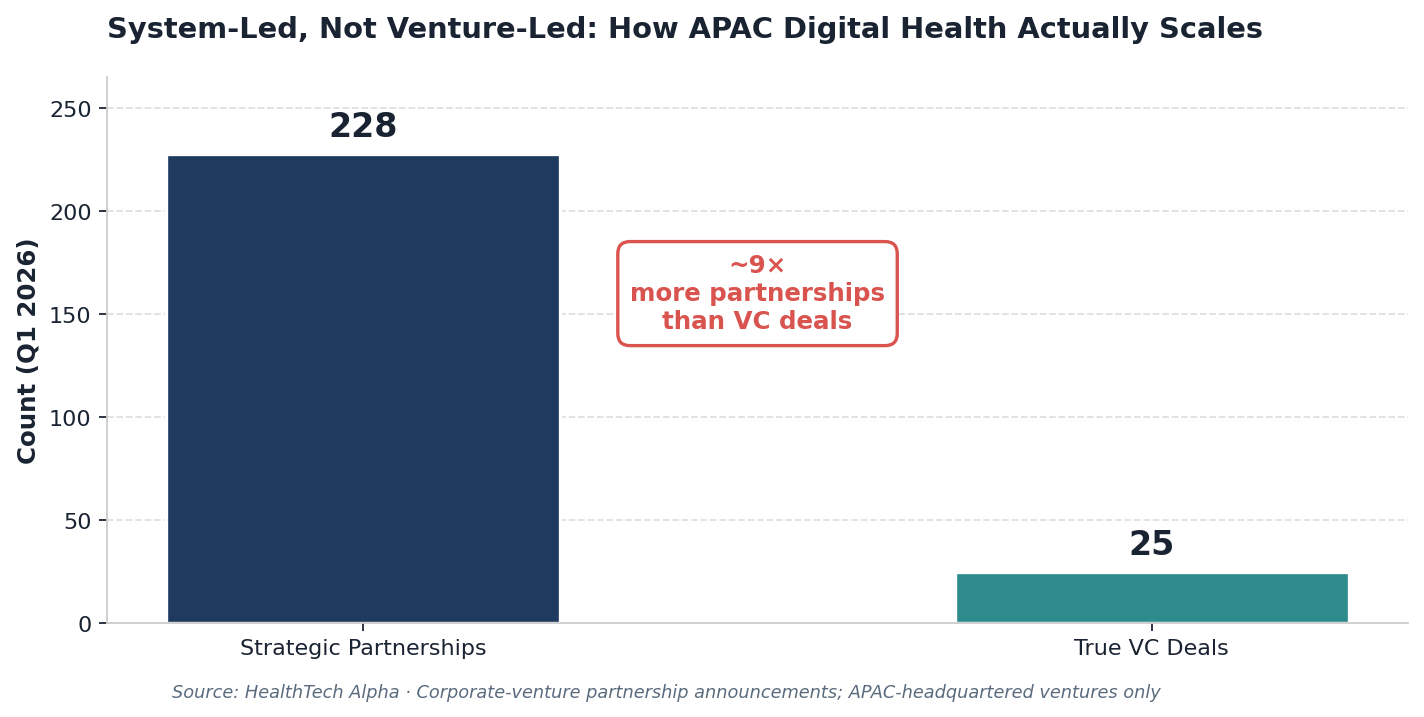

- Asia Pacific also recorded 228 corporate-venture partnerships, more than double Europe’s 101, showing that scale in the region is being built as much through institutional alignment as through venture financing.

- Venture capital is flowing disproportionately into medical imaging, health insurance, healthcare operations and omics research—an infrastructure and research orientation more than a consumer-health one.

Global Context

Global digital health entered 2026 in a more sober mood. The years in which broad digital health narratives could command capital on promise alone are over. Investors increasingly want evidence, workflow integration, and defensible commercial traction. As the Europe op-ed made clear, the first quarter of 2026 was shaped not by exuberance but by concentration: fewer deals, larger rounds, deeper partnerships, and a market that is clearly choosing substance over story.

Asia Pacific belongs to that same global moment, but it expresses it differently. In Europe, larger rounds are a sign of a maturing market with late-stage discipline. In Asia Pacific, headline numbers can be misleading unless one separates venture capital from strategic partnerships, M&A and post-IPO transactions. At first glance, the region appears to have produced blockbuster funding. But once those flows are broken apart, a very different picture emerges. The venture market is active but not explosive. What is explosive is the capital moving through strategic deals around a narrow group of already scaled players.

Asia Pacific Focus

Asia Pacific digital health did not spend Q1 2026 proving that it can attract money. It proved that money now arrives in very different forms, for very different purposes.

Seen from a distance, the region looks like a major funding story. Seen more closely, it looks like two markets unfolding at once. One is a venture market that remains real, selective, and regionally distributed. The other is a strategic and M&A market in which a handful of companies attract outsized capital because they are no longer being treated like startups at all. They are being treated like infrastructure.

Two transactions sit at the heart of that second layer. Rznomics’ collaboration with Eli Lilly—a licensing deal signed in 2025, with the first big payout in Q1 2026 and potentially worth up to $1.3 billion in upfront, milestones and royalties—validates South Korea’s RNA-therapeutics ecosystem as a source of globally strategic science. And Hims & Hers’ acquisition of Eucalyptus for up to $1.15 billion marks the consolidation of Australia’s largest direct-to-consumer telehealth platform into a US-listed global operator. Both deals tell us something different from venture signals. There are signs that Asia Pacific is producing companies that attract strategic capital at a very different order of magnitude once they cross into the infrastructure zone.

That is what makes Asia Pacific so consequential right now. It is not evolving as a delayed copy of Europe or North America. It is moving according to a different logic, shaped by state influence, institutional coordination, fragmented healthcare delivery, and extraordinary demographic pressure. China operates at an ecosystem scale with regulatory centrality. India brings intensity of demand and constant pressure on affordability. Southeast Asia remains commercially promising but structurally uneven. Singapore and Australia show what more mature digital health adoption can look like when institutional trust and infrastructure begin to align.

Venture Funding and Market Activity

Once strategic, M&A and post-IPO capital is stripped out, the venture picture becomes much more grounded—and more interesting.

In Q1 2026, Asia Pacific digital health raised roughly $244 million in venture funding across 25 deals (18 with disclosed amounts), implying an average disclosed deal size of around $13.5 million. That is a very different story from the one suggested by the inflated headline totals. It tells us that the underlying VC market is active, but not overheated; selective, but not absent. It starts to look structurally similar to Europe, where capital is also concentrating on ventures that can demonstrate real traction rather than broad promise.

The top true-venture funding deals reflect that more grounded reality. Splose in Australia raised $32 million in a Series A2 for healthcare workflow—a reminder that operational infrastructure remains highly investable when it solves concrete system problems. Leman Biotech in China raised $29 million at seed in omics-related research, and Matwings raised a similar $29 million Series A1 in drug discovery—pointing to continued conviction in research and platform-layer science. A cluster of $20M+ rounds followed: Plum Benefits (India, $20.5M) in employee health insurance, Lumonus (Australia, $20M) in medical imaging, Omniscient Neurotechnology (Australia, $20M) in clinical decision tooling, and Even Healthcare (India, $20M) in integrated care.

| Company | Country | Amount | Stage · Focus | Signal |

|---|---|---|---|---|

| Splose | Australia | $32M | Series A2 · Healthcare workflow | System-problem solving |

| Leman Biotech | China | $29M | Seed · Omics / platform research | Science depth |

| Matwings | China | $29M | Series A1 · Drug discovery | Platform depth |

| Plum Benefits | India | $21M | Series B · Employee health insurance | Payer infrastructure |

| Lumonus | Australia | $20M | Series B1 · Medical imaging | Clinical tooling |

| Omniscient Neurotech. | Australia | $20M | Series D · Clinical decision / imaging | Late-stage scaling |

| Even Healthcare | India | $20M | Series A2 · Integrated care | Care delivery |

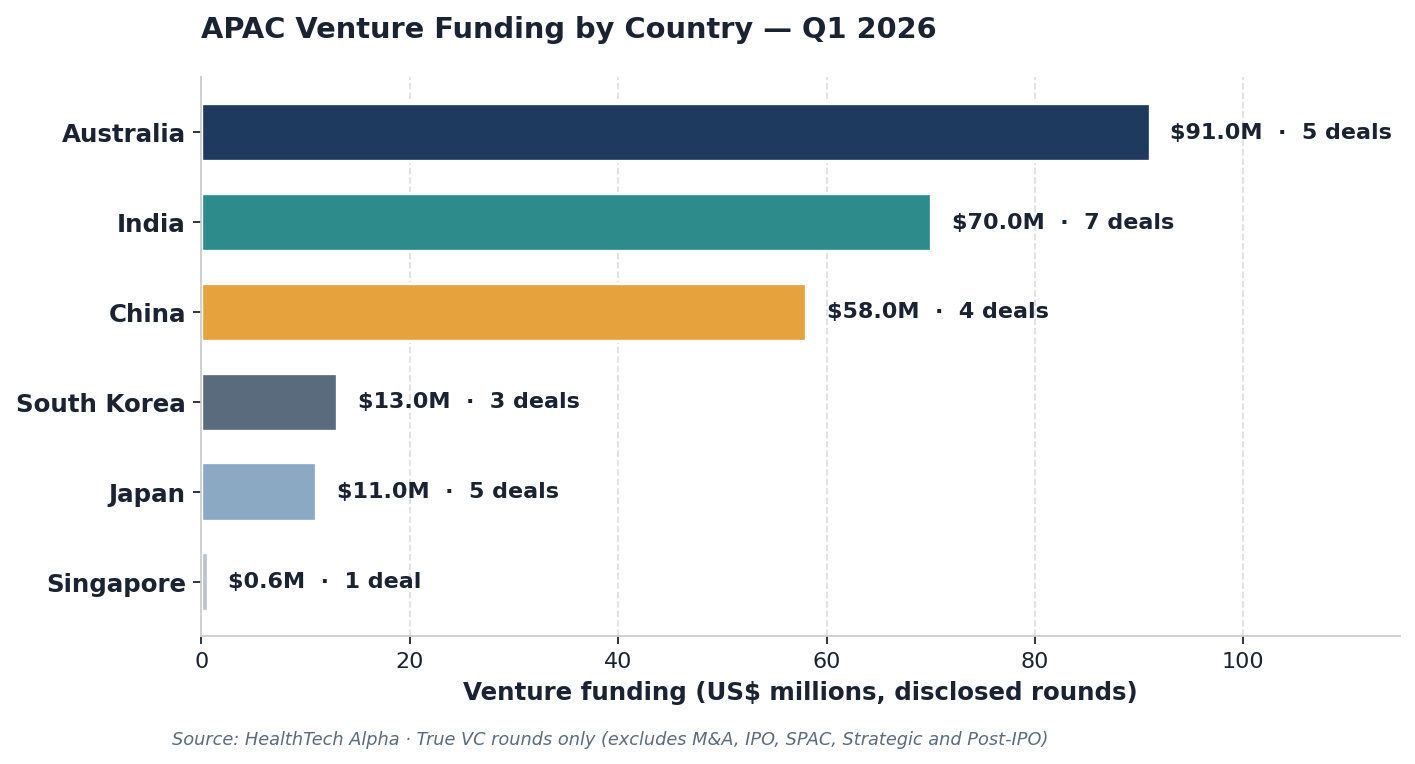

The country mix is just as revealing. On a true-VC basis, Australia, India and China emerge as the principal venture funding markets of the quarter—with Australia contributing roughly $91 million across 5 deals, India about $70 million across 7 deals, and China around $58 million across 4 deals. South Korea—despite the headline-grabbing Rznomics deal that sits in the strategic layer—contributed only about $13 million in true venture funding across 3 deals, and Japan roughly $11 million across 5.

That distribution matters because it changes the argument. Asia Pacific is not a venture market dominated by one extraordinary national ecosystem. It is a regionally distributed VC landscape overlaid by a highly concentrated layer of strategic, M&A and licensing capital. The venture pipeline is broad enough to matter, but the real gravitational pull sits higher up the stack.

The Era of Strategic Consolidation

That higher layer is where the quarter becomes especially revealing.

Asia Pacific recorded $2.65 billion across 12 strategic, M&A and post-IPO transactions in Q1 2026, with most of the narrative weight sitting there. The region’s capital story is not just about startup formation or venture scaling. It is increasingly about what happens after a company has become systemically important enough to justify recapitalisation, out-licensing to a global pharma, or outright acquisition.

Two flagship events define this layer. The Rznomics–Eli Lilly collaboration, potentially worth up to $1.3 billion in upfront, milestone and royalty payments, brings a Korean RNA-therapeutics platform into the core of a US pharmaceutical major’s hearing-loss pipeline. And the Hims & Hers acquisition of Eucalyptus at up to $1.15 billion—roughly $240 million in cash at closing plus deferred and earn-out consideration—absorbs Australia’s largest digital health platform into a US-listed consumer health company with operations across the UK, Germany, Japan and Canada. Both are infrastructure-scale events. Neither is a venture signal.

| Dimension | Venture Layer | Strategic / Exit / Post-IPO Layer | What It Tells Us |

|---|---|---|---|

| Capital in Q1 2026 | $244M | $2.65B | ~11x separation |

| Deal count | 25 (18 disclosed) | 12 (7 disclosed) | Few, very large strategic events |

| Avg deal size (disclosed) | $13.5M | >$370M | Order-of-magnitude gap |

| Flagship events | Splose ($32M)Leman Biotech ($29M) | Rznomics–Lilly ($1.3B)Eucalyptus/Hims ($1.15B) | Partnerships & M&A dominate |

| Dominant logic | Selective early / growth funding | Strategic absorption of scaled players | APAC capitalises infrastructure, not just innovation |

Table 2. APAC digital health capital in Q1 2026 operates across two structurally distinct layers. Venture names link to HealthTech Alpha profiles.

That dynamic gives APAC a different form of consolidation from Europe. In Europe, consolidation often manifests as cleaner M&A narratives and more straightforward acquisition logic. In Asia Pacific, consolidation appears through several routes at once: outright acquisition (Eucalyptus), out-licensing of platform science to global pharma (Rznomics), and the gradual absorption of digital health functions into broader systems of care, insurance and data flow. The endgame is not always acquisition. Often, it is infrastructural entrenchment or strategic integration with a larger global actor.

The Partnership Ecosystem: The State as a Catalyst

If funding tells us where money is going, partnerships tell us how digital health actually scales. And here, Asia Pacific is emphatic.

The region recorded 228 corporate-venture partnerships in Q1 2026, more than double the 101 recorded in Europe over the same period. Raw volume is not the only point. What matters is what that volume says about the structure of the market.

Asia Pacific is not primarily a venture-led adoption story. It is a system-led adoption story. Governments, corporates, and providers all shape the path to scale, and in many markets the state remains the most important actor of all. Policy, procurement, and national infrastructure priorities are not background conditions. They are active market forces. Large corporates—insurers, telecom players, pharmaceutical companies and platform businesses—often serve as the channels through which digital health reaches real scale. Providers matter deeply as well, especially in more mature systems, but they are only one part of a wider architecture.

That is why partnerships outnumber venture funding deals so dramatically. In Asia Pacific, distribution is not simply purchased through marketing spend or built through direct sales. It is negotiated through institutions. The ventures that break through are rarely those with the cleanest pitch decks or the most elegant consumer story. They are the ones able to align themselves with the logic of the system around them.

This is one of the region’s defining characteristics. It can make progress look slower than it is, because scale often depends on alignment across actors with very different incentives. But once that alignment is achieved, deployment can happen quickly. The result is a market that often appears uneven quarter to quarter, but is in fact assembling itself through dense institutional relationships.

Following the Capital: Where Venture Capital is Actually Going

The corrected funding picture also helps clarify what kinds of problems the region is actually prioritising—and the pattern is more striking than the headline narrative suggests.

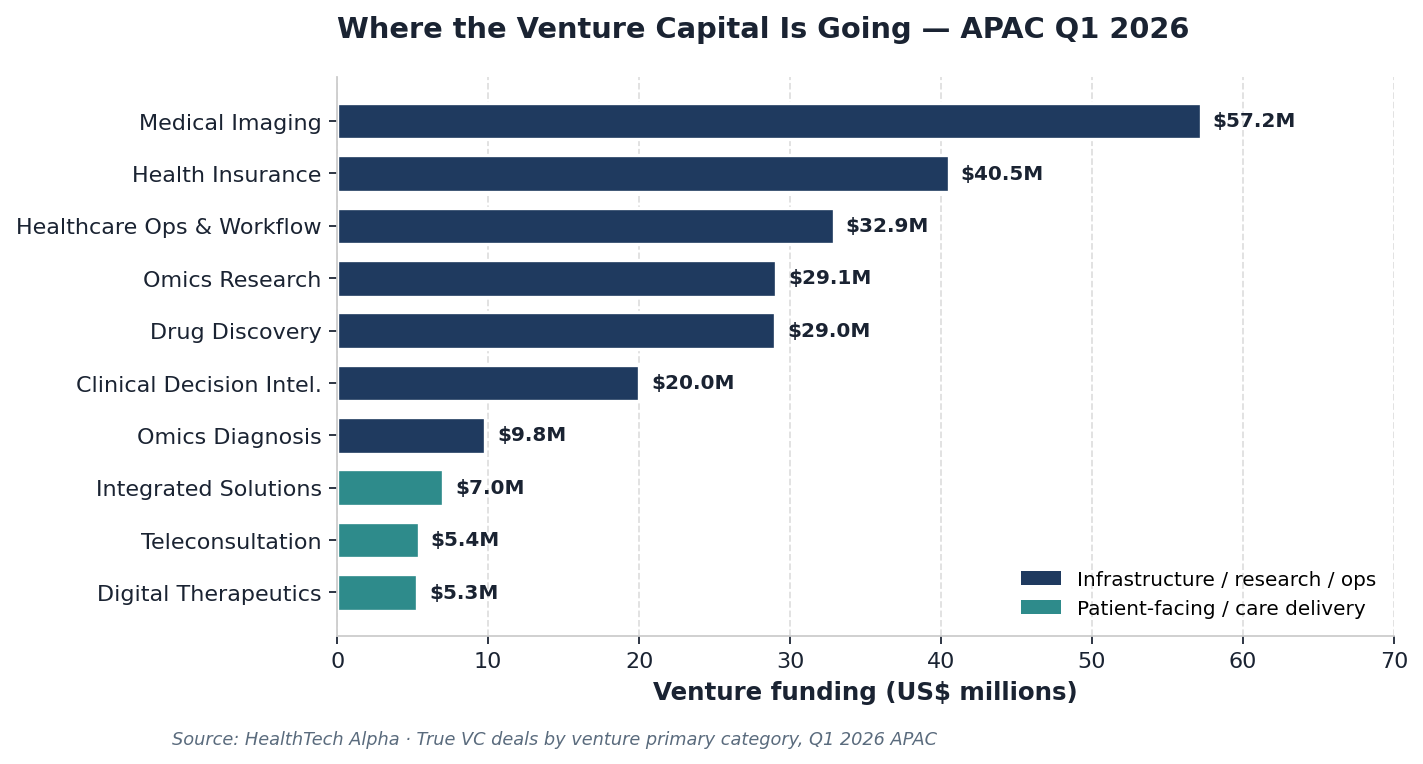

The highest-funded digital health category in APAC this quarter was medical imaging ($57M across 4 deals), followed by health insurance and payer infrastructure ($41M across 2 deals), healthcare operations and workflow ($33M), omics-related research ($29M) and drug discovery ($29M). Consumer-facing categories—teleconsultation, digital therapeutics, integrated solutions—together attracted less than $20 million in true venture capital for the quarter.

That profile reframes the op-ed’s earlier thesis about therapeutic focus. The region’s capital is not merely following high-burden disease areas in the abstract. It is flowing into the tools that allow fragmented health systems to function at all: imaging capacity, insurance rails, workflow infrastructure and the research platforms that underpin future therapeutics. Where provider shortages are acute, access is uneven, and care pathways remain fragmented, the most valuable digital health companies are often those that make the system more functional rather than merely more digital.

This is why the region’s investment profile feels less like consumer technology and more like institutional redesign. The capital is following pain points that are difficult, expensive, and foundational. It is moving toward ventures that can absorb complexity and return not just user growth, but resilience.

Strategic Implications: What This Means for the Ecosystem

For investors, Q1 2026 offers a direct lesson. Asia Pacific is not one market, and it is no longer investable through a broad thematic lens alone. The separation between roughly $244 million in true venture funding activity and $2.65 billion in strategic, M&A and post-IPO transactions points to a deeply bifurcated structure. There is a real venture pipeline distributed across several national ecosystems, but there is also a much more concentrated market for scaled companies attracting global pharma licences and cross-border acquirers. Investors who fail to distinguish between those layers will misread both risk and opportunity.

For ventures, the signal is equally clear. The path from startup to scaleup in Asia Pacific is not linear. It is institutional. Early-stage companies need to prove local fit and the ability to operate within fragmented systems. Growth-stage companies need to demonstrate that they can integrate into broader delivery, financing, or navigation structures without losing leverage. The most successful late-stage players are no longer simply growing. They are becoming indispensable—or they are being acquired into someone else’s global platform, as Eucalyptus was. That is a higher bar, but it is also what makes the region’s winners so defensible.

For corporates, the message is more urgent than ever. With 228 partnerships in a single quarter and global acquirers—Lilly, Hims & Hers—moving decisively into the region, the ecosystem is not waiting for traditional incumbents to decide whether digital health matters. Pharma companies, payers, providers and platforms that engage early can shape that architecture. Those who wait may find that the most important layers of patient flow, data access and care navigation have already been claimed by someone else.

Conclusion: A Market Defined by Scale, Not Sequence

Asia Pacific’s digital health market in Q1 2026 becomes legible only once venture capital is separated from strategic and M&A capital. Do that, and the quarter stops looking like a generic boom and starts to look more significant.

It looks like a region with a real, distributed venture base. It looks like a market where partnerships are doing as much work as funding in determining who scales. And above all, it looks like a system in which the most important companies are beginning to attract capital not as startups, but as infrastructure—whether through licensing, acquisition, or institutional integration.

That is the real meaning of the quarter. Asia Pacific is not simply participating in digital health’s next phase. It shows what happens when the sector matures within markets that are simultaneously fragmented, state-shaped, operationally demanding and under immense demographic pressure. Europe’s Q1 story was one of maturity. Asia Pacific’s was one of transition—from an innovation market to an infrastructure market.

And once that transition is underway, the terms of competition change. The question is no longer which startup can grow fastest. It is the question of which company can become too embedded, too useful, and too strategically important to ignore.

Methodology & Data Note

All data in this analysis is sourced exclusively from the HealthTech Alpha Premium platform (Galen Growth). The analysis covers 216 venture funding transactions (excluding M&A and IPO exits) and 676 corporate partnerships recorded between 1 January and 31 March 2026 (data refreshed 7 April 2026). Unless stated otherwise, venture funding figures exclude M&A transactions, IPO exits, and post-IPO funding. Funding amounts are reported in USD. Ventures may be classified across multiple technology types.

Methodology Note

All figures in this op-ed are drawn from HealthTech Alpha’s structured digital health intelligence database, reflecting Q1 2026 (1 January–31 March 2026) data for ventures headquartered in the Asia Pacific region. Links on venture names open the corresponding HealthTech Alpha profile. ‘True venture’ totals exclude M&A, IPO, SPAC, Strategic and Post-IPO Equity rounds. Some transactions classified as ‘Strategic’ reflect licensing or partnership deals (such as Rznomics–Lilly) where the headline figure includes potential milestones and royalties rather than upfront cash. Where individual round amounts are not publicly disclosed, deals are counted but excluded from dollar totals.