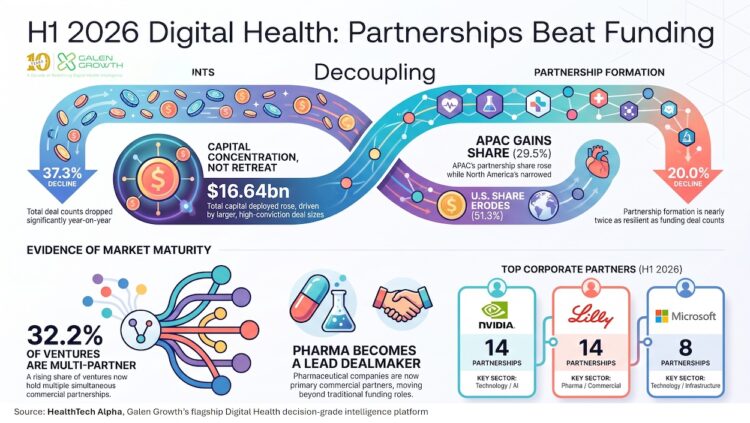

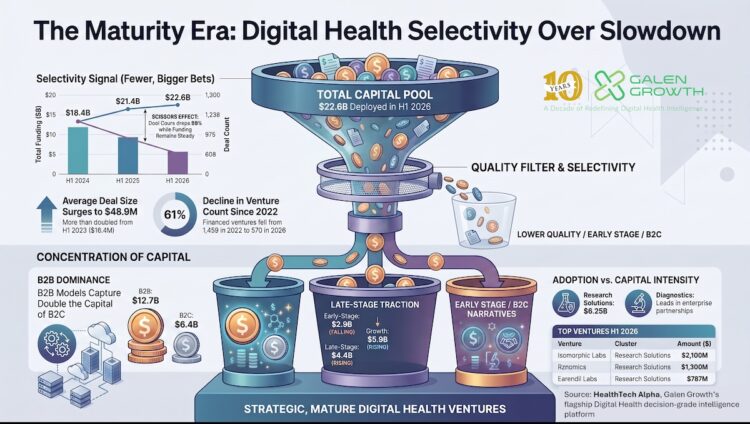

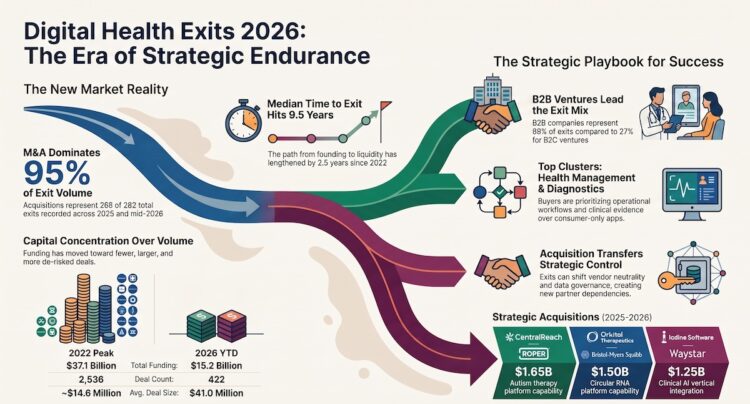

TL;DR

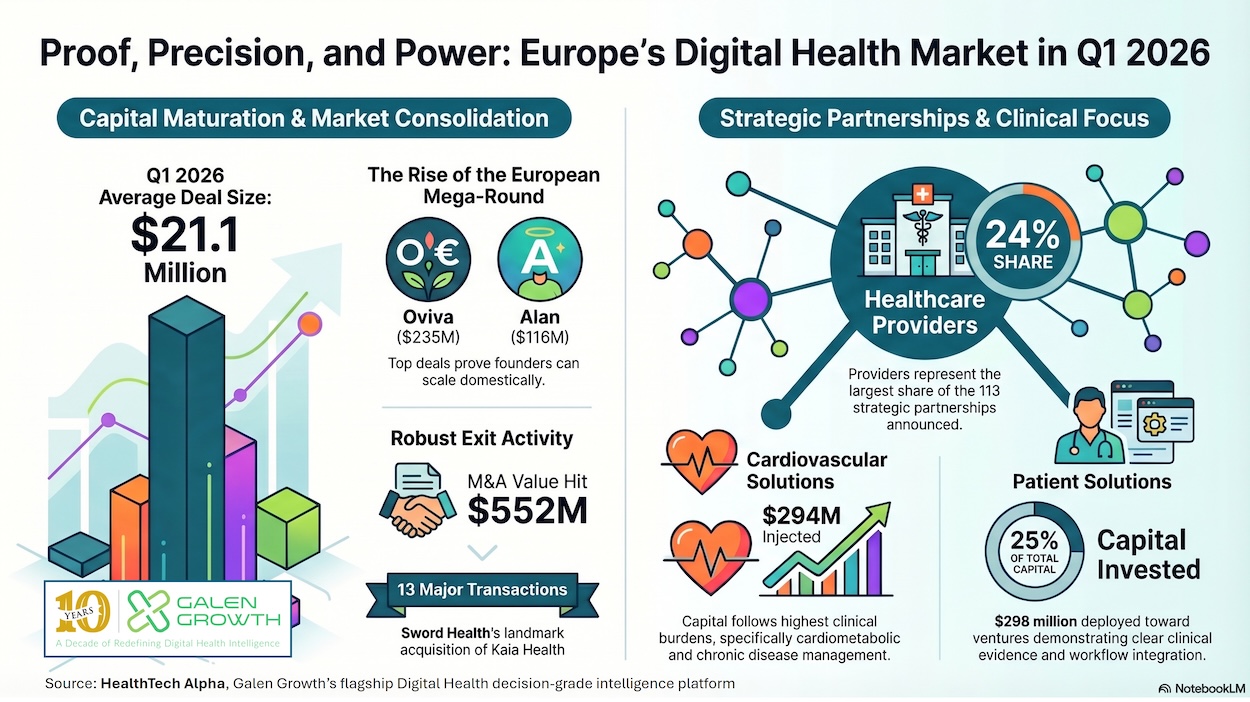

- Funding Shifts to Late-Stage: Q1 2026 saw $1.2 billion in total venture funding deployed with a strong $21.1 million average deal size, as capital moved rapidly toward massive, late-stage mega-rounds.

- M&A remained active with 13 European exit transactions and $552 million in disclosed value, led by Kaia Health at $285 million and Gleamer at $267 million.

- Healthcare Providers Lead Adoption: European hospital trusts are catching up to US trends, with Healthcare Providers making up the largest industry share of the 113 strategic partnerships announced this quarter.

- Capital Follows Clinical Burden: Investment heavily favoured complex health challenges, with a focus on ventures showing clinical evidence. Patient Solutions captured the most capital at $298 million over 6 rounds, whilst Cardiovascular Diseases attracted the highest therapeutic funding at $294 million.

Global Context

Global digital health funding reached $7.1 billion across 216 deals in Q1 2026, with another $5.1 billion flowing through exit and post-exit transactions; North America remained dominant at 76% of global VC capital while Europe accounted for 17%, and the quarter was defined less by exuberant growth than by capital concentration, deeper strategic partnerships, and a sector-wide shift toward evidence-backed, workflow-embedded businesses rather than broad speculative platform plays.

European Focus

As we close the books on the first quarter of 2026, the European digital health ecosystem stands at a profound inflection point. For years, industry commentators and market analysts have viewed Europe through a lens of potential—a landscape rich in clinical expertise and academic brilliance, yet fundamentally fragmented and historically reliant on early-stage seed capital. Today, the narrative has fundamentally shifted. The Q1 2026 data paints a compelling picture of a market that has not just grown, but deeply matured.

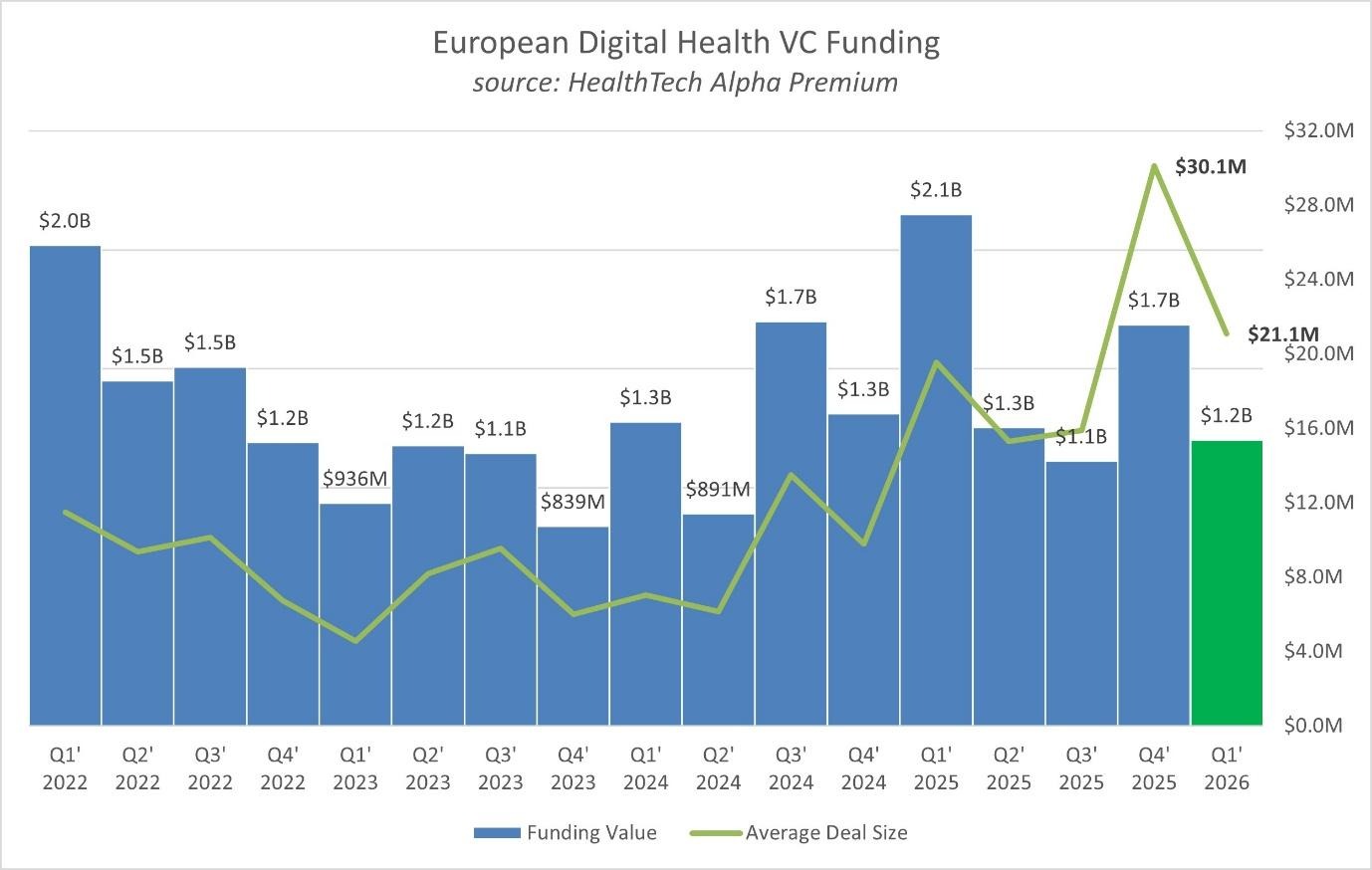

- Q1 2026 VC Funding (excl. exits): $1.2 billion (↓ 44% vs Q1 2025).

- VC Deal Count (excl. exits): 67 deals (↓ 46% vs Q1 2025).

- Average VC Deal Size: $21.1 million (↑ 8% vs Q1 2025).

- VC Mega-Deals (≥$100M): 3 transactions.

The headline numbers reveal an ecosystem moving with deliberate, strategic force. Total venture funding deployed into European digital health ventures in Q1 2026 reached a robust $1.2 billion across 67 active deals. While it is crucial to acknowledge that this funding remains strong, it is unable to compete with the blockbuster Q1 2025 performance that saw unprecedented, exuberant capital deployment across the sector. However, to view this quarter merely as a step down from 2025 would be a fundamental misinterpretation of the data. What we are witnessing is not a retreat, but a graduation. The capital is smarter, the deal structures are larger, and the strategic partnerships are finally aligning with the continent’s massive public health infrastructure.

Venture Funding and Market Activity

The Late-Stage Revolution

To understand the current state of European digital health, one must look past the aggregate $1.2 billion figure and examine the structural composition of the capital deployed. The defining hallmark of this quarter’s maturation is the average deal size, which now stands at a formidable $21.1 million.

When we break down the funding by stage, the transformation becomes undeniable. Growth-stage funding dominated the quarter, absorbing an impressive $622 million, whilst Early-stage investments accounted for $378 million. Most critically, Late-stage funding captured $116 million of the market. Late-stage deals, which prior to 2025 were nearly unheard of in Europe, carried the region through the quarter. These massive capital injections are rapidly becoming the norm as the European digital health ecosystem matures, signalling to global investors that European founders can scale companies to maturity without inherently needing to cross the Atlantic to find growth capital.

The quarter was defined by highly concentrated mega-rounds backing proven, revenue-generating category leaders. Consider the top deals of the quarter: Oviva secured a colossal $235 million in a Series D round, Alan raised a $116 million Series G, and DentalMonitoring closed a $100 million Series D. Further down the cap table, we saw significant growth rounds from Vitestro ($70 million Series B1), Biorce ($52 million Series A), and Bit.Bio ($50 million Series C). These are not speculative bets on unproven technologies. These are massive, sophisticated cheques written to scale proven business models.

The momentum, however, is not without its fluctuations. The month-on-month data reveals a slight deceleration, with total investment dipping by 24.8% from $383 million in February 2026 to $288 million in March 2026, accompanied by a decline in the number of active investors from 67 down to 60. Yet, rather than signalling a systemic contraction, this reflects the natural lumpiness of a market influenced heavily by geopolitical and financial events.

Top 15 VC Deals for European-founded Ventures in Q1 2026

| Rank | Venture name | Primary Category | Stage | Amount | Lead investors |

| 1 | Oviva | Disease Management | Series D | $235.0M | Kinnevik AB |

| 2 | Alan | Health Insurance | Series G | $115.5M | Index Ventures |

| 3 | DentalMonitoring | Medical Imaging | Series D | $100.0M | Lazard Elaia Capital |

| 4 | Vitestro | Smart Equipment | Series B1 | $70.0M | Mayo Clinic, Sutter Health, Puma Venture Capital, ROM Ultrecht, NYBC Ventures, Sonder Capital |

| 5 | Biorce | Clinical Trial Design | Series A | $52.5M | DST Global Partners |

| 6 | Bit.Bio | Omics Related Research | Series C | $50.0M | M&G Investments |

| 7 | Recare | Medical Concierge | Series A | $44.1M | DNV Group |

| 8 | Hublo | HCP Job Board | Series B | $40.0M | Revaia |

| 9 | Universal Diagnostics | Omics Related Diagnosis | Series C | $35.3M | SETT |

| 10 | Dawn Health | Digital Therapeutics | Series B | $25.5M | Cipio Partners, Chr. Augustinus Fabrikker, Trifork, EIFO |

The Era of European Venture Consolidation

As late-stage capital becomes the standard, the natural evolutionary step for an ecosystem is widespread consolidation. Q1 2026 delivered exactly this. The data highlights a robust exit environment, with 13 ventures being acquired within the first three months of the year.

The big headline dominating the quarter—and perfectly encapsulating this trend of European venture consolidation—was Sword Health acquiring Kaia Health. This monumental union of two musculoskeletal (MSK) and digital physical therapy pioneers highlights a critical strategic shift. Ventures are moving away from being single-point solutions to building comprehensive platforms.

Top Exit Transactions for European-founded Venture in Q1 2026

| Venture name | Category | Exit type | Value | Notes |

| Kaia Health | Digital Therapeutics | M&A | $285M | Largest European exit |

| Gleamer | Medical Imaging | M&A | $267M | AI radiology platform |

The Partnership Ecosystem: Health Systems Catch Up

Perhaps the most exciting and transformative data emerging from Q1 2026 lies in the partnership ecosystem. The quarter saw 113 strategic partnerships announced across the continent. But the sheer volume of deals tells only half the story; the true revelation is who is doing the partnering.

Historically, European hospital trusts and state-backed health systems have been frustratingly slow adopters of digital health technologies, lagging significantly behind the aggressive innovation strategies seen in the United States. In Q1 2026, we saw a profound reversal of this narrative: Health Systems are now catching up to the U.S. trends, with Healthcare Providers comprising the largest share (24%) of industries announcing partnerships with European-founded ventures.

This is a monumental shift. The public sector and private healthcare providers in Europe are finally moving past pilot purgatory. We see this reflected in the activity of specific institutions; for instance, Ziekenhuis aan de Stroom emerged as an active partner this quarter, executing multiple strategic agreements. Furthermore, prominent healthcare networks like Alder Hey Children’s NHS Trust and Clinica Universidad de Navarra are actively formalising their digital health strategies.

Geographically, the partnership landscape is dominated by the continent’s traditional powerhouses. The United Kingdom leads the pack with a commanding 35 partnerships, followed closely by France with 28, Germany with 9, and Switzerland with 8.

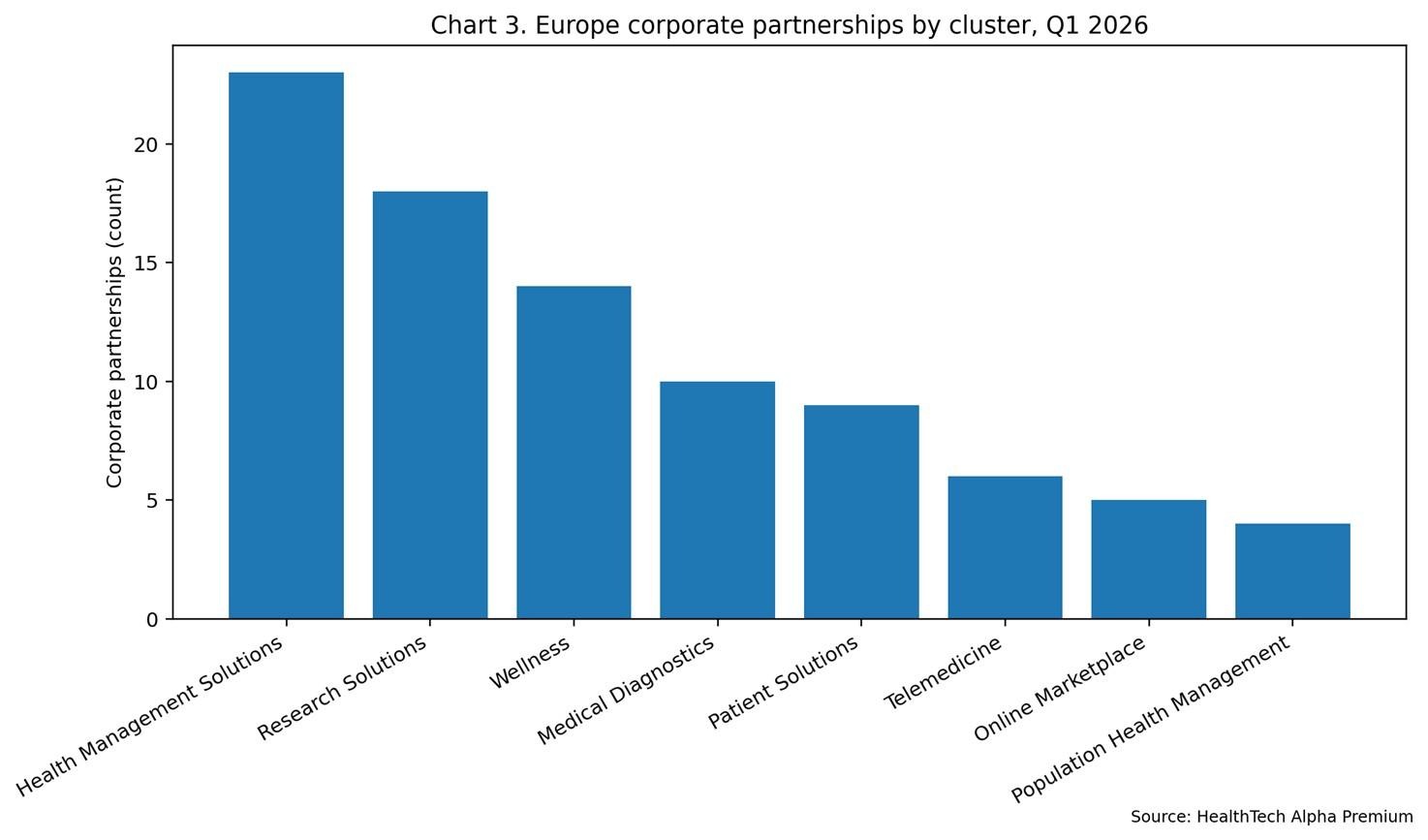

When we examine the nature of these corporate partnerships by cluster, the focus on direct clinical utility is evident. Health Management Solutions, Patient Solutions, and Wellness represent the most active clusters for partnership formation.

Following the Capital: Therapeutic Areas and Value Clusters

To understand where the European digital health market is heading, one must follow where the capital is flowing today. In Q1 2026, investors demonstrated a distinct preference for solutions addressing complex, high-burden clinical areas.

Analysing the investment by primary cluster, Patient Solutions dominated the landscape, capturing 25% of the total capital deployed, equating to $298 million. Medical Diagnostics followed closely, securing $222 million (18% of the total). Research Solutions and Health InsurTech also proved to be massive draws, pulling in $118 million and $116 million respectively.

From a therapeutic perspective, the funding data is equally telling. Solutions targeting Cardiovascular Diseases received the highest level of financial backing, drawing in a staggering $294 million. This was closely followed by ventures operating in the Diabetes and Nutrition spaces, each securing $261 million, alongside Chronic Diseases at $260 million, and Nephrology at $254 million. The sheer volume of capital pouring into cardiometabolic and chronic disease management reflects the immense macroeconomic pressure these conditions place on European health systems.

Strategic Implications: What This Means for the Ecosystem

The maturation of the European digital health market in Q1 2026 presents a new paradigm. Below, we break down what this newly consolidated, late-stage, and provider-integrated reality means for the key stakeholders in the ecosystem.

For Investors

The data clearly indicates that the market has transitioned to a ‘winner-takes-most’ environment. With average deal sizes ballooning to $21.1 million and late-stage rounds like Oviva’s $235 million setting the benchmark, investors need deeper pockets and a high-conviction thesis to play in this market. The 13 public market exits and acquisitions recorded this quarter demonstrate that the liquidity pathways in Europe are fully operational. Furthermore, the massive uptick in Healthcare Provider partnerships provides investors with the ultimate validation: commercial traction within historically impenetrable public health systems.

For Digital Health Ventures

For founders and management teams, the Q1 2026 environment offers rigorous new standards. The good news is that the ceiling for European ambition has been shattered; capital is available domestically for companies that can demonstrate true scale. The challenge lies in the intense competitive pressure of a consolidating market. As seen with the Sword Health and Kaia Health headline, category leaders are actively buying up market share. Because Healthcare Providers are now the most active partners, ventures must pivot their sales narratives to prove robust health economic outcomes.

For Corporates (Pharma / Medical Device / Health Systems)

Pharma and Medical Devices: The pharmaceutical and traditional medical device sectors are standing on the precipice of a severe strategic disadvantage if they do not aggressively engage with the maturing digital health ecosystem. The $118 million invested in Research Solutions and major deals like Bit.Bio’s $50 million raise show that the digitisation of drug discovery is accelerating rapidly. Partnering with, or acquiring, de-risked late-stage digital health companies is the most capital-efficient way for traditional life science companies to digitise their portfolios. Active players like Sanofi, who partnered with DiappyMed this quarter, are already demonstrating how to effectively bridge this gap.

Health Systems: For European hospital trusts, clinics, and national health authorities, the Q1 2026 data is a validation of the hard work done to modernise procurement. Catching up to U.S. partnership trends is a historic milestone. With Healthcare Providers now comprising the largest share of digital health partnerships, a clear divide is forming between ‘digitally enabled’ health systems and ‘analogue’ health systems. Hospital and health systems must actively partner with digital ventures—especially in high-burden areas like cardiology and diabetes, which collectively pulled in over $550 million this quarter—to reach targets in patient outcomes and operational inefficiencies.

About the Data

| About the Data: HealthTech Alpha Premium Every data point in this analysis is drawn exclusively from HealthTech Alpha Premium, Galen Growth’s proprietary intelligence platform for the global digital health ecosystem. In a world flooded with AI-generated market commentary and synthetic data, HealthTech Alpha is built differently: human expert curation combined with AI-assisted enrichment, applied to a purpose-built taxonomy of 69 categories, 18 clusters, and 19 technology types.In the GenAI era, this distinction is not cosmetic — it is the difference between analysis you can publish and analysis you should not. General-purpose AI tools hallucinate deal data, misattribute funding rounds, and confuse funding stages. HealthTech Alpha Premium is verified, structured, updated in near-real time, and designed for machine-readable analysis and human-guided strategy. It is the only dataset we trust, the only one we publish from, and the one that every serious investor, venture, and corporate in digital health should be using as their primary intelligence layer. |

Methodology & Data Note

All data sourced exclusively from HealthTech Alpha Premium by Galen Growth. Q1 2026 covers 1 January – 31 March 2026. VC figures exclude M&A, IPO, SPAC, and Post-IPO transactions. Partnership counts reflect U.S.-headquartered ventures only. Funding amounts in USD. Some figures may be understated due to undisclosed deal terms. © 2026 Galen Growth. All rights reserved.