Roche just bought the vendor problem: why PathAI’s other pharma partners now need a board-level answer

Roche’s proposed acquisition of PathAI is more than a diagnostics land-grab. It turns a neutral pathology AI vendor into an owned asset of one of the world’s most powerful diagnostics groups — and leaves its other pharma partners with a governance problem they cannot ignore.

KEY TAKEAWAYS

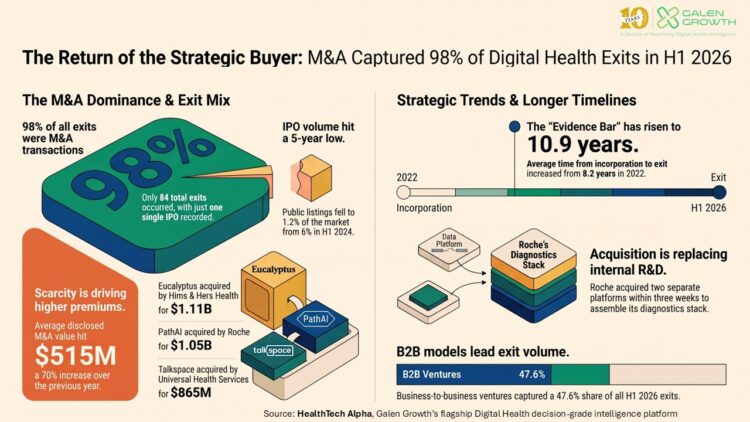

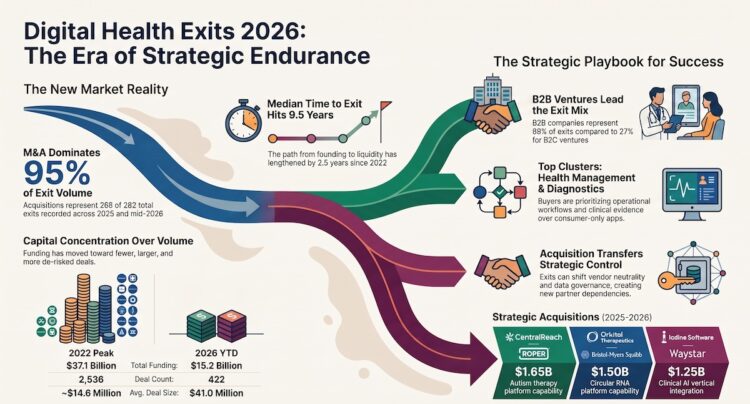

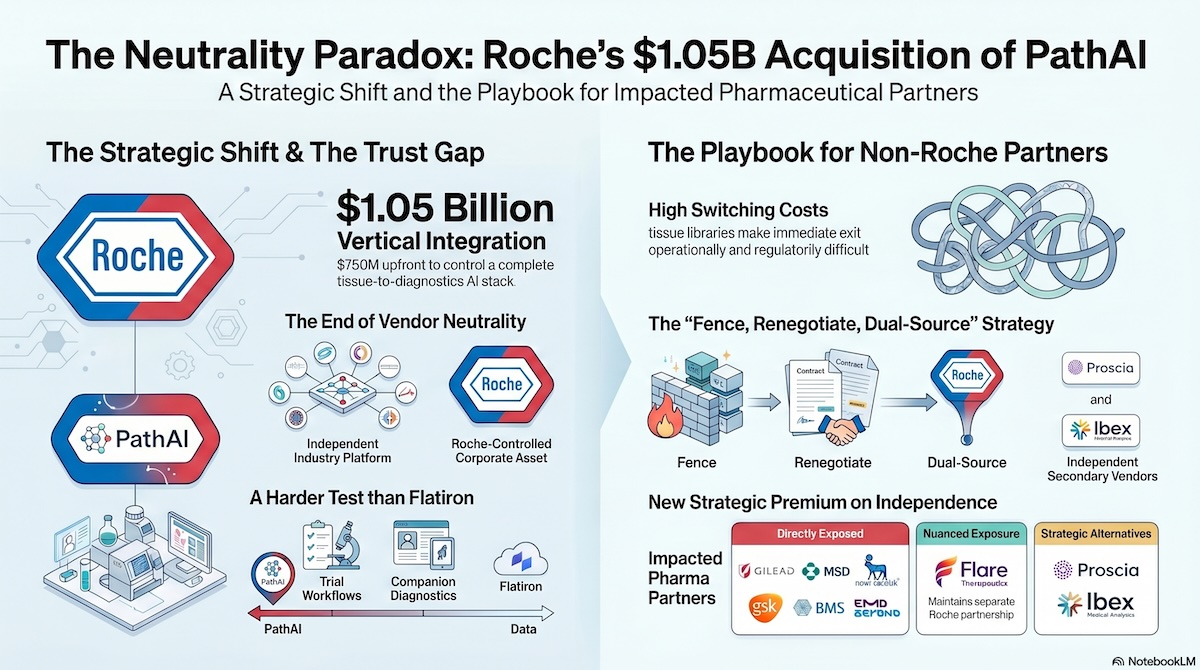

- Roche has disclosed an acquisition of PathAI worth up to $1.05bn, comprising $750mn upfront and up to $300mn in performance-linked milestones, with closing expected in the second half of 2026.

- The deal echoes Roche’s earlier acquisition of Flatiron Health, but PathAI presents a more direct neutrality test because it sits closer to companion diagnostics, biomarker scoring and trial pathology workflows — a harder test of whether Roche can preserve acquired infrastructure assets when they sit inside the operational core of diagnostics.

- PathAI had announced 10 pharma partnerships before the Roche acquisition; Roche and Genentech are within the Roche group, while Flare Therapeutics also has a separate Roche partnership since 2024, making its exposure more nuanced than a simple non-Roche counterparty classification would suggest. The most exposed non-Roche pharma partners include Gilead Sciences, MSD, Novo Nordisk, GSK, Bristol Myers Squibb, EMD Serono and Incendia Therapeutics.

- Roche’s upside is control of a tissue-to-diagnostics AI stack. Its risk is eroding the external partner ecosystem that made PathAI strategically valuable in the first place.

- PathAI gains scale, capital certainty and regulatory reach, but loses the strategic neutrality that helped it become an industry platform.

- The likely response from non-Roche partners is not immediate exit, but tougher firewalls, renegotiated data rights and dual sourcing for new programmes.

- The acquisition validates pathology AI while increasing the strategic premium on independent vendors such as Proscia and Ibex Medical Analytics.

- As digital health M&A accelerates, corporate partners need to treat vendor acquisition risk as a standing portfolio-governance discipline rather than an occasional legal review.

Roche’s move for PathAI looks, on first reading, like an obvious strategic fit. Roche is already a heavyweight in diagnostics. PathAI brings digital pathology, image management, AI-enabled biomarker analysis and a web of biopharma collaborations. The disclosed consideration — up to $1.05bn, split between $750mn in upfront cash and $300mn in milestones — is large enough to matter but not so large as to strain Roche’s balance sheet.

Yet the more interesting question is not what Roche gets. It is what everyone else loses, or fears losing.

PathAI was not a small software vendor selling dashboards into procurement departments. It was part of the infrastructure of modern translational research: algorithms within trials, whole-slide image workflows, annotated tissue datasets, biomarker scoring, and companion diagnostic development. Its customers and partners were not merely buying licences. In many cases, they were building scientific and regulatory pathways around the platform.

That is what makes this transaction strategically sharper — and politically more delicate — than the usual digital health acquisition. A vendor that sat between competing pharmaceutical companies is now set to sit inside one of them, or at least inside the Roche group’s diagnostics orbit. For PathAI’s other pharma partners, the question changes from “does the technology work?” to “can we still trust the operating model?”

Roche has been here before. Its acquisition of Flatiron Health in 2018 sparked a similar debate: could a pharma-owned oncology data platform continue to serve external stakeholders while maintaining trust with competitors, providers and regulators? The answer, in broad terms, was yes — but not without a permanent change in market perception. Flatiron showed that Roche can own strategic data infrastructure without destroying its external relevance. PathAI asks a harder question: whether that same model works when the platform is tied directly to pathology, biomarker strategy and companion diagnostics.

Roche is buying more than algorithms

The obvious reading of the deal is that Roche is buying digital pathology capability. That is true, but incomplete.

According to the transaction summary, Roche is acquiring PathAI’s AISight Image Management System, described as primary-diagnosis cleared by the FDA in 2025; trial-embedded algorithms across multiple biopharma sponsors; a companion-diagnostic algorithm pipeline co-developed since 2024; a workforce of 501 to 1,000 employees; and the data used to train the platform.

That combination matters because pathology AI is not valuable in the abstract. A model is only as strong as the data, workflow integration, validation history and clinical context behind it. In diagnostics, the scarce asset is not just code. It is trust: from pathologists, sponsors, regulators and laboratories. PathAI’s value lies in the fact that it had become part of those workflows before Roche acquired it.

For Roche, this offers three strategic merits.

The first is vertical control. Roche already has deep exposure to diagnostics, oncology and companion diagnostics through assets such as VENTANA and Foundation Medicine. Owning PathAI gives it a tighter link between tissue, image, algorithm and therapeutic decision-making. In oncology, where biomarker complexity is rising and tissue remains central, that is a meaningful advantage.

The second is data accumulation. AI pathology businesses are, in practice, data businesses with regulatory obligations attached. The ability to aggregate labelled tissue images, annotations and algorithmic performance across studies can create a compounding advantage. Even where contractual restrictions limit cross-use, the organisational learning from running these programmes is valuable.

The third is strategic optionality. PathAI gives Roche a platform that can support drug development, diagnostic development and potentially clinical deployment. A point solution would be easier to value. A platform spanning research, development, and diagnostics is more difficult to price — and therefore potentially more valuable if Roche executes well.

But the same logic creates risk. Roche is not simply integrating a product. It is absorbing a counterparty whose neutrality was part of its commercial appeal.

Flatiron is the precedent — but not the answer

The obvious precedent is Roche’s acquisition of Flatiron Health. It is also the wrong precedent to use lazily.

Flatiron was a strategic infrastructure acquisition. Roche bought a company that had become important to oncology, real-world data, evidence generation and clinical workflow. The concern at the time was predictable: would a Roche-owned data platform remain trusted by other pharma companies, health systems and research partners?

In retrospect, Flatiron gives Roche a credible defence. The business did not simply disappear into Roche. It retained a visible external identity, continued to operate as a specialist oncology data company and remained relevant to stakeholders beyond Roche’s own pipeline. That is a useful signal for PathAI’s partners. Roche can plausibly argue that it has experience in preserving the market value of a platform whose usefulness depends on more than internal synergies alone.

But Flatiron is not a free pass.

The difference is proximity to competition. Flatiron primarily focused on oncology data infrastructure and real-world evidence. PathAI sits closer to the operational core of diagnostics: tissue-image analysis, biomarker scoring, algorithmic pathology workflows, and companion diagnostic development. The conflict is therefore not merely about who can see what data. It is about who influences the diagnostic pathway that may determine how a therapy is developed, validated and commercialised.

That distinction matters. A pharma company may tolerate a competitor owning a portion of its evidence infrastructure if the governance is credible. It may be less relaxed about a competitor owning the AI platform used to score tissue, develop biomarkers, or support a companion diagnostic strategy in overlapping indications.

Flatiron lived adjacent to therapeutic competition. PathAI may sit inside it.

That is why this transaction should not be framed as “Roche has done this before”. It should be framed as “Roche has earned the right to try, but the test is harder this time”.

PathAI gains scale, but may lose neutrality

For PathAI, the merits are clear. A $750mn upfront payment with up to $300mn in milestones offers certainty in a venture market that has become less forgiving of capital-intensive digital health companies. Pathology AI is not a lean SaaS category. It requires regulatory work, clinical validation, enterprise deployment, high-quality data infrastructure and a specialist commercial motion. Those things are expensive.

Roche offers PathAI global reach, diagnostic credibility, and a route to scaled clinical adoption. A standalone PathAI would have had to keep persuading investors that the market was arriving quickly enough to justify continued burn and regulatory cost. Inside Roche, the company gains a patient parent, distribution, and a strategic need.

There is also a scientific argument for the transaction. PathAI’s technology can be more useful when embedded in a broader diagnostics stack. Digital pathology has long suffered from fragmentation: scanners, image management systems, laboratory workflows, algorithms, clinical reporting and regulatory frameworks often sit in separate commercial silos. Roche can plausibly argue that integration will accelerate adoption.

Yet PathAI’s biggest risk is the loss of perceived independence.

Before the acquisition, PathAI could present itself as a specialist technology partner serving the sector. After the acquisition, every strategic decision will be read through a Roche lens. Which indications receive investment? Which companion-diagnostic programmes receive senior attention? Which pharma sponsors receive the best service levels? Which datasets are ring-fenced, and how convincingly?

This does not require misconduct to become a problem. In enterprise healthcare, perception is often enough. A partner need not worry that its data will be misused to believe that product priorities will drift. A sponsor does not need proof of preferential treatment to worry that a Roche-aligned programme will move faster. A rival pharma company does not need a smoking gun to conclude that future biomarker work should be dual-sourced.

That is the paradox for PathAI. Roche gives it scale. Roche also makes trust more expensive.

The other pharma partners now have a competitor inside the vendor

The most important sentence in the deal analysis is not about the purchase price. It is that PathAI had 10 pharma partnerships before the acquisition, only two of which — Roche and Genentech — are plainly inside the Roche group.

The named partners include Gilead Sciences before 2019, MSD in November 2019, Genentech in June 2021, Roche in October 2021, Novo Nordisk in November 2021, GSK in April 2022, Bristol Myers Squibb in August 2022, Flare Therapeutics in October 2023, EMD Serono in April 2024 and Incendia Therapeutics in November 2024.

That list needs one important qualification. Flare Therapeutics is not merely an arm’s-length counterparty in this context: it has also maintained a separate partnership with Roche since 2024. That makes Flare’s position more nuanced than the other non-Roche PathAI partners. It may still need to review its PathAI exposure, but its strategic alignment with Roche is different from that of a direct large-pharma competitor.

For Gilead, MSD, Novo Nordisk, GSK, Bristol Myers Squibb, EMD Serono and Incendia, the issue is more direct. A previously independent pathology AI partner now sits inside a major diagnostics and therapeutics group with its own commercial priorities.

The first issue is roadmap priority drift. PathAI’s product roadmap will now be set, formally or informally, within Roche Diagnostics. That does not mean all non-Roche programmes will be neglected. Roche has every incentive to preserve revenue, credibility and ecosystem value. But algorithm priorities, indication coverage and validation timelines will inevitably be assessed against Roche’s own portfolio and diagnostics strategy. In companion diagnostics, where Roche has direct ambitions, the tension is obvious.

The second issue is data and intellectual property governance. Existing partnerships may include confidentiality obligations, data-use restrictions, derivative IP provisions, and sponsor-specific controls. But many of those agreements were likely drafted for a venture-backed vendor, not for one acquired by a major diagnostics competitor. Tissue images, annotations, and trained model weights generated under partnership arrangements now reside within a new corporate structure. The legal question may be manageable. The governance question is harder.

The third issue is channel conflict. Roche has a direct companion-diagnostics franchise. PathAI has supported biomarker programmes for pharma partners that may compete with Roche therapeutics, Roche diagnostics or both. The same vendor that supports a competing sponsor’s biomarker strategy now reports into a group with its own diagnostic profit-and-loss logic. That conflict is no longer theoretical. It is structural.

This is why PathAI’s other partners should treat the deal as a portfolio governance event rather than a procurement update.

Switching away is harder than it sounds

The conventional corporate response to vendor risk is to threaten substitution. In this case, that threat is only partly credible.

PathAI is sticky because the assets built on top of it are sticky. The carousel identifies four categories of embedded exposure: trial-embedded algorithms, tissue and annotation libraries, companion diagnostic timelines, and regulatory submissions. Each creates a different form of switching cost.

Trial-embedded algorithms may already be running inside Phase II or Phase III biomarker workstreams. Replacing them mid-trial is not like switching CRM systems. It may require revalidation, protocol amendments, changes to statistical analysis plans and fresh regulatory engagement. The cost is measured not only in dollars but in time, evidence continuity and clinical risk.

Tissue and annotation libraries are similarly difficult. Years of curated whole-slide image datasets and pathologist labels are not easily recreated. Even where ownership is clear, downstream use rights may need to be reread after a change of control. The value is not just the raw image. It is the combination of tissue, context, labels, quality controls and algorithmic history.

Companion-diagnostic programmes add another layer. A CDx timeline is often tied to a therapeutic development plan. Delays in assay validation, algorithm performance or regulatory submission can affect drug launch strategy. If a non-Roche sponsor believes its CDx programme is now competing internally with Roche’s priorities for resources, it has a fiduciary duty to ask uncomfortable questions.

Regulatory submissions may be the most underappreciated exposure. If a sponsor has referenced PathAI assets, workflows or outputs in a regulatory dossier, the counterparty change matters. Regulators may not object to a change of ownership, but sponsors will want a clean record of continuity, data integrity and post-acquisition control.

The result is asymmetric. PathAI’s partners may want leverage, but Roche knows many cannot simply walk away. That gives Roche commercial strength. It also gives it reputational responsibility.

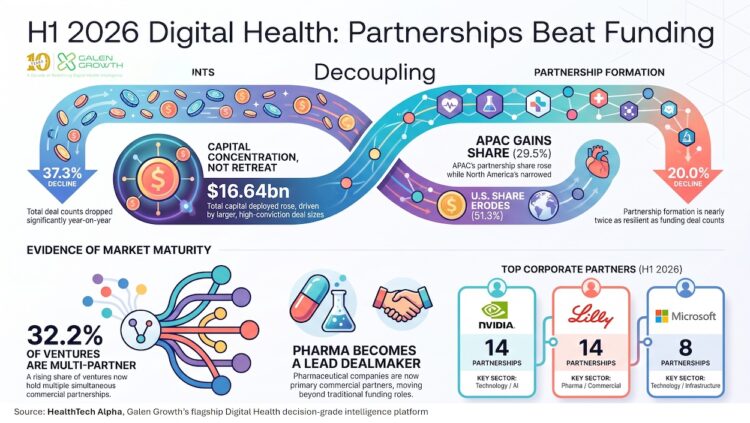

Digital health M&A is turning partner risk into portfolio risk

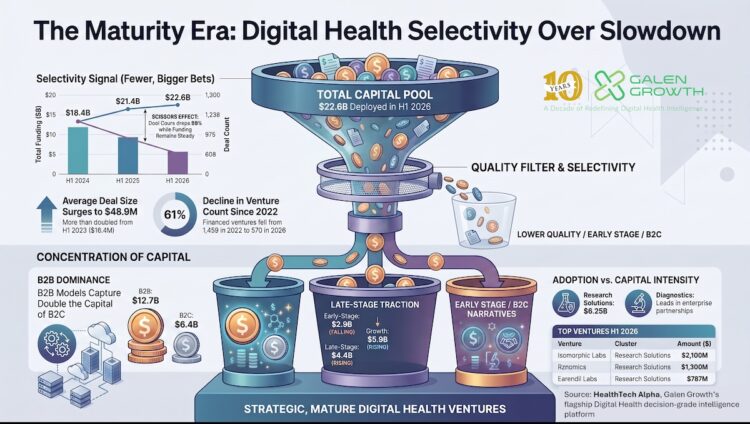

The Roche-PathAI transaction should not be treated as an isolated event. It is part of a broader shift in digital health: as funding markets tighten, strategic acquirers are increasingly able to buy infrastructure assets that were previously venture-backed, independent and widely partnered.

That creates a new class of risk for corporate partners.

The traditional diligence question was: “Is this venture credible enough to partner with?” The more important question is becoming: “Who might own this venture in three years, and what would that do to our strategic exposure?”

This matters because digital health partnerships are no longer peripheral innovation theatre. They increasingly sit inside clinical trials, diagnostic pathways, patient engagement models, real-world evidence generation, reimbursement workflows and provider operations. When such a vendor is acquired, the consequences can extend beyond procurement. They can affect data access, competitive intelligence, regulatory continuity, commercial strategy and enterprise architecture.

The problem is especially acute in categories where the same asset can serve multiple competing stakeholders. AI pathology is one. Oncology real-world data is another. Clinical trial technology, decentralised trial infrastructure, remote monitoring, imaging AI, patient identification, digital biomarkers and care-navigation platforms all create similar tensions. A vendor can be strategically useful because it is neutral, and strategically problematic the moment that neutrality disappears.

For pharmaceutical companies, providers, payers and medtech groups, this requires a more disciplined approach to partner governance. Change-of-control clauses should no longer be boilerplate. Data rights, model-training permissions, derivative IP ownership, sponsor-specific firewalls, audit rights, continuity provisions, and exit mechanics need to be negotiated as strategic protections, not legal afterthoughts.

This is where Galen Growth’s role becomes material. The firm’s HealthTech Alpha platform tracks more than 16,000 digital health ventures, including their funding, maturity, evidence, partnerships and corporate relationships. That allows strategic partners to map not only which ventures are credible, but also which are becoming strategically crowded, acquisition-prone, or competitively conflicted.

In an M&A-heavy market, the value of intelligence is not a list of interesting start-ups. It is the ability to see dependency before it becomes exposure. Galen Growth helps corporates answer the questions that matter before a transaction forces them to do so: which vendors are embedded across our portfolio, which competitors partner on the same assets, which ventures are plausible acquisition targets, and which contracts require governance upgrades before ownership changes.

The PathAI case is a warning shot. Vendor M&A is no longer only a cap-table event. It is a partner-risk event.

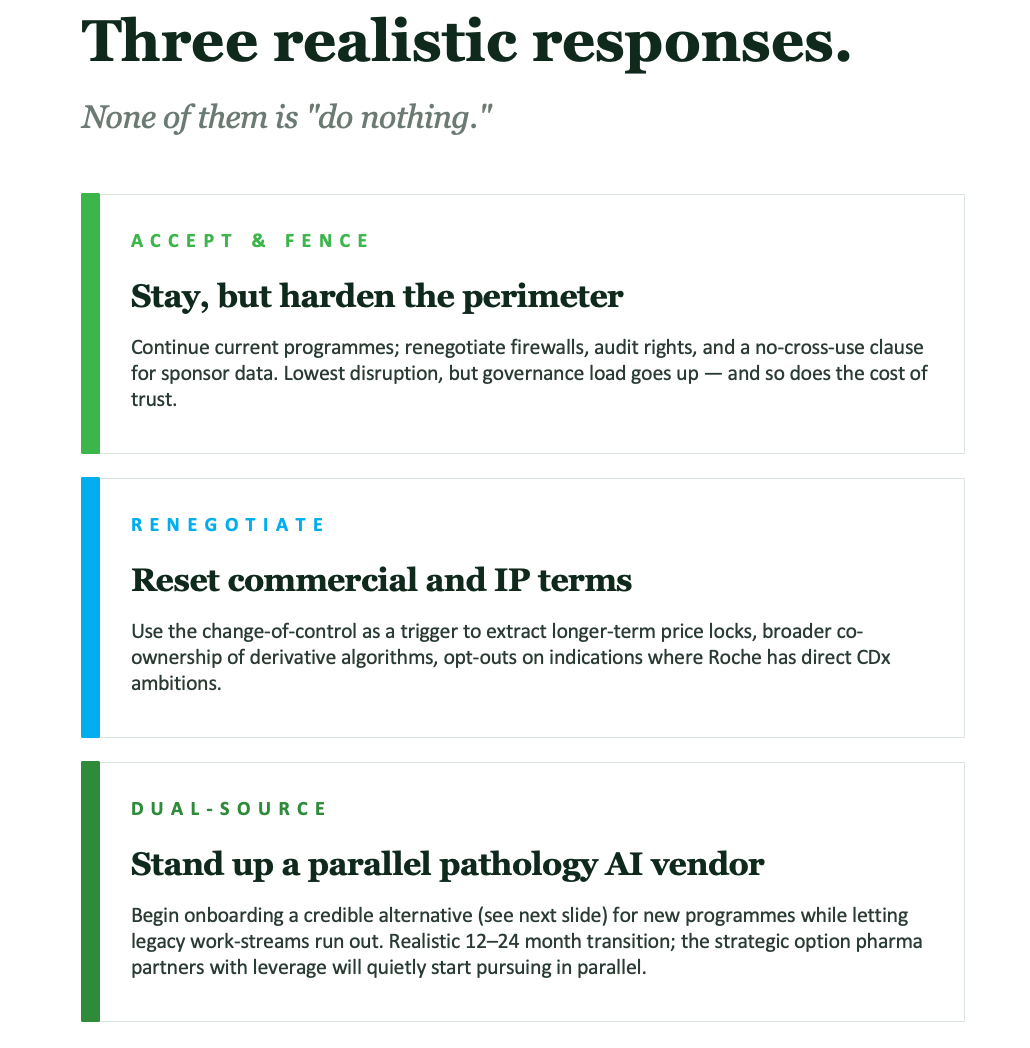

The right partner response is not panic. It is fencing.

For PathAI’s other pharma partners, the wrong answer is immediate exit. The second wrong answer is doing nothing.

The realistic playbook has three moves: accept and fence, renegotiate, and dual source.

“Accept and fence” means continuing current programmes while hardening governance. Sponsors should seek explicit firewalls, audit rights, sponsor-data segregation, no cross-use provisions, and clear rules on derivative algorithms. The purpose is not theatrical legalism. It is to convert trust from a relationship assumption into an enforceable operating model.

Renegotiation should follow. A change of control is a commercial moment. Sponsors with meaningful programmes should use it to seek price locks, continuity commitments, step-in rights, expanded access to outputs, clearer co-ownership of derivative IP, and opt-outs in indications where Roche has direct companion diagnostic ambitions. The strongest sponsors will not frame this as punishment. They will frame it as the cost of continuing after neutrality has changed.

Dual sourcing is the strategic hedge. Partners do not need to rip PathAI out of active programmes. They do need alternatives for new ones. The shortlist is not long. The carousel identifies Proscia and Ibex Medical Analytics as the closest pure-play independent peers, both with partnership maturity scores above 89 in HealthTech Alpha, while noting that neither is a one-for-one replacement. Aidoc, Scopio Labs and others may be relevant in adjacent use cases, but histopathology AI at pharma-grade maturity remains a narrow field.

This is precisely why the time to act is before closing, not after it. Once the transaction is completed and integration is underway, the negotiating leverage of non-Roche partners will decline.

The risk to Roche is ecosystem erosion

Roche’s biggest risk is not that the acquisition fails technically. It is PathAI’s ecosystem value that decays after ownership changes.

Many corporate acquirers underestimate this problem. They buy a networked asset and then manage it as a captive capability. That can work when the target’s value lies in internal synergies. It is dangerous when the target’s value lies partly in its external neutrality.

If MSD, Novo Nordisk, GSK, Bristol Myers Squibb, EMD Serono, Gilead and Incendia each become more cautious, PathAI’s partnership network becomes less dynamic. New sponsors may hesitate. Existing sponsors may limit scope. Sensitive programmes may move elsewhere. Data flows may narrow. The platform may remain technically excellent while becoming commercially less trusted. Flare Therapeutics, given its separate Roche partnership, may sit in a different category — but even there, the governance questions do not disappear.

Roche can mitigate this, but only if it treats governance as a product feature. That means formal separation where needed, transparent data controls, independent audit mechanisms, contractual commitments that survive organisational reshuffles and a credible assurance that non-Roche programmes will not become second-class citizens.

Flatiron provides a partial model here. Roche can preserve acquired infrastructure if it avoids suffocating the asset inside its own organisation. But PathAI requires a stronger version of the Flatiron playbook. Real-world data governance is one problem. AI-enabled tissue analysis tied to companion diagnostics is another.

There is precedent in other sectors. Cloud providers serve competitors. Contract research organisations work across rival drugmakers. Diagnostics companies partner broadly while pursuing their own strategic agendas. Conflict can be managed. But it must be managed explicitly.

The hard part is cultural. Roche must resist the temptation to view all PathAI assets through the lens of internal portfolio advantage. If it does not, it may win the acquisition and shrink the market opportunity.

What this means

For Roche: The acquisition gives it a credible shot at owning more of the digital pathology and companion diagnostics stack. The strategic prize is vertical integration across tissue, image, algorithm and diagnostic decision-making. The execution risk is partner distrust: Roche must preserve PathAI’s external credibility or risk turning a platform asset into a captive tool.

For PathAI: The transaction brings capital certainty, scale and diagnostics infrastructure. It also ends the company’s claim to vendor neutrality. PathAI’s management challenge will be to keep non-Roche partners confident that the platform’s roadmap, service levels and data governance remain commercially fair.

For pharma and corporate partners: The most exposed non-Roche partners should treat this as a live governance event. Active trials may remain with PathAI, but contracts should be reviewed now for change-of-control rights, confidentiality, derivative IP, data-use restrictions, audit rights and termination mechanics. New programmes should be assessed against a dual-source strategy.

For strategic digital health partners more broadly: The PathAI case shows why partner portfolios need continuous surveillance. A vendor that appears safe to sign can become strategically conflicted after an acquisition. Corporations should map shared vendors, competitor relationships and likely acquirers before those risks crystallise.

For investors: The deal validates pathology AI as a strategic acquisition category and shows that independence itself can be a source of enterprise value. Investors should pay closer attention to whether AI vendors are building neutral infrastructure for many sponsors or becoming acquisition targets for one strategic buyer.

For digital pathology ventures: Roche’s move validates the category. It also creates a commercial opening for independent vendors such as Proscia and Ibex Medical Analytics. Their pitch is no longer only performance. It is independence.

For Galen Growth clients: The transaction is a practical example of why venture intelligence and partnership intelligence need to be read together. Funding history, partnership density, evidence maturity, corporate overlap and acquisition probability are not separate data points. They are the risk map.

FAQ

How much is Roche paying for PathAI?

Roche disclosed a transaction worth up to $1.05bn, with $750mn upfront in cash at closing and up to $300mn in performance-linked milestones. Closing is expected in the second half of 2026.

Why does the Roche-PathAI deal matter to other pharma companies?

PathAI had announced 10 pharma partnerships before the acquisition, and most sit outside the Roche group. Those partners now face changes in vendor ownership, data governance, and potential conflicts with companion diagnostics.

Which pharma companies partnered with PathAI before the Roche acquisition?

The announced partnership stack includes Gilead Sciences, MSD, Genentech, Roche, Novo Nordisk, GSK, Bristol Myers Squibb, Flare Therapeutics, EMD Serono and Incendia Therapeutics. Flare Therapeutics also has a separate partnership with Roche since 2024, which makes its position more nuanced than a simple non-Roche exposure.

What is the Flatiron precedent?

Roche’s acquisition of Flatiron Health showed that a pharma-owned oncology data infrastructure company can continue to serve external stakeholders if the acquirer preserves operational independence, governance and trust. The PathAI deal is a harder test because PathAI sits closer to companion diagnostics, biomarker scoring and trial pathology workflows.

Why is PathAI potentially more sensitive than Flatiron?

Flatiron was primarily an oncology data and real-world evidence platform. PathAI is involved in digital pathology, tissue-image analysis, algorithms, and companion diagnostic workstreams. That places it closer to decisions that can shape therapeutic development and the commercialisation of diagnostics.

What is the main risk for Roche?

The main risk is not integration failure but ecosystem erosion. If non-Roche partners conclude that PathAI is no longer neutral, they may reduce scope, demand tighter controls or move new programmes to alternative vendors.

What should PathAI’s other partners do now?

They should review contracts before closing, seek stronger data and IP protections, negotiate roadmap and continuity commitments, and begin dual-sourcing for new pathology AI programmes where clinically and operationally feasible.

Why does digital health M&A increase risk for strategic partners?

Digital health ventures increasingly sit inside clinical, regulatory and commercial workflows. When a strategic vendor is acquired by a competitor or adjacent market participant, the risk shifts from procurement to portfolio governance: data rights, IP, continuity, roadmap priority and competitive exposure all need to be reassessed.

How can Galen Growth help strategic partners mitigate this risk?

Galen Growth’s HealthTech Alpha platform tracks more than 16,000 digital health ventures, including signals on maturity, evidence, funding, and partnerships. That makes it possible to identify shared vendor exposure, competitor overlap, acquisition-prone assets and governance risks before a transaction changes the balance of power.

Closing view

The Flatiron precedent gives Roche credibility. It does not give it a free pass.

Roche’s acquisition of Flatiron normalised the idea that pharma-owned data infrastructure can remain commercially useful to competitors. The acquisition of PathAI will test a harder question: whether competitors will still trust a Roche-owned platform when it sits inside the companion-diagnostics and biomarker-development workflow.

Oncology data infrastructure was one thing. AI-enabled pathology, trial-embedded biomarker workflows, and companion diagnostics are other examples.

The broader lesson reaches well beyond Roche. Digital health M&A is turning vendor ownership into a strategic-risk variable. Any corporation that builds on venture-backed infrastructure must now ask not only whether the technology works, but who might control it next.

If Roche wants PathAI to remain a platform rather than become a captive asset, it will have to make neutrality contractual, auditable and commercially visible. The burden of trust has moved from PathAI’s brand to Roche’s governance.

For everyone else, the message is simpler: map your dependencies before the acquirer does.

Data source and methodology

Data source: HealthTech Alpha by Galen Growth. The analysis reflects disclosed transaction terms, announced partnerships and HealthTech Alpha maturity indicators presented in the source material. Deal figures are in US dollars. Partnership exposure reflects announced relationships, not undisclosed commercial arrangements.

Related Galen Growth analysis

- Digital pathology market intelligence — Galen Growth

- AI in diagnostics research — Galen Growth

- Digital health M&A trend analysis — Galen Growth

How to cite this analysis

About Galen Growth

Galen Growth is the digital health intelligence firm behind HealthTech Alpha, the leading ontology-driven platform tracking the global digital health ecosystem. With operating entities in the US, Europe and Asia, we combine large-scale labelled data, auditable GenAI research and explainable analytics to advise pharma, medical device, insurance, health system, investor and startup clients.