Digital health liquidity remains steady, but the market has changed. For investors, corporates, and ventures, the winning strategy is less about waiting for an IPO window and more about building strategically relevant, capital-efficient companies that can endure a longer path to exit.

KEY TAKEAWAYS

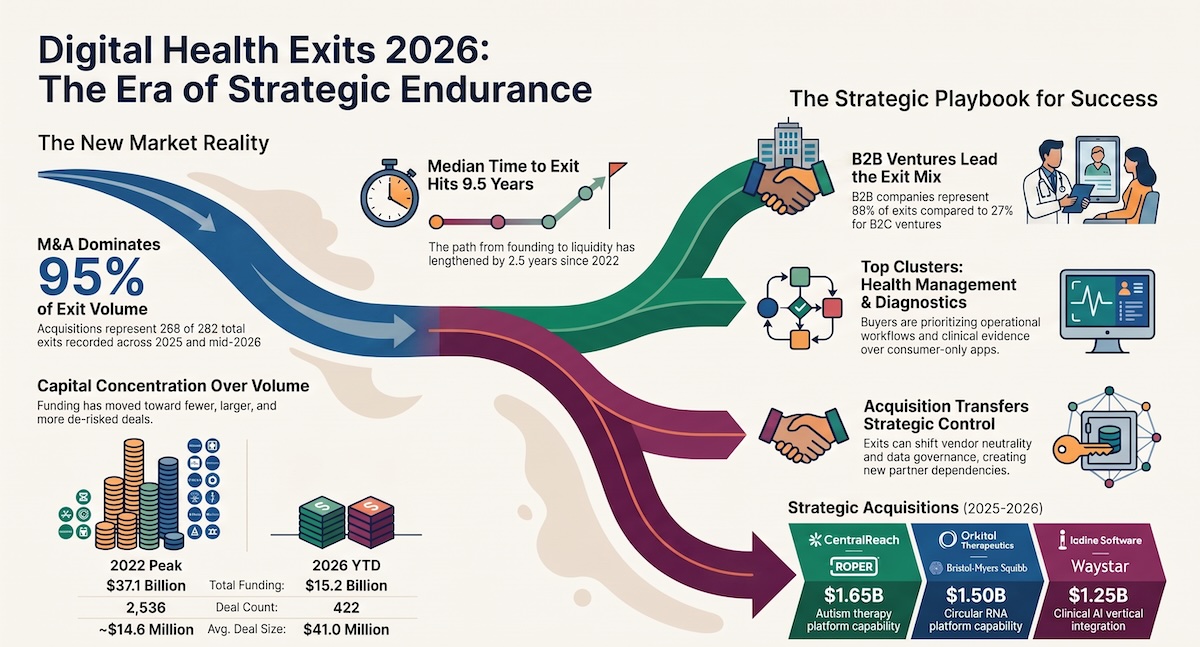

- M&A is the primary exit route for digital health. Across 2025 and the first half of 2026, acquisitions represented 268 of 282 exits, or 95% of total exit volume.

- The time horizon has lengthened. Median time from founding to exit has increased from roughly seven years in 2022 to 9.5 years in 2026, with corporate buyers typically acquiring companies two to three years later than venture buyers.

- Capital is concentrating rather than disappearing. Funding is well below the 2022 peak, but average deal size has risen to $41.0M in 2026 YTD, indicating a preference for fewer, larger, more de-risked rounds.

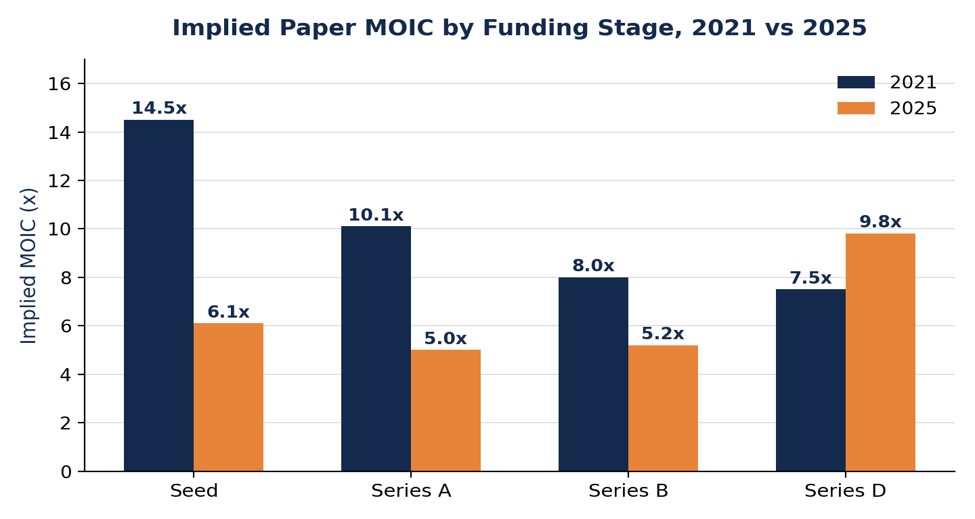

- Early-stage markups are under pressure. Implied Seed MOIC has fallen from 14.5x in 2021 to 6.1x in 2025, while Series A MOIC has more than halved over the same period.

- Strategic ownership matters. Roche’s proposed acquisition of PathAI illustrates how exits can reshape vendor neutrality, data governance, and partner dependencies beyond the liquidity event itself.

M&A should be treated as the base case, not the fallback

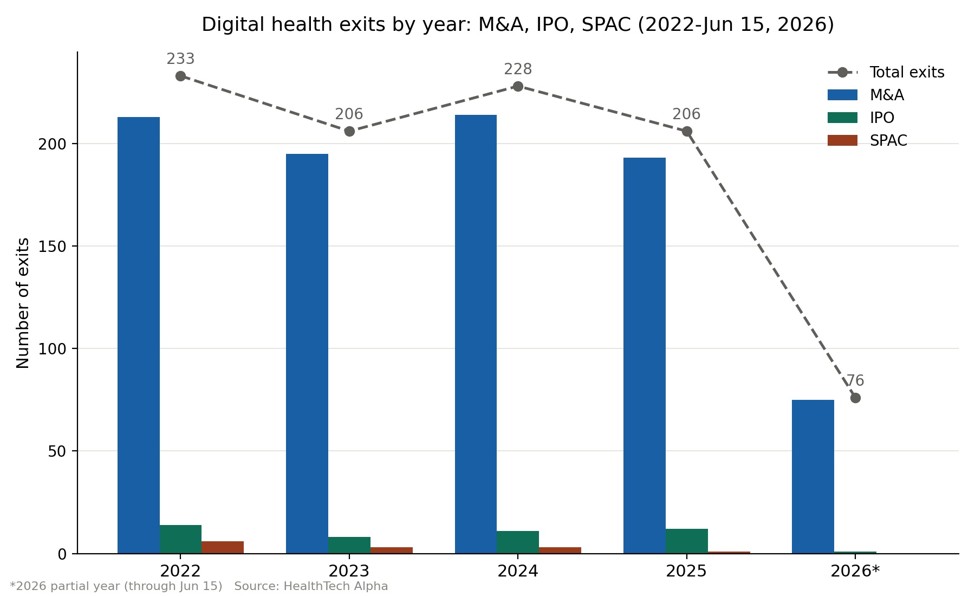

The new route to liquidity is overwhelmingly strategic for Digital Health startups. Of 282 exits recorded across 2025 and the first half of 2026, 268 were acquisitions. M&A has represented at least 91% of digital health exit volume every year since 2022 and reached 99% in 2026 YTD. By contrast, SPAC activity has effectively stopped, with one transaction in 2025 and none recorded yet in 2026 YTD (the Freenome SPAC was expected in H1 2026 but has not yet closed).

For venture investors, that changes underwriting. A credible exit thesis should start with a clear strategic-buyer map, likely acquisition rationales, and the operational milestones that would make the company indispensable to those buyers. For founders, it means building around the question a buyer will eventually ask: what capability, distribution advantage, clinical evidence, data asset, or workflow position does this company control that is difficult to replicate?

For corporate development teams, the same data signals that acquisition opportunities are abundant but increasingly selective. The market is not rewarding generic growth stories; it is rewarding assets that solve a defined capability gap or accelerate a strategic roadmap.

The exit bar has risen as capital has become more selective

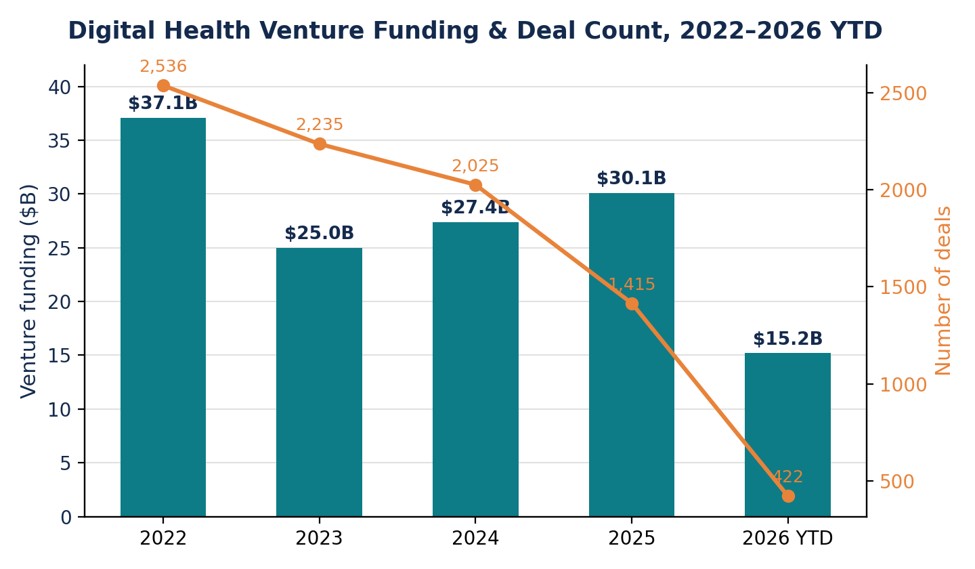

The funding environment provides important context for exit behaviour. Digital health venture funding peaked at $37.1B across 2,536 deals in 2022, fell to $25.0B in 2023, and has since recovered unevenly. In 2026 YTD, funding stands at $15.2B across 422 deals, implying an average deal size of $41.0M – the highest level in the five-year period.

This is not a market in which capital has disappeared. It is a market in which capital is being allocated more narrowly. Investors are reserving larger cheques for companies with stronger evidence, clearer commercial traction, and a more explicit path to strategic relevance. The same filter is visible in exits: acquirers are buying proven assets rather than funding unresolved risk.

Median time to exit has expanded from roughly seven years in 2022 to 9.5 years in 2026. Corporate acquirers consistently buy companies two to three years more mature than venture-to-venture acquirers, reflecting the higher bar for enterprise readiness, integration fit, evidence, and governance. More than 60% of exiting companies had reached Series B or beyond before exit, while the median last funding round before M&A was only $7.7M. That combination points to capital efficiency, not capital intensity, as the more durable route to liquidity.

What strategic buyers are paying for

The strongest acquisition patterns are forming around infrastructure, workflows, and capabilities that are directly relevant to enterprise customers and corporate roadmaps. Health Management Solutions led exit clusters with 60 exits across 2025-2026 YTD, followed by Patient Solutions, Medical Diagnostics, and Population Health Management. These are not single-feature consumer applications; they are categories tied to operational workflows, clinical evidence, and enterprise adoption.

Business-model mix reinforces the point. B2B ventures accounted for 69% of exits, compared with 27% for B2C ventures. In the current market, workflow-embedded technologies with clear buyer value are more likely to attract strategic interest than stand-alone products that depend primarily on consumer acquisition or broad market expansion.

The largest disclosed transactions also show a targeted strategic logic. Roper’s $1.65B acquisition of CentralReach added a vertical ABA and autism therapy platform. Waystar’s $1.25B acquisition of Iodine Software embedded clinical AI into the revenue-cycle and coding stack. Hims & Hers’ acquisition of Eucalyptus, valued at up to $1.11B, expanded distribution into Australia, Japan, and Europe. These are capability, infrastructure, and channel acquisitions – not generalised bets on sector momentum.

| Venture | Acquirer | Value | Strategic rationale |

| CentralReach | Roper Technologies | $1.65B | Capability buy — ABA/autism therapy platform |

| Orbital Therapeutics | Bristol-Myers Squibb | $1.50B | Capability buy — circular RNA platform |

| Iodine Software | Waystar | $1.25B | Vertical integration — clinical AI for coding |

| Eucalyptus | Hims & Hers | $1.11B | Channel expansion — AU/Japan/EU telehealth |

| Talkspace | Universal Health Services | $865M | Consolidation — behavioural health |

The IPO window remains narrow

Recent public-market activity may create the impression that the exit environment is broadly reopening. SpaceX’s record $75B Nasdaq listing on 12 June 2026 and confidential S-1 filings from companies such as Oura and Strava suggest investor appetite for scaled, high-quality growth assets. For digital health, however, the evidence still points to a selective IPO market rather than a broad reopening.

Digital health IPO volume peaked at 57 listings in 2021 and has not exceeded 14 annual listings in any year since. In 2026 YTD, the market has recorded only one listing. Recent public companies such as Saluda Medical, Hinge Health, and HeartFlow share characteristics that most ventures have not yet achieved: multi-year clinical evidence, clearer reimbursement positioning, and substantial revenue scale, often $100M or more in ARR before filing.

The implication for investors and founders is straightforward: IPO readiness is a high-quality signal, but it should not be the default liquidity assumption. The companies most able to access public markets are typically those that have already proven enough to have multiple strategic options.

Exits also transfer control

An acquisition does more than deliver liquidity. It can alter the competitive position, governance model, and data-control dynamics of the acquired company’s customers and partners. Roche’s proposed acquisition of PathAI, valued at up to $1.05B, is a useful example. PathAI was embedded across ten pharmaceutical partnerships, including GSK, MSD, Novo Nordisk, and Bristol Myers Squibb. Seven of those partners sit outside the Roche Group, meaning the transaction could shift formerly neutral trial infrastructure into the ownership of a direct competitor.

For corporate partners, pharma companies, and health systems, this is not simply a legal issue. Change-of-control clauses are important, but they do not fully answer whether a previously neutral vendor remains neutral under new ownership. Vendor concentration across discovery, diagnostics, clinical workflow, and infrastructure categories introduces strategic-dependency risk that should be assessed before a transaction occurs, not after the press release.

For acquirers, this also raises an integration question. Preserving customer trust may require explicit governance protections, data-boundary commitments, and transparent partner communications. In a market where strategic buyers are consolidating infrastructure assets, managing neutrality may become a competitive advantage in its own right.

Endurance is now the operating strategy

The market is not closed. It is more disciplined. Funding is concentrating into fewer rounds, early-stage paper returns have compressed, and the typical M&A path now takes close to a decade. That environment favours ventures that can extend runway, prove enterprise value, and make themselves strategically necessary without relying on repeated valuation step-ups to sustain the story.

For founders, endurance means making strategic relevance part of the company-building plan from the beginning. The practical question is not only how large the market could become, but which buyer would eventually need this capability, what evidence would make the asset hard to ignore, and what integration risk must be removed before acquisition becomes viable.

For investors, endurance means explicitly underwriting longer hold periods and more conservative markup-to-distribution assumptions. It also means favouring companies with capital-efficient growth, clear evidence plans, and multiple strategic-buyer pathways over companies that primarily demonstrate momentum through fundraising.

For corporates, endurance means building a more systematic view of the acquisition landscape. As valuations normalise and point solutions seek strategic homes, corporate buyers have an opportunity to acquire capabilities that would take years to build internally. The best opportunities will not necessarily be the loudest fundraising stories; they will be the companies with defensible workflow position, evidence, and customer trust.

What this means for each audience

| Audience | Implication |

| Investors | Model M&A as the base-case exit for most holdings. Underwrite longer hold periods, lower reliance on paper markups, and greater value on capital efficiency, evidence, and strategic-buyer fit. |

| Founders and ventures | Build with the buyer thesis in mind. Identify the capability gap you close, the evidence required to validate it, and the operating milestones that make the company easier to acquire and integrate. |

| Corporate development teams | Use the current market to identify infrastructure and workflow assets that fill a strategic roadmap gap. Prioritise assets with enterprise adoption, defensible data, and manageable integration risk. |

| Pharma and corporate partners | Treat vendor acquisition as a governance trigger. Map platform dependencies, strengthen change-of-control provisions, and assess who could control critical infrastructure next. |

| Health systems and policymakers | Recognise the upside of stronger, better-funded infrastructure, while scrutinising vendor neutrality, data governance, and concentration risk as strategic ownership changes. |

Frequently asked questions

Is the digital health IPO window reopening in 2026?

Only selectively. Public-market activity has improved for scaled, high-quality growth companies, but digital health IPO volume remains far below the 2021 peak and is still limited to a small number of category leaders.

Why is M&A so dominant in digital health exits?

Strategic buyers are the most consistent liquidity route because they can value specific capabilities, data assets, workflows, and distribution advantages even when public-market appetite remains selective.

What does the Roche-PathAI example show?

It shows that an exit can change more than ownership of the target. It can reshape governance, data access, vendor neutrality, and competitive dependencies for customers and partners.

Why have early-stage paper returns compressed?

Valuations have moved away from narrative-driven growth and toward evidence, commercial traction, and buyer relevance. As a result, early-stage markups are less generous than they were in 2021.

What should founders do differently?

Plan for a longer path to exit, prioritise capital efficiency, and define early which strategic buyers would value the company and what proof points those buyers will require.

Data source and methodology

Data source: HealthTech Alpha by Galen Growth, accessed June 2026, covering exit volume, route mix, disclosed deal value, cluster and business-model distribution, funding context, time-to-exit, and M&A strategic rationale across the global digital health ecosystem. Figures are in USD unless stated otherwise; some totals may be understated where transaction terms are undisclosed.

Additional company and risk-assessment detail is drawn from Galen Growth’s “Exits are Back. Easy Exits Aren’t. Digital Health 2026” report, published June 2026, based on HealthTech Alpha’s tracking of 16,000-plus digital health ventures.