Galen Growth’s proprietary ranking of the world’s most promising early-stage digital health startups reveals a global sector defined by capital discipline, AI-native architectures, and a decisive shift toward clinical validation — not just product launches.

Published March 2026 | Based on HT250 data as at 1 February 2026 | Powered by HealthTech Alpha

TL;DR

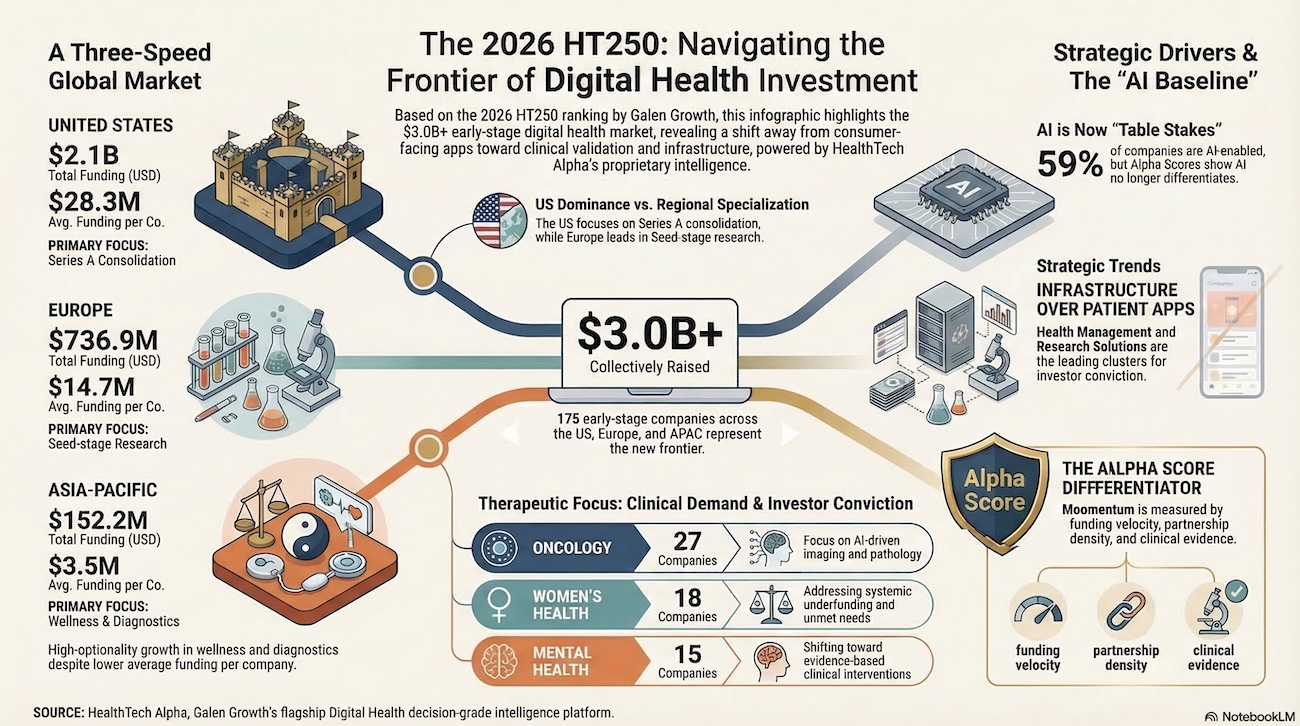

- 175 early-stage digital health companies across the US, Europe, and Asia-Pacific collectively raised over $3.0B in disclosed funding, with the US accounting for 70% of total capital deployed.

- 59% of HT250 companies are AI-enabled — yet AI is not a differentiator on its own; it is now table stakes. Alpha Scores are nearly identical between AI and non-AI cohorts.

- Health Management Solutions and Research Solutions dominate globally, signalling that investors are backing infrastructure and discovery — not only patient-facing apps.

- Europe is a Seed-heavy innovation engine; APAC is capital-lean but rapidly accelerating in wellness and diagnostics; the US is firmly in Series A consolidation mode.

- Oncology, Women’s Health, Mental Health, and Cardiovascular Diseases are the leading therapeutic focus areas among top-ranked companies, pointing to where clinical demand and investor conviction converge.

- The HT250 is built on HealthTech Alpha, a structured proprietary intelligence platform tracking 50,000+ companies and 16,000+ investors — a dataset that is itself a strategic asset in a GenAI era where structured domain data is increasingly scarce and valuable.

From Noise to Intelligence: Why the HT250 Matters Now

Every year, the digital health sector generates thousands of new ventures, millions of press releases, and billions of dollars of investor activity. The signal-to-noise ratio has never been worse — and the stakes have never been higher. For venture capitalists, corporate strategists, pharma business development teams, and health system leaders, the challenge is not finding startups. It is finding the right ones, at the right moment, with the right fundamentals.

This is exactly the problem the Galen Growth HT250 was designed to solve. The 2026 edition — a curated ranking of the most promising early-stage digital health companies across the globe — is not a list of funded darlings or conference-circuit favourites. It is a structured, evidence-informed intelligence product, powered by the HealthTech Alpha platform, that applies quantitative signals — funding velocity, partnership density, and clinical evidence indicators — alongside an analyst-validated qualitative review to surface companies demonstrating genuine forward-looking momentum.

Looking across the three most active regions for digital health innovation, the result is 175 companies that collectively represent the true frontier of early-stage digital health. And when you examine the data, the picture that emerges is both more nuanced and more instructive than any single headline can capture.

The Geography of Early-Stage Capital: A Three-Speed Market

The most immediate takeaway from the HT250 dataset is that global digital health investment is not a single market — it is three very different ones, each operating at its own pace and with its own funding logic.

HT250 Investment Landscape by Region (Data as at 1 February 2026)

| Region | Companies | Total Disclosed Funding (USD) | Avg Funding per Co. (USD) | AI-Enabled (%) | Top Funding Stage |

| United States | 75 | $2.1B | $28.3M | 52% | Series A (43 cos) |

| Europe | 50 | $736.9M | $14.7M | 70% | Seed (32 cos) |

| Asia-Pacific | 50 | $152.2M | $3.5M | 58% | Seed (25 cos) |

The United States dominates by a significant margin. Seventy-five HT250 companies based in the US have collectively raised USD 2.1 billion in disclosed funding — an average of USD 28.3 million per company. Critically, 43 of those 75 companies are at Series A, indicating a maturing cohort of startups that have moved beyond proof-of-concept and are actively building commercial scale. This is a market in consolidation mode. The venture dollars being deployed in the US are larger, later, and more concentrated. For investors, this suggests that the best US-based opportunities in the HT250 cohort are not early bets on unproven technologies but deliberate bets on companies with demonstrated traction and validated product-market fit.

Europe tells a different story. Fifty companies with total disclosed funding of USD 736.9 million, averaging USD 14.7 million per company, with 32 at Seed stage. Europe is earlier, leaner, and more exploratory. The European HT250 cohort is disproportionately concentrated in Research Solutions and Medical Diagnostics — two clusters that reflect the region’s comparative strength in clinical science, genomics, and academic-to-commercial translation. For investors with a longer time horizon and an appetite for high-differentiation bets, Europe offers some of the most technically sophisticated innovation in the global HT250.

Asia-Pacific (APAC) is the most striking data point. Fifty companies, USD 152.2 million in total disclosed funding, and an average raise of just USD 3.5 million. These are capital-lean, often pre-Series A companies operating in markets where venture infrastructure is still developing. And yet the APAC HT250 cohort comprises 29 AI-enabled companies, a Wellness cluster of 9 companies reflecting demographic- and lifestyle-driven demand, and breakout companies in diagnostics and precision medicine that are building with global ambition. For investors willing to engage with a higher degree of structural complexity — regulatory environments, currency risk, partnership dynamics — APAC represents the highest-optionality opportunity in the 2026 HT250.

Where Capital Is Concentrating: Clusters, Categories, and Conviction

Beyond geography, the HT250 data surfaces a clear picture of which innovation clusters are attracting the most investor attention globally.

HT250 Company Distribution by Innovation Cluster and Region (2026 Edition)

| Primary Cluster | US | Europe | APAC |

| Health Management Solutions | 14 | 8 | 12 |

| Research Solutions | 8 | 9 | 5 |

| Medical Diagnostics | 7 | 9 | 3 |

| Patient Solutions | 9 | 4 | 4 |

| Wellness | 5 | 3 | 9 |

| Telemedicine | 7 | 1 | 4 |

| Remote Devices | 2 | 3 | 2 |

| Health InsurTech | 5 | 0 | 1 |

Health Management Solutions is the single largest cluster globally, with 34 companies spanning hospital workflow optimisation, physician tools, and prescriptive analytics. This concentration reflects a fundamental shift in where digital health value is being created: not at the consumer interface, but at the operational core of healthcare delivery. Investors who understand this are backing companies that sit inside clinical workflows — not alongside them.

Research Solutions, at 22 companies, is the second-largest cluster — and arguably the most strategically interesting for pharma and biotech investors. Companies in this cluster are building infrastructure for drug discovery, bioinformatics, and omics-driven research. Many are AI-native by design. The Alpha Scores in this cluster are among the highest in the global HT250 dataset, suggesting that the market is beginning to recognise that research-facing digital health is not a niche — it is a critical part of the next generation of therapeutic development.

Medical Diagnostics (19 companies) and Patient Solutions (17 companies) round out the top four, with Wellness (17 companies) — heavily concentrated in APAC — representing a fast-growing category that sits at the intersection of consumer behaviour change and preventive medicine. Telemedicine, while more mature as a concept, still accounts for 12 HT250 companies, reflecting continued momentum in care access and virtual-first delivery models, particularly in the US.

Therapeutic Conviction: Oncology, Women’s Health, Mental Health

The HT250 is also a window into where the clinical conviction of the global digital health investment community currently lies. Of the 175 companies in focus from the dataset, Disease Agnostic platforms — those building horizontal infrastructure applicable across conditions — represent the largest single category (69 companies). This is consistent with a maturing sector that is increasingly investing in foundational capabilities rather than condition-specific point solutions.

Among condition-specific plays, Oncology leads decisively with 27 companies, followed by Women’s Health (18), Mental Health (15), Cardiovascular Diseases (13), and Chronic Diseases (12). Oncology’s dominance reflects both the clinical urgency of the problem and the growing evidence base for digital health interventions — particularly AI-driven imaging, pathology, and early detection tools. Women’s Health has undergone a remarkable re-rating in the past three years, driven by a combination of investor interest, regulatory tailwinds, and an enormous unmet clinical need that legacy healthcare has systematically underfunded. Mental Health remains a priority, though the transition from engagement tools to clinically validated, evidence-based interventions is still underway — and the companies with the strongest Evidence Signals in the HT250 will be the ones best positioned to survive the coming standards shift.

AI Is Table Stakes. Structure Is the Differentiator.

Perhaps the most counterintuitive finding in the 2026 HT250 dataset is this: 59% of companies in the list are AI-enabled — but being AI-enabled does not, on its own, translate to a higher Alpha Score. The mean Alpha Score for AI-enabled companies in the HT250 is 54.5. For non-AI-enabled companies, it is 54.9. The difference is statistically negligible.

This is not a critique of AI in healthcare. It is a data signal about market saturation. Artificial intelligence has become the infrastructure layer of digital health, not a differentiator. It is the operating system, not the application. What differentiates companies — what the HT250’s composite Alpha Score actually measures — is the combination of funding velocity, partnership density, and clinical evidence. The companies scoring highest across those three dimensions are the ones that have done the hard work of clinical validation, regulatory engagement, and real-world deployment. AI helps them do that faster. It does not replace the need to do it at all.

This has a direct implication for investors: the era of rewarding companies simply for using machine learning in a healthcare context is over. The next phase of digital health investment will be won or lost on the depth of structured data, the quality of clinical evidence, and the density of institutional partnerships. That is what the Alpha Score is measuring. And that is what the market will reward.

Why the HT250 Is Essential Reading for Investors and Startups

For investors — whether venture capital, corporate venture, pharma business development, or health system M&A — the HT250 serves several critical strategic functions that go beyond a simple watchlist.

First, it is a deal-sourcing instrument. The companies in the 2026 HT250, drawn from a universe of more than 50,000 companies tracked by HealthTech Alpha, represent the top cohort of early-stage digital health ventures demonstrating measurable forward momentum. For investors trying to identify companies before they become obvious, the HT250 provides a structured, evidence-based entry point into the global pipeline — well ahead of traditional conference cycles or media coverage.

Second, it is a portfolio benchmarking tool. For investors with existing digital health exposure, the HT250 offers a systematic way to assess portfolio concentration by cluster, geography, therapeutic focus, and funding stage — and to identify where gaps or over-weights exist relative to the highest-signal opportunities in the market. A portfolio heavy in consumer wellness apps, for example, looks quite different when benchmarked against an HT250 that is skewed toward Health Management Solutions and Research infrastructure.

Third, it is an M&A and partnership radar. The HT250 captures companies at precisely the stage where acquisition conversations begin to make commercial sense — Series A, with validated partnerships, early evidence signals, and institutional investor backing. For corporates and pharma players looking to build their digital health capability through acquisition or strategic alliance, the HT250 is a shortcut through the noise.

For startups, the significance of the HT250 differs but is equally material. Inclusion in the list is a signal of structural credibility — a third-party, data-driven validation that a company’s fundamentals are strong enough to be ranked among the global top tier. In a fundraising environment where investor diligence has become more rigorous and the bar for Series A has risen substantially, that kind of structured, independent signal carries real weight. Startups that understand how the HT250’s scoring methodology works — and that align their evidence-building, partnership, and funding strategies accordingly — are implicitly building the foundations of venture attractiveness.

A detailed description of the HT250’s scoring methodology can be found with the full HT250 report.

Galen Growth, HealthTech Alpha, and the Strategic Value of Structured Proprietary Data

The HT250 is not just a publication. It is an expression of a fundamentally different approach to healthcare intelligence — one that the team at Galen Growth (www.galengrowth.com) has been building for years through the HealthTech Alpha platform (www.healthtechalpha.com).

HealthTech Alpha is a structured, AI-powered intelligence platform covering more than 50,000 digital health companies, 16,000 investors, and 15,000 corporates. It operates in real-time, with continuous structured refresh, applying a proprietary taxonomy — the HealthTech Alpha Digital Health taxonomy — to classify, score, and signal companies across dimensions that are commercially meaningful: funding signals, partnership signals, and evidence signals, all tracked from January 2023 through December 2025 for the current HT250 edition.

In a world increasingly shaped by generative AI, the value of structured proprietary data has never been higher — nor more widely misunderstood. The narrative around AI in enterprise contexts has focused heavily on the model layer: which foundation model is most capable, which fine-tuning approach is most effective, which inference architecture is most efficient. These are real questions. But they are secondary to the more fundamental one: what data are you working with?

General-purpose language models, however powerful, have no inherent understanding of the HealthTech Alpha taxonomy, no access to real-time funding signals, no ability to distinguish between a Series A digital therapeutics company with three published clinical trials and a Seed-stage app with a press release. Without structured, domain-specific, continuously refreshed data, AI is guessing. With it, AI becomes a genuine intelligence amplifier.

This is the core strategic insight behind the Galen Growth and HealthTech Alpha positioning. In a GenAI era, the competitive moat is not the model — it is the data. Structured proprietary datasets that capture real-world signals across a complex, high-stakes domain like digital health are extraordinarily difficult to build and nearly impossible to replicate at speed. They require years of curation, a deep taxonomy, continuous-refresh infrastructure, and domain expertise to know which signals actually matter.

Galen Growth has built precisely this. The HT250 is the public-facing product of a much deeper intelligence infrastructure. And for the investors, corporates, pharma players, and health systems that subscribe to HealthTech Alpha, the value proposition is not just access to a list of promising startups — it is access to a continuously updated, structured intelligence layer that makes every investment decision, partnership conversation, and M&A evaluation sharper, faster, and more defensible.

In a market defined by noise, that is the most valuable thing an investor can have: structured signal.

The Takeaway

The 2026 HT250 from Galen Growth is more than a ranking. It is a data-driven argument about the state of global digital health investment — where capital is flowing, where clinical conviction is strongest, and where the structural conditions for long-term value creation are most clearly in place.

The US is in Series A mode, deploying scale capital against companies that have earned it. Europe is building from the bench up, with deep technical differentiation and a Seed-stage pipeline that deserves more international investor attention than it currently receives. APAC is capital-lean and high-optionality, with a wellness and diagnostics story that will look very different in three years. And across all three regions, the companies that will define the next cycle of digital health value creation are not the ones with the most impressive AI pitch decks — they are the ones with the deepest clinical evidence, the most meaningful institutional partnerships, and the clearest path from early-stage momentum to commercial scale.

That is what the HT250 measures. And that is what investors should be looking for.

Download the HealthTech 250 list: https://www.galengrowth.com/healthtech250-2026/