TL;DR

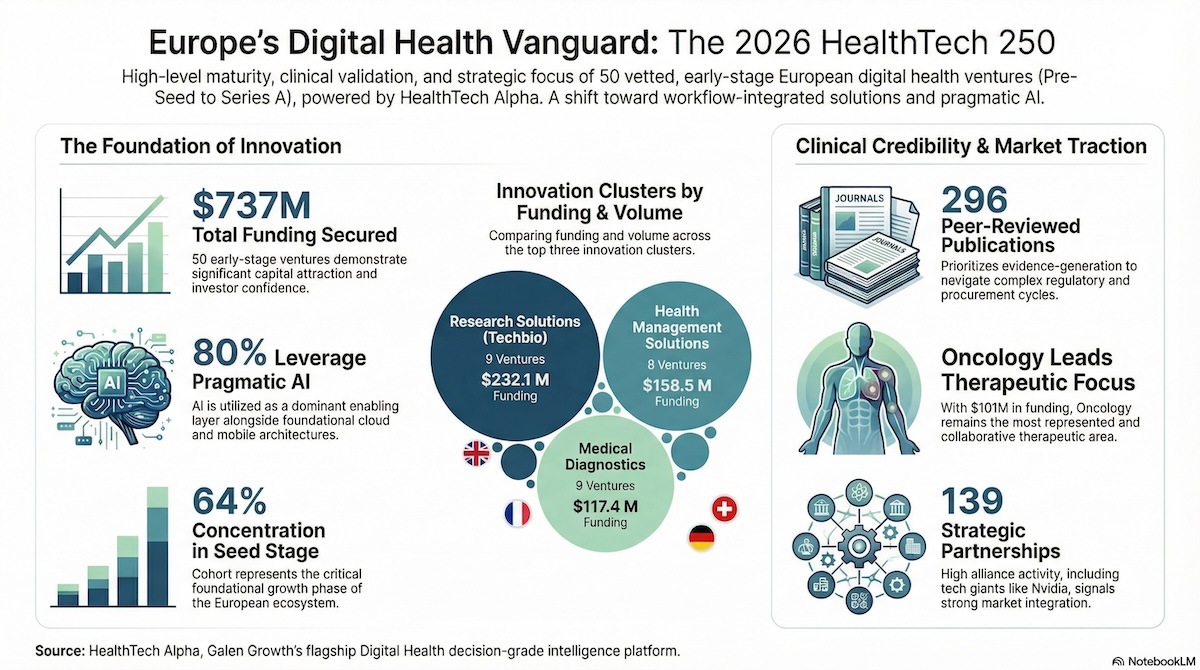

- A Data-Driven Snapshot: The HealthTech 250 (Europe) 2026 cohort (data as of 1 Feb 2026) showcases 50 Europe-based, early-stage (Pre-Seed to Series A) digital health startups selected via a rigorous, healthcare-native methodology.

- Workflow & Evidence Heavy: Europe’s strength shows up in evidence- and workflow-heavy clusters: Research Solutions, Medical Diagnostics, and Health Management Solutions make up 26 of the 50 healthtech startups (52%).

- AI as a Pragmatic Layer: AI is a dominant enabling layer, with 40 of 50 ventures (80%) explicitly listing Artificial Intelligence in their technology stack—often working seamlessly alongside foundational software, mobile, and cloud architectures.

- Oncology Leads the Charge: Oncology emerges as the most represented therapeutic area among the cohort, driving both significant partnership activity and substantial venture funding across the ecosystem.

- Designed for Decision-Grade Diligence: Built for precision, not media heat, the list utilizes waterfall eligibility filters, geography-normalised percentile benchmarking, and a weighted scoring model encompassing relevance, evidence, partnerships, funding context, momentum, and health checks.

Europe’s Early-Stage Digital Health Startups Bench is Deeper Than the Headlines Suggest

Europe does not need another “top start-ups” list that rewards press volume, the sheer magnitude of seed rounds, or proximity to the loudest innovation hubs. What Europe needs—and what investors and corporates increasingly demand—is signal. Stakeholders require a consistent, empirical way to identify which early-stage healthtech startups are accumulating the kind of validation, traction, and resilience that accurately predict scale in the complex healthcare landscape.

That is the primary purpose of the HealthTech 250 (Europe) cohort, 2026 edition. Published by Galen Growth and powered by HealthTech Alpha, this cohort is not a performative trophy cabinet; it is a meticulously structured map. It represents Europe’s most promising early-stage digital health startups as of 1 February 2026, surfaced through an execution-focused methodology. The founders in this cohort deserve genuine recognition for building in an operationally and ethically demanding environment where clinical credibility must be earned, procurement cycles are notoriously long, and outcomes are highly scrutinised. Collectively, they represent teams that understand the path to true impact in healthcare runs through evidence, integration, and trust.

1. A Data-Driven Cohort Showcasing Europe’s Best

The HealthTech 250 (Europe) 2026 cohort showcases 50 highly vetted, Europe-based, early-stage digital health startups. Eligible ventures must fall within the Pre-Seed to Series A stages, and this cohort perfectly reflects that foundational growth phase: 64% of the ventures are at the Seed stage, 24% at Series A, 10% are Grant-funded, and 2% are Pre-A.

These ventures are highly distributed across Europe’s leading innovation economies. The United Kingdom leads with 10 ventures, closely followed by France and Germany with 9 each, and Switzerland with 7.

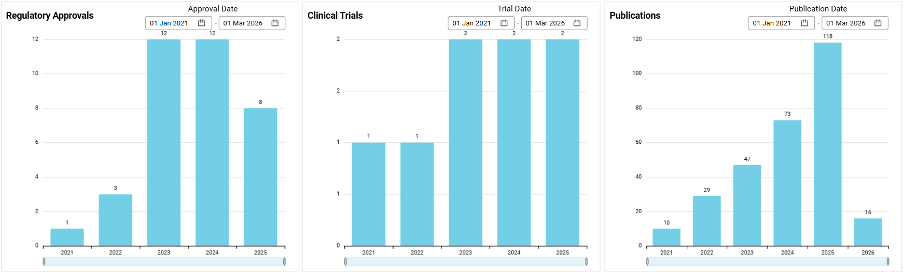

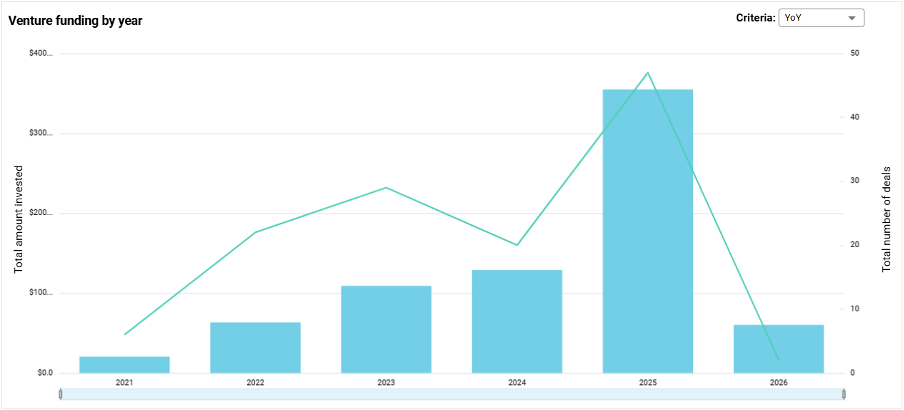

Most importantly, these 50 ventures have proven their ability to attract serious capital and forge critical alliances. In total, they have secured $737 M in funding. They boast an impressive Average Alpha Score of 54.2, indicating that they are more mature than their peers, and they have collectively announced 139 strategic partnerships. Their commitment to clinical reality is cemented by a staggering 296 peer-reviewed publications, 40 regulatory approvals, and 21 clinical trials to date.

2. Europe’s Strength: Evidence- and Workflow-Heavy Clusters

A defining signature of the 2026 cohort is precisely where its innovation is concentrated. Europe is producing “validation-first” builders, heavily leaning into science-adjacent and infrastructure-adjacent innovation.

The three largest clusters within the cohort are:

- Research Solutions (aka Techbio): 9 of 50 ventures

- Medical Diagnostics: 9 of 50 ventures

- Health Management Solutions: 8 of 50 ventures

Together, these categories represent 26 out of the 50 startups (52%). This is a vital read-through for the market. These are not the easiest categories to conquer; they require strict alignment with clinical realities, operational constraints, and regulated environments. The data indicates that Europe’s pipeline is moving far beyond simple “health apps” to build core capabilities closer to healthcare’s engine room, including evidence generation, research tooling, and clinical decision support.

The funding distribution validates this workflow-heavy focus. Out of the $736.9M raised, Research Solutions secured a massive $232.1M (32% of total funding), Health Management Solutions captured $158.5M (22%), and Medical Diagnostics brought in $117.4M (16%). The market is actively rewarding ventures that offer deep, defensible utility.

3. AI as a Pragmatic, Dominant Enabling Layer

In 2026, it is easy to claim that “AI is everywhere,” but the HealthTech 250 cohort allows us to quantify that reality. A striking 35 of 50 ventures (70%) explicitly list Artificial Intelligence as a core component of their technology stack.

However, the crucial distinction lies in how AI is being applied. In healthcare, AI that cannot survive clinical scrutiny, regulatory attention, or workflow friction is not an asset—it is technical debt. This cohort demonstrates that AI is being embedded into constrained, high-accountability use cases. It is positioned as a dominant enabling layer alongside traditional software, mobile, and cloud foundations.

This is the distinction that investors and corporate buyers increasingly demand: AI as a capability, not as marketing. Tech giants are taking note of this deep integration, with industry leaders like Nvidia emerging as highly active partners within the digital health ecosystem, holding 3 key partnerships. The cohort’s composition suggests that European teams are building within domains that mandate technological utility and robust reliability.

4. Oncology Leads as the Most Represented Therapeutic Area

While the cohort features 19 platforms (38%) categorized as “Disease Agnostic”—a pragmatic design choice that allows solutions to scale across multiple conditions and enterprise environments—when it comes to specific disease focus, Oncology stands out as the definitive leader.

Oncology is the most represented therapeutic area in the cohort, with 8 dedicated ventures. It is also the most heavily funded therapeutic area, capturing an impressive $101M in investments. The critical need for innovation in cancer care is also reflected in collaboration metrics; Oncology leads the ecosystem in partnerships, featuring in 14 distinct strategic alliances. This points to a massive, ongoing ecosystem effort to integrate digital solutions, precision diagnostics, and research tools directly into the complex continuum of cancer care.

It is also worth noting that Women’s Health is rapidly moving from a niche market to a strategic mandate. Five of the 50 ventures explicitly focus on women’s health, indicating a structural shift where these areas are being treated as society-critical product, pathway, and data priorities.

5. Methodology: Built for Decision-Grade Diligence, Not Media Heat

What separates the HealthTech 250 from generalist public rankings is its unwavering commitment to signal density over storytelling. Built to accelerate repeatable decision-making, the list relies on a two-stage selection framework designed to surface execution rather than hype.

- Universe Definition & Waterfall Filtering: To be eligible, ventures must be incorporated between 1 January 2021 and 1 February 2026, be strictly within the Pre-Seed to Series A stages, and possess sufficient structured data. A hard filter immediately removes inactive companies, acquired ventures, or late-stage entities (Series B and beyond).

- Geography-Normalised Percentile Benchmarking: Because healthcare ecosystems vary wildly in funding volumes and media visibility, eligible ventures are benchmarked using percentile comparisons within comparable regions. This normalization ensures the selection reflects relative excellence and operational momentum rather than sheer capital intake.

- Weighted Scoring Model: Ventures are ultimately evaluated using a healthcare-native taxonomy and a weighted scoring model that factors in relevance, clinical evidence, depth of partnerships, funding context, momentum, and an overall health check.

This outcome is a cohort that is inherently less performative and vastly more usable, mirroring how serious investors and corporate leaders actually build conviction.

What This Means for VCs and Later-Stage Investors

For VCs, this list acts as a powerful diligence accelerator. The signal framework helps firms quickly transition companies from “interesting” to “priority diligence,” while supporting better portfolio construction with clear exposure to specific clusters and validation pathways.

For later-stage investors, the strong mix of clinical evidence (296 publications) and strategic partnerships (139 alliances) acts as a predictive tool to identify which of these early-stage companies are most likely to successfully “graduate” to Series B readiness. Notable recent high-value raises, such as Biorce ($53M), Tandem Health ($50M), and Bioptimus ($41M), prove that the ceiling for well-validated European digital health is exceptionally high.

What This Means for Corporates (Pharma, Medtech, Payers, Providers)

For corporates, this cohort is not merely a partner list—it is an early-warning system.

- Pharma and CROs: The heavy concentration in Research Solutions should be read as a strong signal that competitive advantage is rapidly shifting towards advanced evidence generation, decentralized trial operations, precise patient identification, and decision-grade analytics.

- Medtech Teams: Medtech leaders should see a market clearly converging around hybrid capabilities. The future belongs to solutions that seamlessly blend hardware, software, continuous monitoring, and clinical services—where patient outcomes, workflow integration, and reimbursement are deeply intertwined.

- Payers and Providers: Healthcare systems and insurers should interpret the high density of Health Management Solutions as the continued, vital move towards risk stratification, care coordination, and scalable chronic disease management. However, these solutions are now expected to deliver significantly higher standards of clinical proof and seamless operational fit.

The most pragmatic takeaway for corporates: if you wait until these digital health companies are universally “proven,” you will be forced to meet them in a crowded, expensive competitive process. Engaging now allows you to act as a co-creation partner, actively shaping their operational trajectory.

Conclusion: Europe’s Advantage is Compounding

The HealthTech 250 (Europe) 2026 cohort is not simply an argument for European exceptionalism; it is an undeniable argument for European substance. This is a pipeline of early-stage healthtech startups building defensible solutions in domains where truth is rigorously tested by clinicians, health systems and regulators to result in high-level patient outcomes.

To the founders in this cohort: you are building the hard things in the hard markets—the right way. For the rest of the ecosystem, this is a decision map that invites you to engage on the metrics that truly matter: evidence, seamless integration, and scalable impact.

Ready to dive deeper into the data? [Click here to download the full list of European ventures from the HealthTech 250]