Capital, Categories, and the Structural Shifts Defining Digital Health in 2026

TL;DR

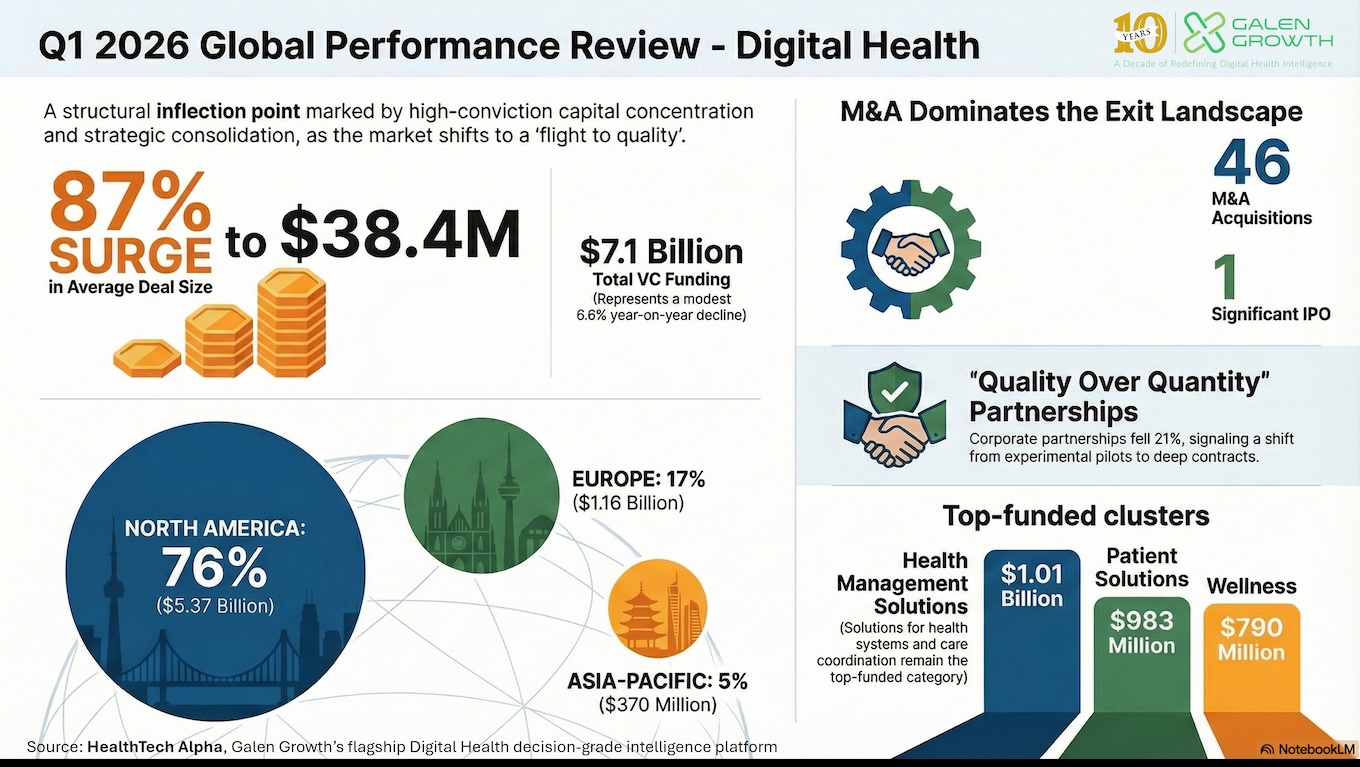

Global digital health venture funding reached $7.1 billion in Q1 2026 across 216 deals — representing a modest year-on-year decline (–6.6%) — with a further $5.1 billion deployed through exit and post-exit transactions (M&A, IPO, and post-IPO deals), bringing combined activity to $12.2 billion across 263 transactions.

46 M&A acquisitions and one IPO (Generate Biomedicines, $400 million) represent $3.5 billion in disclosed exit value across 47 exit transactions in Q1 2026. In addition, the Rznomics strategic investment/development agreement ($1.3 billion) represents a further post-exit transaction, bringing total exit and post-exit activity to $5.1 billion across 48 transactions. Health Management Solutions recorded the highest acquisition deal count (12 transactions).

North America retains a dominant VC position at 76% of global VC capital ($5.37 billion across 114 deals), whilst Europe’s VC share follows at 17% ($1.16 billion across 66 deals).

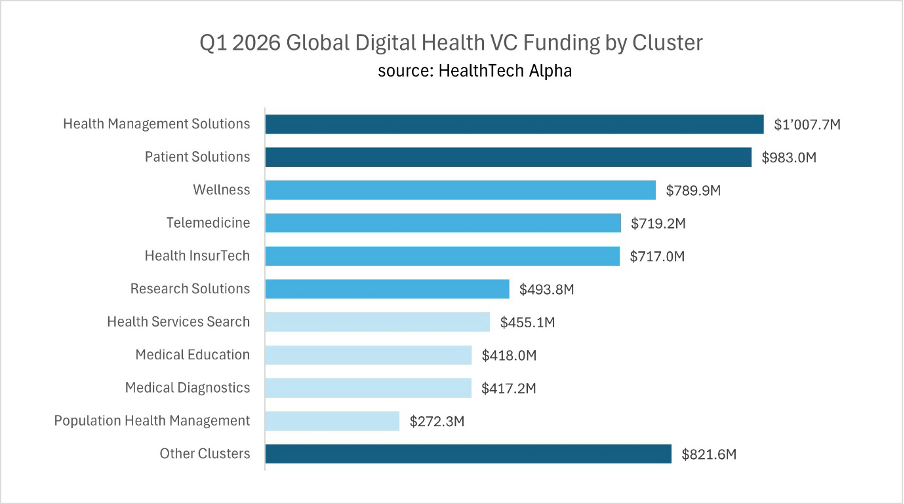

Health Management Solutions leads the digital health clusters at $1.01 billion (14.2% of VC capital), followed by Patient Solutions ($983 million, 13.9%) and Wellness ($790 million, 11.1%) — genuine venture conviction is concentrated in tools for health systems, care management platforms, and consumer health.

Corporate partnerships declined 21% year-on-year to 676 transactions, reflecting a deliberate shift from broad pilot portfolios to fewer, deeper, contractually committed relationships — the clearest signal yet that the ecosystem’s tolerance for endless pilots is exhausted.

Introduction: A Sector Finding Its Footing

The first quarter of 2026 closes with global digital health at a genuinely consequential inflection point. After the euphoric highs of 2021, the sharp corrections of 2022 and 2023, and the measured recoveries of 2024 and 2025, Q1 2026 is best understood not as a resumption of speculative growth but as a sector actively clarifying its identity. The companies attracting capital are winning on different terms than five years ago. The investors placing bets are asking harder questions. And the corporates — pharmaceutical companies, medical device manufacturers, and health systems — are transitioning from cautious observation to direct, strategic participation.

This review draws exclusively on data from the HealthTech Alpha Premium platform, tracking the global digital health ecosystem across 69 distinct categories, 18 clusters, and 19 underlying technology types — a granular taxonomy of the sector for investors and strategists. Q1 2026 data covers 216 venture funding transactions and 676 corporate partnerships recorded on the platform between 1 January and 31 March 2026. Unless otherwise stated, all venture funding figures in this review exclude M&A acquisitions and IPO exit transactions, which are analysed separately in the Exit Activity section.

The age of the broad digital health platform play, funded on the promise of a better healthcare system, is over. The age of the focused, high-conviction, operationally disciplined digital health company has begun.

The Global Funding Landscape in Q1 2026

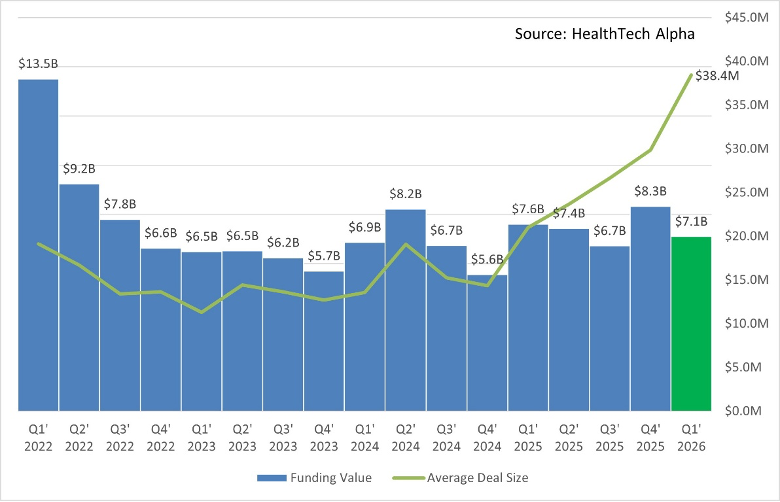

The headline finding from Q1 2026 is one of structural consolidation rather than headline growth. Pure venture funding reached $7.1 billion across 216 deals. This represents a contraction from Q1 2025, which saw $7.6 billion across 420 deals. However, the average VC deal size has surged to $38.4 million, up significantly from the $21.0 million average observed in Q1 2025.

- Q1 2026 VC Funding (excl. exits): $7.1 billion ↓6.6% vs Q1 2025

- VC Deal Count (excl. exits): 216 deals ↓48.6% vs Q1 2025

- Average VC Deal Size: $38.4 million ↑87% vs Q1 2025 ($21.4M)

- VC Mega-Deals (≥$100M): 23 transactions vs 19 in Q1 2025

The sequential comparison is equally instructive. VC capital fell from $8.3 billion in Q4 2025, across 320 deals, with deal value rising by 29%. The picture that emerges is one of accelerating capital concentration: the money is flowing into a rapidly shrinking number of high-conviction transactions.

Regional Dynamics: The US Outperforms the Globe Amidst Turbulence

In a quarter marked by geopolitical turbulence, international investment profiles shifted dramatically, with the United States absorbing most of the capital. North America recorded $5.37 billion in venture funding, making up 76% of the total capital deployed. The United States alone contributed the vast majority of this sum, massively outperforming all other regions.

| Region | VC Deals | VC Capital (USD) | Avg Deal Size | % of VC Capital |

| North America | 114 | $5.37B | $49.7M | 76% |

| Europe | 66 | $1.16B | $17.9M | 17% |

| Asia-Pacific | 30 | $370M | $12.8M | 5% |

| Middle East | 6 | $144M | $24.0M | 2% |

| Latin America | 1 | $18.1M | $18.1M | 0.4% |

Europe demonstrated resilience, ranking second with $1.16 billion in capital, bolstered by major ecosystem players in France ($322.6 million) and Switzerland ($301.9 million). Meanwhile, the Asia-Pacific region saw a significant cooling, bringing in $370 million.

Where the Capital Is Flowing: Clusters and Categories

The HealthTech Alpha taxonomy’s 18 clusters reveal highly competitive internal dynamics. Health Management Solutions is barely staying on top with $1.01 billion. Close on its heels, Patient Solutions pushes forward with $983 million, driven largely by high-profile entities like Oviva ($235 million Series D).

Health Management Solutions Maintains Momentum

Health Management Solutions secured $1.01 billion in venture funding during Q1 2026, capturing 12.6% of total VC capital and reinforcing its position as a leading cluster. The cluster continues to attract significant funding because these platforms sit at the intersection of clinical necessity and system-level scalability. It also recorded the highest acquisition deal count of the quarter with 12 transactions, reflecting consolidation across health systems and payers.

Patient Solutions on the Offensive

Patient Solutions is aggressively challenging for the top spot, with $983 million of funding, supported by major transactions such as Oviva’s $235 million round. Momentum indicates prioritisation of tangible clinical outcomes and patient engagement.

Wellness Driven by Consumer Health

Wellness secured $790 million in venture capital, driven by consumer health ventures such as WHOOP, reinforcing demand for proactive health management.

The Quarter’s Landmark Transactions

The ten largest transactions of Q1 2026 are instructive not only in their scale but in their categorical diversity. They span eight sub-categories and range from Series A to H — a signal that the digital health ecosystem’s most ambitious capital deployment is diversely distributed, although all except one deal was for a US-founded venture.

| Company | Country | Category | Stage | Amount |

| WHOOP | United States | Wearables | Series G | $575M |

| Devoted Health | United States | Health Insurance | Series F | $366M |

| Verily | United States | Prescriptive Analytics | Series E | $300M |

| OpenEvidence | United States | Health Information Platform | Series D | $250M |

| Oviva | Switzerland | Disease Management | Series D | $235M |

| Science Corporation | United States | Digital Therapeutics | Series C | $230M |

| Talkiatry | United States | Teleconsultation | Series D | $210M |

| Zipline | United States | On-demand Delivery | Series H | $200M |

| eMed | United States | Disease Management | Series A | $200M |

| Claroty | United States | Cybersecurity | Series F | $150M |

Exit Activity: M&A, IPO, and the Consolidation Wave

Q1 2026 recorded 47 exit transactions — 46 M&A acquisitions and one IPO — totalling $3.5 billion in disclosed value. With 40 undisclosed deals, the true scale of consolidation is significantly higher.

M&A Activity

The 46 M&A transactions span 13 clusters, with Health Management Solutions leading in deal count. Telemedicine dominates disclosed capital, driven by landmark transactions.

| Company | Country | Category | Value | Notes |

| Eucalyptus | Australia | Teleconsultation | $1.1B | Largest deal of Q1 2026 |

| Talkspace | United States | Teleconsultation | $865M | US mental health platform |

| Care.com | United States | Home Healthcare | $320M | Change of private equity owners |

| Kaia Health | Germany | Digital Therapeutics | $285M | European DTx consolidation |

| Gleamer | France | Medical Imaging | $266.9M | AI radiology platform |

| Torch | United States | EHR / PHR | $60M | AI health data company |

| 40 further deals | Various | Various | Various | – |

Beyond the headline values, the categorical spread of M&A activity tells a more nuanced story. Health Management Solutions’ 12 undisclosed acquisitions — spanning EHR, healthcare navigation, and care coordination — reflect a wave of health system and payer-led consolidation of point solutions into integrated platforms. These are not venture exits; they are operational rationalisations by health systems and payers that have accumulated fragmented relationships with digital health vendors and are now absorbing them.

The European M&A activity deserves particular attention. Kaia Health‘s $285 million acquisition (Germany) and Gleamer’s $266.9 million acquisition (France) represent two of the largest European digital health exits to date. Both companies had built significant clinical evidence bases — Kaia in musculoskeletal digital therapeutics, Gleamer in AI-powered radiology — that made them attractive to international acquirers seeking regulatory-ready assets in major markets.

IPO Activity

Q1 2026 produced a single IPO: Generate Biomedicines, which raised $400 million in its public debut at an implied valuation, placing it firmly in the upper tier of digital health public companies. Generate Biomedicines sits at the intersection of generative AI and drug discovery — a category that has attracted sustained venture interest over the past three years. Its IPO is significant not only as an exit event but also as a proof of concept for the public market’s appetite for AI-native biotech platforms with a credible clinical pipeline.

The broader IPO market for digital health remains dormant. The watchlist of companies described as ‘IPO-ready’ — including names in value-based care, mental health, and chronic disease management — has not materially converted into filed S-1s or completed listings in Q1 2026. The combination of public market volatility, profitability scrutiny from institutional investors, and the availability of late-stage private capital at acceptable valuations continues to make M&A the path of least resistance for most exit-stage digital health companies.

Structural Shifts: Consolidation, Evidence, and the Buyer Revolution

Consolidation: M&A as the Ecosystem’s Dominant Exit Mechanism

M&A transactions represented 46 deals and $3.4 billion in Q1 2026. Together with the Rznomics strategic investment ($1.3 billion) and the Generate Biomedicines IPO ($400 million), exit transactions account for $5.1 billion — 42% of total disclosed capital ($12.2 billion combined). This represents a structural shift in how digital health value is realised: acquisitions and strategic transactions have replaced IPOs as the primary exit pathway. As covered in detail in the Exit Activity section, most M&A deals in Q1 2026 have undisclosed valuations, suggesting the $5.1 billion disclosed figure significantly understates total exit activity.

Corporate partnerships recorded 676 transactions in Q1 2026, compared to 855 in Q1 2025 — a 21.0% year-on-year decline. This apparent contraction is not a signal of reduced corporate engagement; it reflects a deliberate shift from broad partnership portfolios to fewer, deeper, more commercially substantive relationships. The era of signing ten pilot agreements and measuring success in logos is over. The health systems, pharma companies, and device manufacturers driving partnership activity in Q1 2026 are seeking embedded, integrated, and contractually committed relationships — not exploratory collaborations.

The Health System as Kingmaker

The most consequential structural shift in the digital health market over the past 18 months is the inversion of the buyer-seller dynamic. In 2021 and 2022, venture capital set the agenda for digital health adoption. Capital flowed, companies were built to investor specifications, and health systems were expected to follow. That dynamic has inverted. The digital health companies demonstrating the strongest commercial momentum in Q1 2026 are those structured around health system procurement processes, IT interoperability requirements, administrative burden reduction, and measurable operational ROI — not those that built innovative products and then sought clinical champions.

The go-to-market strategy for a digital health company in 2026 must begin with the operational realities of the buyer, not the innovation preferences of the builder. This is a harder, slower, more expensive path to initial revenues — but it produces a fundamentally more durable commercial relationship.

The Evidence Bar Has Risen

Clinical evidence requirements for digital health reimbursement are tightening across every major market. CMS in the United States, NICE in the United Kingdom, the G-BA in Germany, and equivalent bodies in France, Japan, and Australia are increasingly requiring randomised controlled trial data — or at a minimum, robust real-world evidence with matched control populations — before expanding reimbursement coverage. The companies that invested in evidence generation during the lean years of 2022 to 2024 are now positioned to benefit disproportionately. Those that deferred that investment are facing a harder conversation with payers — and with the investors who are increasingly treating evidence maturity as a key underwriting criterion.

Why It Matters: Implications for Investors, Digital Health Companies, and Corporates

For Investors

The Q1 2026 data deliver a clear portfolio-construction message: capital concentration is accelerating, and the return profile of digital health investing is bifurcating accordingly. The 23 mega-deals (≥$100M) that account for a substantial portion of the capital deployed in Q1 2026 represent a distinct investment category from the 193 sub-$100M transactions. Generalist healthcare technology funds with undifferentiated exposure to both are likely to underperform specialist vehicles with genuine domain expertise in specific clinical areas, care settings, or geographies.

Alpha in this market in 2026 will come from conviction bets on specific clinical workflows, specific reimbursement pathways, and specific geographic first-mover advantages. The HealthTech Alpha taxonomy — 69 categories across 18 clusters, each with distinct evidence, reimbursement, and competitive dynamics — is precisely the analytical infrastructure that enables this level of specificity.

For Digital Health Companies

For digital health companies — whether at seed stage, Series B, or approaching profitability — Q1 2026 delivers an unambiguous message: commercial execution is the only currency that matters. The companies attracting follow-on capital are demonstrating revenue growth, improving gross margins, deepening relationships with enterprise customers, and reducing customer acquisition costs. They are not primarily announcing new partnerships, publishing white papers, or launching adjacent product lines.

The structural implication for company building is significant. Digital health companies in 2026 that are still optimising for fundraising metrics — user acquisition at the expense of engagement depth, pilot contracts at the expense of contracted recurring revenue, clinical publications at the expense of payer agreements — are misallocating resources against a market that has moved on. The KPIs that matter to the next generation of investors and strategic acquirers in this sector are contracted ARR, net revenue retention, and measurable clinical outcome data from deployed cohorts. The 47 exit transactions of Q1 2026 — spanning outright acquisitions and the single IPO — are a reminder that the most common exit for a digital health company in this environment is not an IPO. It is acquisition or strategic alignment, and the buyers are looking for operational, not aspirational, assets.

For Corporates: Pharma, Medical Device, and Health Systems

For pharmaceutical companies, Q1 2026’s data is a strategic signal. The $494 million deployed in drug discovery, omics research, and clinical trial innovation, in addition to the $1.3 billion Rznomics strategic round, reflects the degree to which pharmaceutical R&D organisations are now treating digital health companies as essential pipeline infrastructure rather than optional innovation supplements. The companies building competitive positions inside pharma workflows are becoming increasingly difficult and expensive to dislodge. For pharmaceutical strategy teams, Q1 2026 is an appropriate moment to assess which embedded relationships are genuine strategic assets and which are legacy commitments that should be renegotiated or replaced.

For medical device manufacturers, the $575 million WHOOP Series G and the strong performance of the Biosensors and Digital Medical Devices technology categories underscore the accelerating convergence of hardware and software. The boundary between a medical device company and a digital health company is increasingly difficult to locate — and the regulatory, commercial, and talent implications of that convergence are still being worked through. Device companies that continue to treat software as an ancillary feature rather than a core product dimension are accumulating strategic risk.

For health systems, the imperative in Q1 2026 is vendor rationalisation and investment in interoperability. The 21.2% decline in corporate partnerships year-on-year reflects, in part, a deliberate shift in the health system from broad pilot portfolios to fewer, deeper, contractually committed relationships. The health systems that have invested in HL7 FHIR-compliant data architectures and centralised digital health governance are now positioned to extract compounding value from their digital health partnerships. Those that have not are beginning to feel the cost of fragmentation acutely — and the Q1 2026 M&A wave is offering them a route to rationalisation through acquisition rather than organic integration.

Conclusion: Two Markets, One Direction of Travel

Q1 2026 presents two distinct but complementary stories about the state of global digital health — and understanding the difference between them is essential to reading the market accurately.

The venture capital story is one of disciplined concentration and regional safety. In the face of geopolitical turbulence, the United States outperformed all other markets combined. Globally, $7.1 billion was raised across just 216 deals, proving that investors are writing larger cheques into fewer, stronger companies. Health Management Solutions is barely clinging to its lead, while Patient Solutions is successfully monetising clinical specificity to close the gap. The long tail of speculative, pre-revenue digital health ventures is no longer attracting institutional capital at the pace of 2021. The bar has risen, and it is not coming back down.

The exit story is one of quiet, accelerating consolidation. Forty-six M&A transactions in a single quarter — the majority undisclosed — represent a level of private-market activity that largely falls below public visibility. The six disclosed deals totalling $3.4 billion barely capture the full scope. Strategic acquirers, including pharmaceutical companies, health systems, and diversified health technology platforms, are acquiring clinical evidence, workflow integration, and regulatory position. They are not buying growth stories; they are buying validated solutions that solve specific, high-value problems. The closure of the IPO window is a related signal: the companies best placed to go public are waiting for valuation conditions that reward demonstrated profitability rather than growth at any cost.

Taken together, the VC and exit data point in the same direction. Digital health capital — whether venture or strategic — is concentrating around clinical specificity, commercial proof, and workflow integration. The era of broad-platform bets, generalist applications, and market-creation narratives is giving way to a market that pays a premium for precision: precise clinical problems, precise buyer relationships, precise evidence bases. The companies that navigate this transition successfully — whether as investment targets, acquirers, or strategic partners — will be those that have built something irreplaceable within a defined domain, rather than something promising across many.

In Q1 2026, venture capital and exit activity told the same story from different vantage points: digital health is no longer a sector that rewards ambition alone. It rewards proof.

Methodology & Data Note

All data in this analysis is sourced exclusively from the HealthTech Alpha Premium platform (Galen Growth). The analysis covers 216 venture funding transactions (excluding M&A and IPO exits) and 676 corporate partnerships recorded between 1 January and 31 March 2026 (data refreshed 7 April 2026). Unless stated otherwise, venture funding figures exclude M&A transactions, IPO exits, and post-IPO funding. Funding amounts are reported in USD. Ventures may be classified across multiple technology types.