TL;DR

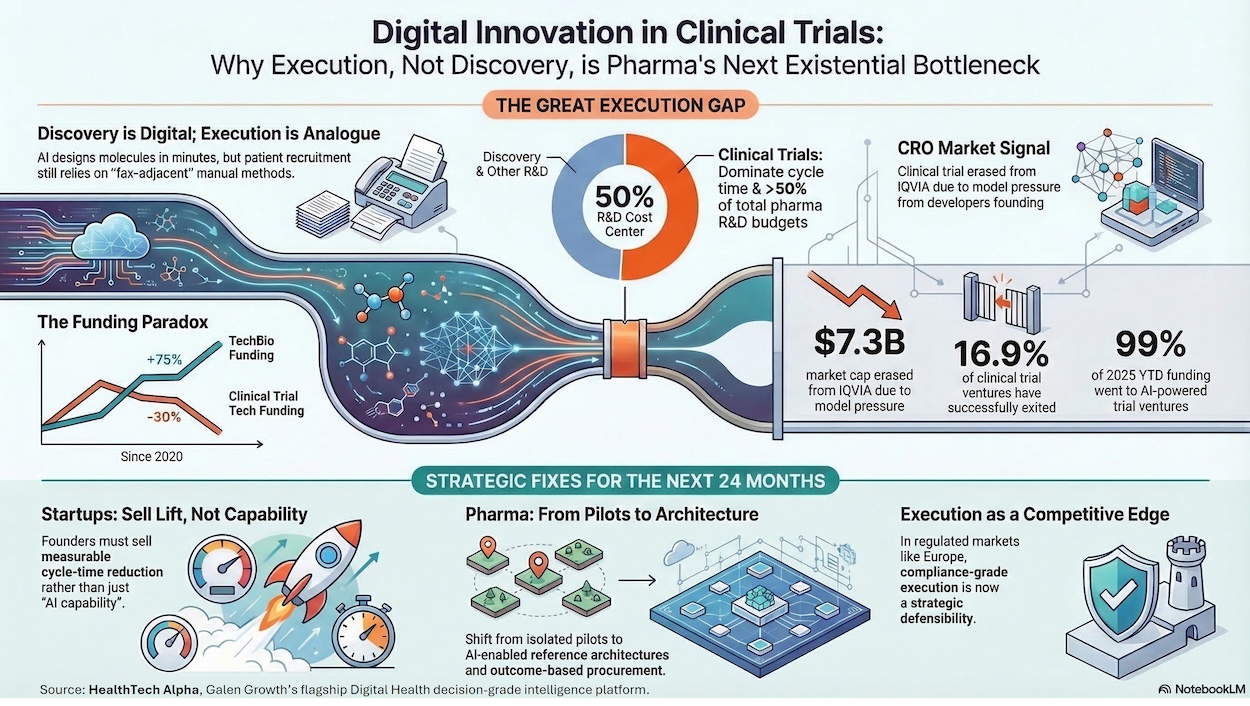

- The Bottleneck Has Shifted: TechBio funding surged +75%. Clinical trial funding fell -30%. Trials still consume >50% of total R&D costs. The bottleneck has never been discovery.

- The Valuation Paradox: Funding is down 46% over five years, yet clinical trial ventures post a 17% exit rate — the highest M&A velocity in digital health. Capital is cyclical; value is structural.

- Public Markets are Repricing CROs: Disruption isn’t coming — it’s already repricing incumbents. IQVIA lost $7.3 billion in market cap on a single guidance miss. AI-driven margin compression is not a future risk for CROs; it is a present one.

- The New Operating Model: Hybrid and decentralised trials are the new default, driving 59% of M&A activity in the sector.

- Ecosystems Over Point Solutions: 80+ new health-system partnerships in 2024–2025 confirm a decisive market shift: interoperability is no longer a differentiator, it is table stakes. Point solutions die in pilot purgatory.

TechBio has monopolised venture capital for the past two years, but the real structural value—and the highest M&A activity in digital health—now lies in the unglamorous business of clinical trial execution.

The Discovery-Execution Gap: Where the Real Bottleneck Lives

Only 3% of digital health ventures focus on clinical trials — yet this is where the pharmaceutical industry burns more than half its R&D budget. For the past twenty-four months, the digital health ecosystem has been captivated by the promise of TechBio. Investors have aggressively underwritten the thesis that artificial intelligence will revolutionise target discovery and molecule design. This enthusiasm is entirely justified by the science, but it has created a profound strategic blind spot. We have successfully taught machines to design complex molecules in a matter of minutes, yet the pharmaceutical industry continues to rely on highly analogue methods to identify the human patients needed to test them.

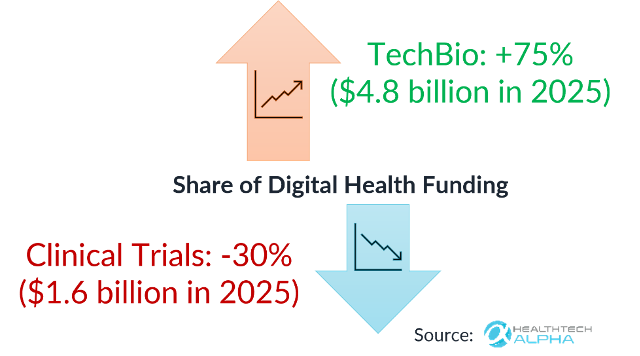

This dynamic has created a severe imbalance in capital allocation. Between 2020 and 2025, the share of digital health funding allocated to TechBio surged by 75% to reach 4.8 billion USD, while funding for clinical trial innovation contracted by 30%, with only 1.6 billion USD deployed in 2025. This divergence reveals a fundamental misunderstanding of pharmaceutical economics. Today, clinical trials consume more than 50% of total R&D costs.

The inescapable reality is that the bottleneck in bringing new blockbuster drugs to the market is no longer scientific discovery; it has shifted entirely to execution. Every month lost in the clinical trial phase is a month of patient impact delayed, and millions in capital burned. The return on investment for accelerating clinical trials is not merely incremental—it is structurally transformative, fundamentally altering the speed at which science becomes commercial medicine.

The Financial Paradox: High Liquidity, Cyclical Starvation

If one analyses the data strictly through the lens of venture capital deployment, the clinical trials sector appears starved. Funding for clinical trials technology is down a material 46% over a five-year horizon. Capital, however, is cyclical, whilst the intrinsic value of these assets is structural.

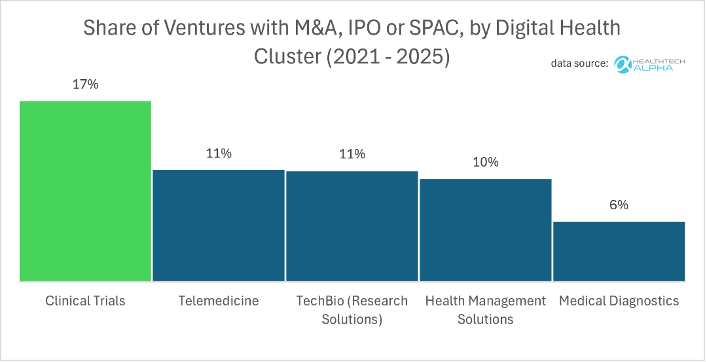

To understand the mispricing of this asset class, one must look at exit liquidity. Clinical trials ventures represent only 3% of the total digital health startup ecosystem, making them appear to be a niche category on the surface. Yet, it is disproportionately strategic. An astonishing 17% of ventures in the clinical trials cluster have successfully exited via M&A, IPO, or SPAC—a rate that dwarfs those in other highly publicised clusters such as Medical Diagnostics, TechBio, and Health Management Systems.

This creates a paradox that should be a beacon for disciplined investors and strategic corporate buyers: structural demand for trial innovation is at an all-time high, yet venture funding remains depressed. The technology is demonstrably driving outsized exits because pharmaceutical companies and large healthcare incumbents are acquiring the infrastructure needed to industrialise time-to-evidence. The gap between cyclical venture capital starvation and the high structural exit velocity presents a generational mispricing opportunity.

Geography reinforces this thesis. HealthTech Alpha data shows that 32% of European clinical trial ventures have an Evidence Signal above 40 — the highest of any region globally, ahead of North America (26%) and APAC (22%). Europe’s stringent regulatory environment is not a constraint on innovation; it is a selection mechanism that produces more credible, exit-ready assets.

Deconstructing the Clinical Trial Stack: Where Value Concentrates

To understand where the smart money is moving, one must deconstruct the architecture of modern drug testing. We categorise this into the “Clinical Trial Stack,” comprising four distinct layers where innovation clusters and value concentrates: Design, Matching, Decentralised Execution, and Data Collection.

1. Clinical Trial Design: Shifting Failure Forward

The first lever is trial design, which encompasses protocol formulation, feasibility analysis, and endpoint structuring. Historically, protocol design was an exercise in educated guesswork, resulting in costly mid-trial amendments. Today, AI is an integral part of this layer. According to HealthTech Alpha data, 86% of ventures in the clinical trial design space actively utilise AI tools — making it the most AI-saturated layer of the entire clinical trial stack. The design layer is also the most under-represented in terms of venture volume (only 14% of the stack), creating a clear supply-demand tension for investors.

By analysing vast historical datasets, AI-assisted design leads to better protocols. The mechanical translation of value here is straightforward: a better protocol leads to fewer regulatory amendments, which accelerates the start-up phase, ultimately increasing the probability of phase III success and improving capital efficiency. The strategic goal is to shift failure to the earliest possible stages of trial design, preventing wasted capital downstream.

2. Clinical Trial Matching: Changing the Funnel

Patient recruitment remains the single most dominant delay in clinical research. Traditionally, matching relied on blunt demographic filters and manual chart reviews by overburdened clinicians. Today, AI is fundamentally changing the funnel—not just the match itself. The modern recruitment funnel progresses through distinct stages: identifying the population, confirming eligibility, ensuring reachability, securing enrolment, and maintaining retention.

AI radically improves reach, parses complex eligibility logic against unstructured electronic health records, and deploys predictive retention monitoring to prevent dropouts. However, the strategic imperative here is vertical integration. The winners in this category do not merely offer a sleek user interface; they own the underlying data loop. Without control over data integration and workflow, a recruitment tool is quickly commoditised.

The scale of the problem is worth stating plainly. According to Citeline’s 2024 data, enrolment alone takes an average of 15.9 months to complete — more than four times the duration of the treatment phase itself (3.9 months). This single data point reframes the entire innovation opportunity: the largest time-sink in clinical development is not science, safety review, or reporting. It is finding and enrolling patients.

3. Decentralised Clinical Trials (DCTs): The New Operating Model

The global pandemic served as a forced catalyst for remote trials, changing regulatory precedent overnight. Regulators moved from accepting remote methods out of necessity in 2020 to increasing their comfort levels between 2021 and 2023. Looking ahead to 2024 through 2026, hybrid and decentralised trial architectures are no longer experimental; they are the default operating model.

The financial markets have already validated this shift. Among clinical trial ventures acquired from 2021 to 2025, a massive 59% were in the Decentralised Clinical Trials category. Value is rapidly concentrating in orchestration and workflow integration, as major acquirers buy up the decentralised stack to standardise operations globally.

4. Data Collection Tools: Trust as the Product

The final layer of the stack involves the actual capture and auditing of trial data. In highly regulated global markets, data collection requires rigorously regulated tools. Continuous data collection via wearables and remote sensors dramatically expands patient access and bolsters retention by removing the friction of physical site visits. Furthermore, real-time data signals enable trial sponsors to detect risks earlier and intervene proactively.

However, technology alone does not create a moat in this layer. True differentiation comes from offering Good Clinical Practice (GCP) grade controls: absolute data privacy, undeniable data integrity, and flawless audit trails. In the realm of regulated clinical evidence, trust is not a feature; trust is the entire product.

| Venture Name | Primary Category | Alpha Score | Partnership Score |

|---|---|---|---|

| Phesi | Clinical Trial Design | 60.2 | 60.6 |

| Risklick | Clinical Trial Design | 47.3 | 52.0 |

| Inato | Clinical Trial Matching | 64.0 | 54.9 |

| uMed | Clinical Trial Matching | 61.1 | 85.2 |

| Qureight | Data Collection Tools | 61.7 | 84.1 |

| Skezi | Data Collection Tools | 55.4 | 55.1 |

| Medable | Decentralised Clinical Trials | 81.6 | 89.5 |

| Teckro | Decentralised Clinical Trials | 72.9 | 48.9 |

The Public Market Warning: AI Reprices the Traditional CRO Model

If venture capital metrics highlight the opportunity, the public equities market is broadcasting a severe warning to incumbents. Disruption in clinical trials is not a theoretical future event; it is already actively re-pricing the incumbent Contract Research Organisation (CRO) model.

The most glaring proof point is IQVIA. Recently, the market erased $7.3 billion from IQVIA’s market capitalisation. Despite posting strong Q4 results, the market brutally punished the stock on lower-than-expected 2026 profit guidance. Investors are pricing in a daunting reality for traditional CROs: severe AI-driven margin risk, an impending “profitability valley” caused by mandatory internal AI and cloud spending and accelerating contract cancellations as pharmaceutical sponsors proactively cut legacy trial models.

This massive erasure of wealth indicates that the market fundamentally questions the long-term viability of human-heavy, service-oriented CROs in an era where AI can automate vast swathes of the trial workflow. Pharmaceutical companies and major CROs must aggressively standardise an AI-enabled stack and transition to procuring software based on hard outcomes—such as speed, lower amendment rates, and higher data quality—rather than billable hours. The takeaway for every stakeholder is the same: disruption is not coming — it is already repricing incumbents.

Escaping Pilot Purgatory: The Coordination Game and Ecosystems

Despite the obvious financial and operational benefits of digital clinical trial platforms, startup founders face a brutal reality: only 10% of clinical trial ventures launched in the last five years have reached Series A funding. This extraordinarily high mortality rate is largely due to the systemic friction of enterprise healthcare procurement.

Innovation frequently stalls in what industry insiders refer to as “pilot purgatory.” The lifecycle of failure is painfully predictable: a successful pilot is launched, triggering an exhaustive, multi-month IT security review. This is followed by a complex electronic health record integration phase that eventually stalls due to a mismatch of incentives among the clinical budget owner, the IT department, and the corporate sponsor.

Scaling clinical trial innovation is ultimately a massive coordination game. The solution to the pilot trap is not to run more pilots, but to mandate standardisation. Ecosystems, rather than isolated point solutions, are the entities that will win. The market data support this shift toward consolidation and collaboration: between 2024 and 2025, more than 80 new strategic partnerships were forged between health systems and clinical trial tech vendors. Scale requires uncompromising standards, seamless interoperability, and the careful alignment of incentives across pharmaceutical sponsors, CROs, and clinical sites. Interoperability has ceased to be a competitive advantage; it is now baseline table stakes.

Point of View: Strategic Imperatives for Industry, Investors, and Startups

The data leaves no room for ambiguity: the next major competitive advantage in the biopharmaceutical industry will be won in the execution layer, and clinical trials represent the ultimate arena. To capitalise on the next 24 months of market evolution, the primary stakeholders in the ecosystem must take distinct actions.

For Venture Capital and Growth Equity Investors: The current macroeconomic environment offers a rare opportunity to acquire high-value infrastructure at depressed cyclical valuations. Investors must pivot their focus away from generic AI claims and back to platforms possessing deep data moats and demonstrable workflow automation capabilities. It is vital to underwrite compliance-grade evidence as a core defensible asset. Furthermore, as traditional service-heavy CRO models undergo a structural reset, investors should anticipate significant margin volatility and target software margins that can replace human-in-the-loop inefficiencies.

For Digital Health Startups and Founders: The era of selling isolated, single-feature SaaS products to pharmaceutical companies is over. Startups must build directly into the existing workflows of sponsors and CROs, prioritising system integration from the outset. It is no longer sufficient to pitch an “AI capability”; you must sell a measurable lift in cycle times. Finally, validation, robust enterprise security, and unassailable auditability must be core product features from day one, rather than afterthoughts built for compliance reviews.

For Pharmaceutical Sponsors and CRO Leadership: Incumbents face an existential imperative to evolve or risk repricing by the public markets. Pharmaceutical leaders and CROs must abandon the perpetual cycle of disconnected technology pilots and commit to an AI-enabled reference architecture. Procurement models must radically shift from paying for access or hours to procuring strictly on clinical outcomes—specifically, speed of recruitment, reduction in protocol amendments, and absolute data quality. Scaling these technologies will only be possible if corporate leadership actively works to align the fragmented financial and operational incentives spanning the sponsor, the CRO, and the clinical site.

Galen Growth Point of View

The market has already decided. In 2025, 99% of all digital health funding deployed within the clinical trials cluster went to AI-powered ventures — not a majority, not a plurality, but effectively the entire category. The narrative that digital clinical trial innovation is a “future” disruption is not premature caution; it is statistically false. The disruption is underway, and the capital is following the signal.

The tools exist. The science is ready. The remaining bottleneck is not technological — it is a deficit of strategic coordination across sponsors, CROs, and clinical sites. The players who win the next decade will not be those who invent the best algorithm; they will be those who successfully industrialise the generation of evidence at scale. Clearing the clinical trial bottleneck is the fastest lever available to shorten the distance between a scientific breakthrough and the patient who needs it.

For the full analysis of Digital Innovation in Clinical Trials, download Galen Growth’s report: Clearing the Bottleneck: How Digital Innovation is Driving Clinical Trials