TL;DR

- Carbon Health filed for Chapter 11 protection on 2 February 2026 in the Southern District of Texas as a lender-backed “dual‑track” process: a court‑supervised sale alongside a plan to restructure (including a debt‑for‑equity swap).

- The proximate trigger was a liquidity crunch after demand normalised post‑pandemic and capital markets tightened; secondary summaries of first‑day papers cite a landlord dispute that allegedly froze about US$1.9m of cash as the acute shock.

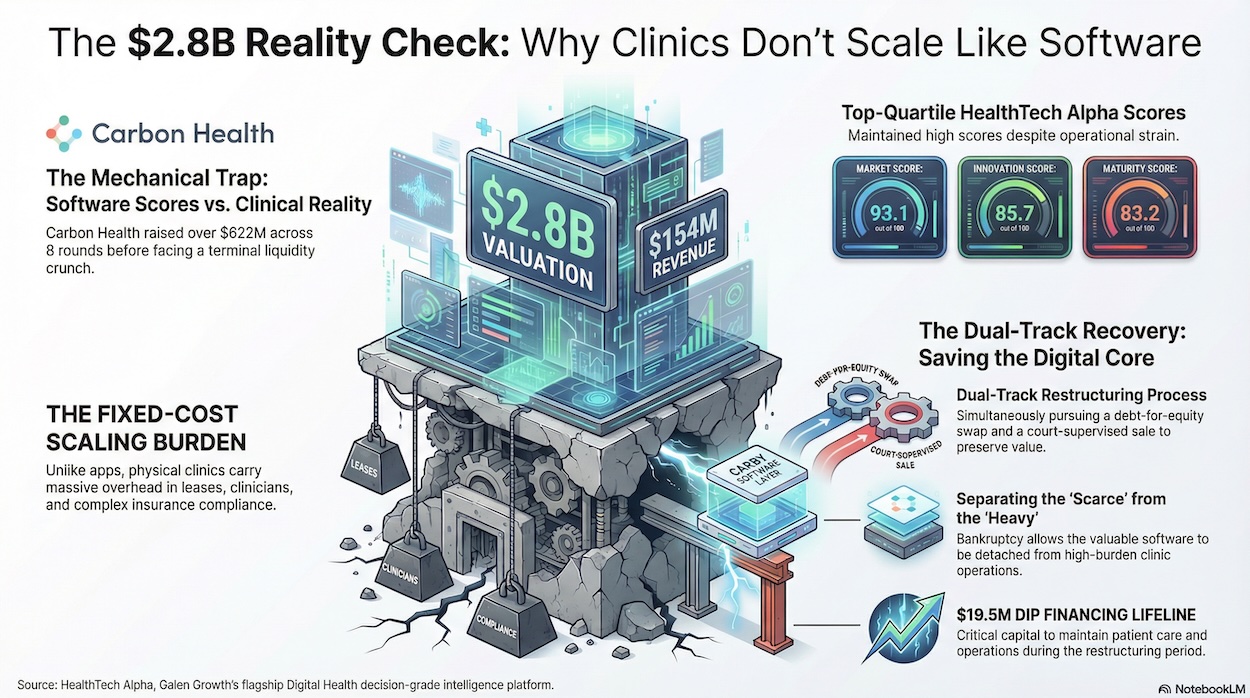

- HealthTech Alpha data shows the contradiction: a 2023 valuation of US$2.8bn and strong scores (Market 93.1/100; Innovation 85.7/100; Maturity 83.2/100; Momentum 66.6/100), supported by meaningful consumer product signals.

- But clinics are not apps. The model carries a large fixed‑cost base (leases, clinicians, compliance) and cannot expand or contract at software speed; once the growth subsidy ends, unit economics and utilisation volatility dominate.

- By the filing, restructuring coverage derived from court papers points to a debt stack anchored by at least ~US$77m secured term debt plus ~US$36m unsecured obligations and ~US$15m of clinic‑level secured facilities—against revenues reported around ~US$166m (2024) and ~US$154m TTM to 30 November 2025.

- DIP financing of up to US$19.5m kept operations running, but the number itself is a tell: the business had moved from venture‑funded expansion to bridge‑to‑restructuring survival capital.

- The likely residual value sits in the workflow/technology layer and brand; Chapter 11 is therefore less an epitaph than a mechanism to re-bundle assets into a structure that can survive healthcare’s stubbornly non‑software margins.

Carbon Health’s Chapter 11 filing is not (just) another post-ZIRP hangover. It is a stress test of an idea that investors have wanted to be true for a decade — that urgent care can be rebuilt with consumer-grade software and then scaled with software-like economics.

On 2 February 2026, Carbon Health Technologies and twenty-eight affiliated debtors filed voluntary Chapter 11 petitions, explicitly pursuing a “dual-track” outcome: confirm a restructuring plan (including a debt-for-equity exchange) while simultaneously running a court-supervised marketing and sale process. (Kroll Restructuring) The company framed the move as value-preserving and paired it with up to $19.5m of debtor-in-possession financing to maintain operations during the process. (PR Newswire)

Yet even “pre-arranged” bankruptcies are admissions. They say: the operating model may be serviceable, but the capital structure is not, and sometimes, more bluntly, that the model never converged to durable cash economics once the growth subsidy was withdrawn.

A venture-grade asset profile — by the numbers (HealthTech Alpha)

HealthTech Alpha profile data on Carbon reads like a blueprint for a category leader. Carbon Health’s 2023 valuation is pegged at $2.8bn, with employee strength in the 1,000–5,000 range — a scale that implies a genuine operational footprint rather than an app wrapped around outsourced care.

Its scores are similarly emphatic:

- Market Score: 93.1/100

- Momentum Score: 66.6/100

- Innovation Score: 85.7/100

- Maturity Score: 83.2/100

And the supporting signals extend beyond the headline indices. The data also records an Evidence Score of 52.8, a Money Score of 65.6, a Team Score of 72.6, a Maturity Score of 64.5, and a Product Score of 67 — not perfect, but far from the profile of a marginal venture.

The category placement matters. HealthTech Alpha positions it primarily in “Teleconsultation” clustered under “Telemedicine”, reflecting its “front door” strategy: a digital access layer paired with clinic capacity for escalation and continuity. That hybrid proposition was designed to arbitrage the friction in US care booking, fragmented records, and follow-up.

Capital formation: plenty of fuel — and a bigger crater

Carbon Health also enjoyed a funding arc that, in the venture imagination, should have de-risked execution: eight rounds from 2016 to 2023, including a and a $100m Series D1 (January 2023), for total capital raised “north of $622m”.

This matters for two reasons.

First, it shows the company had repeated market validation from sophisticated capital. Second, it increases the probability that the operating plan assumed a permanently friendly funding regime — because only that regime makes rapid clinic expansion feel like “growth” rather than what it often is: prepaid fixed cost.

Why health care scales operationally, not digitally

Healthcare delivery is not resistant to software. It is resistant to the assumption that software changes the cost base quickly enough to justify venture-style scaling.

The HealthTech Alpha data is clear about the mechanical trap: each physical location incurs significant capital and operational expenditures; payback is stretched by regulatory and insurance complexity; and the model’s sustainability is undermined when low-margin urgent care economics are layered with high US staffing and real estate costs.

In that context, Chapter 11 is less surprising. Trade reporting notes that Carbon Health’s filings listed assets and liabilities between $100m and $500m, with more than 100,000 creditors — a sprawling web of landlords, vendors, counterparties, and (indirectly) clinicians and patients. (fiercehealthcare.com) This is what happens when a venture thesis becomes an operating system: complexity becomes balance-sheet risk.

The DIP financing — up to $19.5m — is simultaneously reassuring and revealing: reassuring because it is intended to keep care running; revealing because it signals that liquidity headroom is limited and the restructuring must move with discipline. (PR Newswire)

Product value persists — and may be the real prize

If there is a bullish angle here, it is that bankruptcy can separate the “scarce” from the “heavy”.

The HealthTech Alpha data points to strong consumer product traction, especially in the “Carby” app suite: 4.8 stars on Apple, 16,020 reviews, release date June 2024, with availability in 40+ countries; and on Android, roughly 425k downloads with a 3.9 rating.

Those numbers do not prove profitability — but they do indicate distribution, user engagement, and a workflow layer that may be more valuable when detached from the full burden of clinic operations. This is why the dual-track process is so significant: it creates a credible path for strategic buyers to acquire (i) software/workflow IP, (ii) select geographies, or (iii) the integrated platform at a distressed price — without pretending that the original capital structure is salvageable. (PR Newswire)

SWOT (grounded in HealthTech Alpha data)

Strengths

- Brand and penetration: Marke Momentum 66.6/100 suggests a strong footprint and high activity velocity in a consumer-access model.

- Innovation + early validation: Innovation 85.7 and Evidence 52.8 indicate credible model differentiation with some integration/validation signal.

- Product distribution: Carby Health Apple 4.8★ with 16,020 reviews; Android ~425k downloads.

Weaknesses

- Fixed-cost drag: clinic expansion requires heavy upfront capex/opex and suffers from stretched payback due to reimbursement/regulatory complexity.

- Funding dependence: 8 rounds, >$622m total, last $100m (Jan 2023) — signalling a model reliant on external capital to sustain scale.

- Organisational strain: Team Score stress from layoffs/morale effects noted in the draft.

Opportunities

- Licensing / carve-out: Product Score 67 supports a credible narrative for the provider-facing workflow/EHR/scheduling layer.

- Partnership-driven re-rating Score 64.5 suggests some ability to integrate with labs/pharmacies/insurers under new ownership.

- Court-supervised sale optionality: explicit marketing + sale process alongside plan confirmation. (PR Newswire)

Threats

- Counterparty cascade risk: 100,000+ creditors, and the repubankruptcy can accelerate vendor/landlord/talent leakage. (fiercehealthcare.com)

- Competitive absorption: incumbents can absorb staff and patients during periods of uncertainty (as noted in your draft’s threat set).

- Tight liquidity envelope: $19.5m DIP is a lifeline, to drift. (PR Newswire)

The lesson investors should actually take

For venture investors, the message is not that care delivery is not a good investment; it is that it must be underwritten like infrastructure: cyclical, regulated, and operationally dense. HealthTech Alpha’s data makes the uncomfortable point: even with a $2.8bn valuation, top-quartile market and innovation scores, and a massive funding history, a hybrid provider can still be pushed into court protection if unit economics do not become cycle-proof.

For strategics, Chapter 11 may be the best window in years to acquire what is scarce — software, workflow integration, and demand aggregation — without inheriting every ounce of what is heavy. The restructuring process is, in effect, an auction for the rights to the model’s parts.

Carbon Health’s bankruptcy is therefore less a punchline than a reminder that “digital transformation” in healthcare is not a theme — it is a balance sheet.